Mortgage Loan for Self-Employed Borrowers

Self-employed real estate investors face unique challenges when securing traditional mortgage financing. Unlike W-2 employees with steady paystubs, entrepreneurs and investors often have variable income streams that don't fit conventional lending criteria. However, specialized mortgage loan products and strategic approaches can help self-employed borrowers access the financing they need for investment properties. Understanding these alternatives could mean the difference between missing opportunities and building a profitable real estate portfolio.

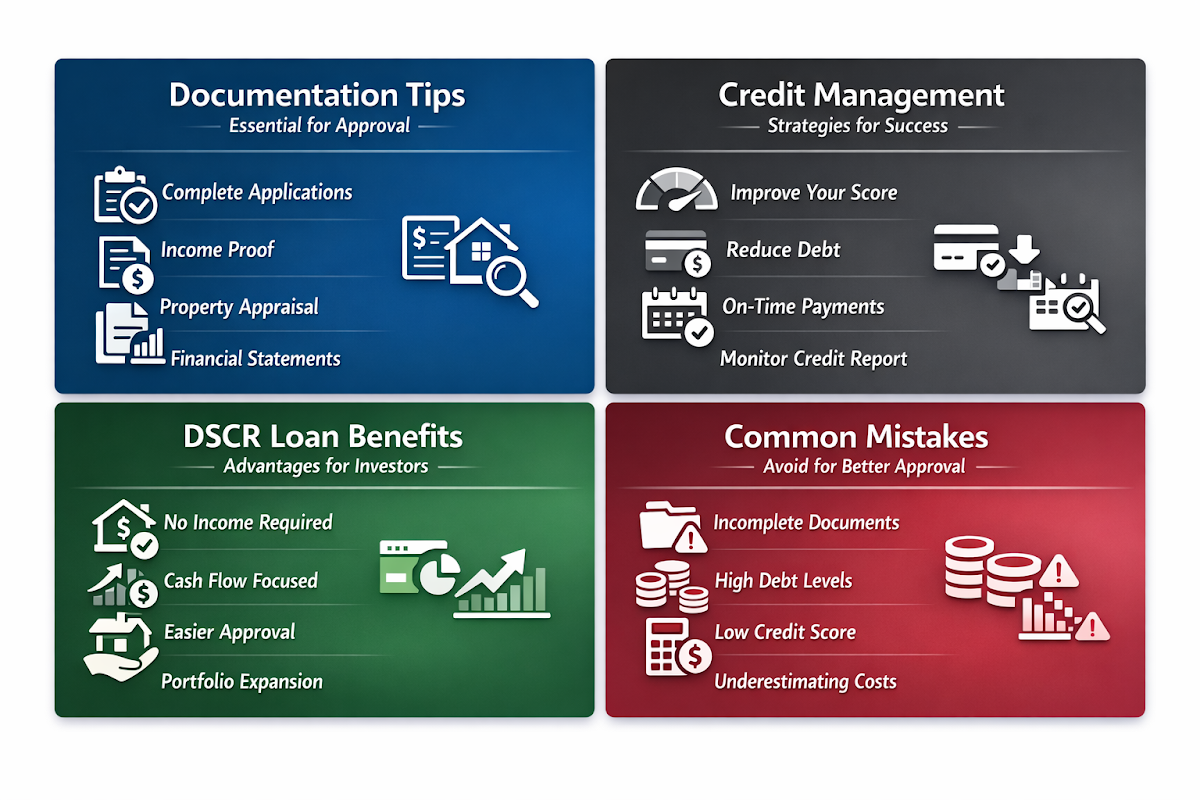

Essential Documentation Tips for Self-Employed Investors

Securing a mortgage loan for self-employed borrowers requires careful preparation and strategic documentation. These tips can significantly improve your chances of approval while streamlining the application process.

- Maintain detailed financial records: Keep comprehensive business and personal financial statements, tax returns, and profit and loss statements for at least two years. Organized documentation demonstrates financial stability and professionalism to lenders.

