Essential Self-Employed Investor Mortgage Options

Self-employed real estate investors face unique challenges when securing financing for investment properties. Traditional mortgage lenders often require W-2 forms and pay stubs that self-employed borrowers simply don't have. However, the mortgage landscape in 2026 offers several specialized loan programs designed specifically for investors who generate income through business ownership, freelancing, or other non-traditional employment arrangements.

Understanding the available Mortgage Loan Options for Self-Employed investors can mean the difference between missing out on profitable deals and building a successful real estate portfolio. From DSCR loans that focus on property cash flow to bank statement programs that verify income through deposits, today's market provides multiple pathways to financing.

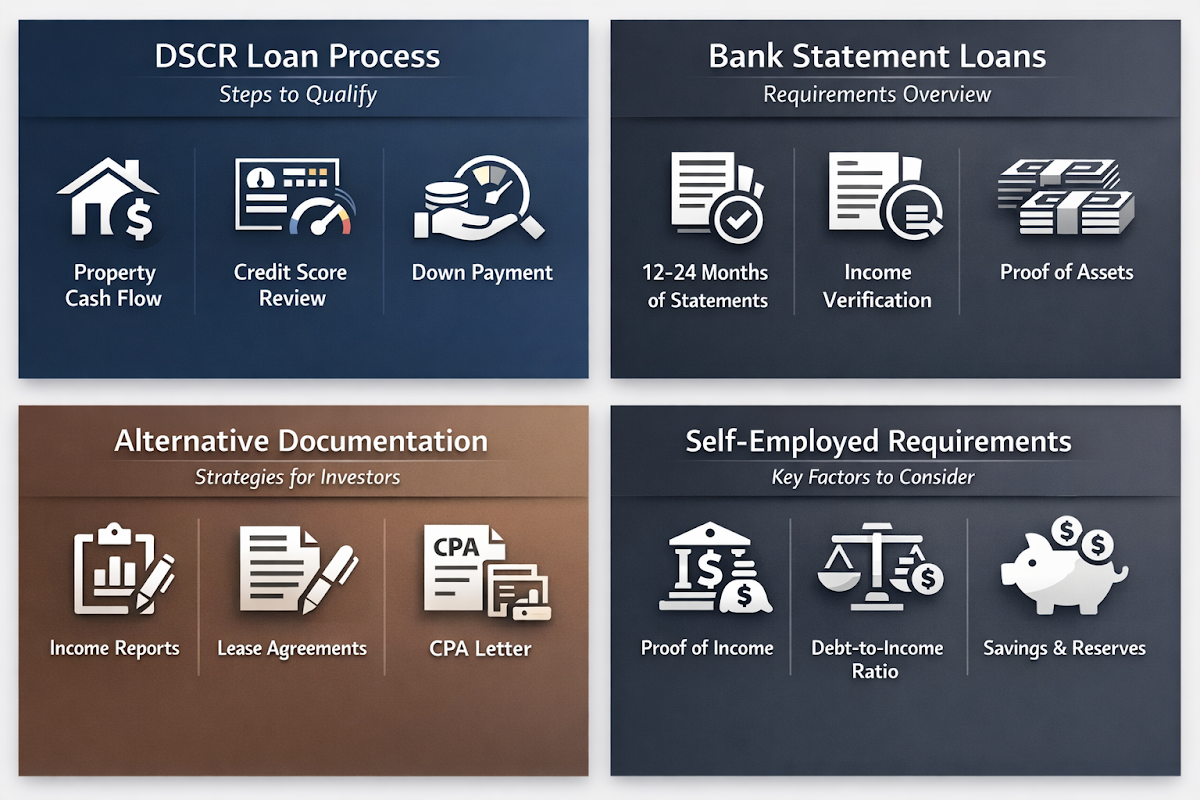

Step-by-Step DSCR Loan Qualification Process

DSCR loans represent one of the most accessible Mortgage Loan Options for Self-Employed investors because they focus on property performance rather than personal income documentation. The qualification process typically involves specific steps that streamline approval for investment properties.

- Calculate Property Cash Flow: Lenders evaluate the rental income potential against monthly mortgage payments, taxes, and insurance. A DSCR ratio above 1.0 indicates the property generates sufficient income to cover its expenses, with many lenders requiring ratios between 1.0 and 1.25 for approval.

- Prepare Reserve Requirements: Most DSCR programs require investors to maintain 2-6 months of mortgage payments in reserves. This requirement ensures borrowers can handle vacancy periods or unexpected maintenance costs without defaulting on the loan.

- Submit Property Documentation: Instead of personal tax returns or pay stubs, investors provide lease agreements, rent rolls, and property appraisals. This documentation demonstrates the property's income-generating capacity and current market value.

- Complete Credit and Asset Verification: While income documentation requirements may be relaxed, lenders still verify creditworthiness and liquid assets. Minimum credit scores typically range from 620 to 680, depending on the specific lender and loan terms.

Bank Statement Loan Requirements and Process

Bank statement loans provide another viable option among Mortgage Loan Options for Self-Employed investors who can demonstrate consistent income through business deposits. This alternative documentation approach allows lenders to verify income without traditional employment verification.

- Gather 12-24 Months of Statements: Lenders typically require personal and business bank statements covering 12 to 24 months of activity. These statements must show consistent deposits that indicate stable business income and cash flow patterns.

- Calculate Qualifying Income: Lenders analyze deposit patterns to determine average monthly income, often applying a percentage factor to account for business expenses. The calculation might use 50-75% of gross deposits as qualifying income, depending on the business type and documentation provided.

- Provide Business Documentation: Supporting documents may include business licenses, profit and loss statements, or accountant letters. While not as extensive as traditional loan documentation, these materials help verify the legitimacy and stability of the business operation.

- Meet Credit and Down Payment Standards: Bank statement loans often require higher credit scores and down payments compared to conventional mortgages. Investors might need scores above 680 and down payments of 20-25% or more for investment properties.

Alternative Documentation Strategies for Investment Properties

Beyond DSCR and bank statement loans, several alternative documentation strategies expand the available Mortgage Loan Options for Self-Employed investors. These approaches recognize that successful real estate investors often have complex income structures that don't fit traditional lending models.

- Asset-Based Qualification: Some lenders approve loans based on liquid assets rather than income verification. Investors with substantial savings, investment accounts, or other properties might qualify by demonstrating their ability to make payments from existing wealth.

- Stated Income Programs: Limited stated income options may be available for investors with excellent credit and significant down payments. These programs require borrowers to state their income on the application, though some documentation or verification might still be required.

- Portfolio Lender Options: Smaller banks and credit unions that keep loans in-house often have more flexible underwriting standards. These portfolio lenders might consider unique income sources, property types, or borrower situations that larger institutions cannot accommodate.

- Fix and Flip Bridge Financing: Short-term bridge loans designed for property rehabilitation projects often have minimal income documentation requirements. These loans focus on the property's after-repair value and the investor's experience rather than traditional income verification.

Self-Employed Mortgage Requirements and Documentation

Understanding self-employed mortgage requirements helps investors prepare comprehensive application packages that increase approval odds. While documentation varies by loan type, certain common elements appear across most mortgage programs designed for non-traditional borrowers.

- Credit Score Minimums: Most specialized loan programs require credit scores of 620 or higher, with better rates and terms available to borrowers with scores above 700. Self-employed borrowers might face slightly higher credit requirements compared to W-2 employees applying for similar loan amounts.

- Cash Reserve Standards: Lenders typically require 2-6 months of mortgage payments in liquid reserves for investment properties. These reserves provide a safety net for vacancy periods, repairs, or other unexpected expenses that could affect the borrower's ability to make payments.

- Business Continuity Documentation: Evidence of business stability, such as licenses, contracts, or client relationships, might strengthen applications. Lenders want assurance that the self-employed borrower's income source will continue beyond the loan closing date.

- Property-Specific Requirements: Investment property loans often have additional requirements such as property management agreements, lease documentation, or market rent studies. These materials help lenders evaluate the property's income potential and overall investment viability.

Documentation for Self-Employed Mortgages and Application Tips

Proper documentation for self-employed mortgages can significantly impact approval odds and loan terms. Organized, comprehensive documentation packages demonstrate professionalism and reduce processing delays that might affect time-sensitive investment opportunities.

- Maintain Consistent Banking Patterns: Regular, predictable deposits strengthen bank statement loan applications by showing stable income flows. Avoiding large, irregular deposits or transfers between accounts during the application period helps prevent underwriting questions that could delay approval.

- Organize Financial Records: Well-organized tax returns, profit and loss statements, and business documentation make the underwriting process smoother. Consider working with accountants or bookkeepers to ensure financial records accurately reflect business income and expenses.

- Prepare Asset Documentation: Complete documentation of liquid assets, retirement accounts, and other properties demonstrates financial strength. Asset documentation becomes particularly important for programs that consider overall wealth rather than just monthly income.

- Work with Experienced Loan Officers: Lenders familiar with investor loans and self-employed borrowers can guide applicants toward appropriate programs. These professionals understand the unique challenges self-employed investors face and can recommend strategies to strengthen applications.

●Conclusion

The variety of Mortgage Loan Options for Self-Employed real estate investors continues to expand as lenders recognize the growing population of non-traditional borrowers. From DSCR loans that focus on property cash flow to bank statement programs that verify income through deposits, today's market offers multiple pathways to investment property financing.

Success in securing self-employed investor financing often depends on understanding which programs align with your specific situation and preparing comprehensive documentation packages. Whether you're acquiring rental properties through DSCR loans or funding fix and flip projects with bridge financing, the key lies in matching your financial profile with the right loan product.

As lending standards and interest rates continue evolving throughout 2026, staying informed about program changes and qualification requirements becomes increasingly important. The current market environment may present opportunities for favorable rates and terms, making this an opportune time to explore financing options for your next investment property acquisition.