- Separate business and personal expenses: Clear separation between business costs and personal income makes it easier for underwriters to evaluate your true earning capacity. This practice also helps when calculating debt-to-income ratios for loan qualification.

- Work with experienced accountants: Professional tax preparation can optimize your returns while ensuring compliance with lending requirements. Accountants familiar with real estate investment can structure your finances to support mortgage applications.

- Document consistent income patterns: Even if your monthly income varies, showing consistent annual earnings or growth trends helps establish creditworthiness. Lenders typically look for stability over time rather than month-to-month consistency.

Alternative Income Verification Strategies

Traditional income verification methods might not capture the full financial picture for self-employed borrowers. These alternative documentation methods can help demonstrate your ability to service mortgage debt effectively.

- Bank statement analysis: Many lenders now accept bank statements as primary income documentation, typically requiring 12 to 24 months of statements. This method allows underwriters to see actual cash flow rather than tax-adjusted income figures.

- Asset-based qualification: Some loan programs focus on your asset portfolio rather than traditional income metrics. Investment properties, retirement accounts, and liquid savings can serve as qualification criteria for certain mortgage products.

- Debt service coverage evaluation: For investment properties, lenders may evaluate the property's rental income potential against the proposed mortgage payment. This approach emphasizes the property's ability to generate cash flow rather than personal income alone.

Smart Credit Management for Self-Employed Borrowers

Credit scores carry extra weight for self-employed mortgage applicants since lenders often view variable income as higher risk. Implementing these credit management strategies can help offset income documentation challenges.

- Monitor credit reports regularly: Check all three credit bureaus quarterly and dispute any inaccuracies immediately. Small errors can significantly impact approval odds when income documentation is non-traditional.

- Optimize credit utilization ratios: Keep credit card balances below 30% of available limits, ideally under 10% for optimal scoring. Low utilization demonstrates financial discipline and improves your overall credit profile.

- Avoid new credit applications: Limit hard inquiries in the months leading up to your mortgage application. Multiple inquiries can lower your score and raise questions about your financial stability during underwriting.

- Maintain established credit accounts: Keep older accounts open to preserve credit history length. Closing accounts can reduce available credit and negatively impact your credit utilization ratios.

DSCR Loan Benefits for Investment Properties

Debt Service Coverage Ratio loans offer significant advantages for self-employed real estate investors seeking financing for rental properties. Understanding these benefits can help you choose the right financing strategy for your investment goals.

- No personal income verification required: DSCR loans focus on the property's rental income potential rather than borrower income documentation. This eliminates the need for tax returns, bank statements, or employment verification that can complicate traditional mortgage applications.

- Faster closing timelines: With simplified documentation requirements, DSCR loans typically close faster than conventional mortgages. This speed advantage can be crucial when competing for investment properties in active markets.

- Higher loan amounts possible: Since qualification is based on property cash flow rather than personal debt-to-income ratios, investors may access larger loan amounts. This increased borrowing power can open opportunities for higher-value properties.

- Portfolio expansion flexibility: DSCR loans don't count against conventional loan limits, allowing investors to finance multiple properties simultaneously. This flexibility supports rapid portfolio growth strategies without traditional lending constraints.

Bank Statement Loan Program Requirements

Bank statement loan programs provide viable alternatives for self-employed borrowers who cannot qualify through traditional income documentation. These programs have specific requirements that investors should understand before applying.

- Minimum credit score thresholds: Most bank statement programs require credit scores between 660 and 760 for approval. Higher scores typically unlock better interest rates and more favorable loan options, making credit optimization a priority before applying.

- Bank statement timeframes: Lenders typically require 12 to 24 months of personal or business bank statements for income analysis. Consistent deposits and account management during this period are crucial for demonstrating financial stability.

- Down payment expectations: Bank statement loans often require larger down payments than conventional mortgages, typically 20% to 25% minimum. Investment properties may require even higher down payments, so plan your capital allocation accordingly.

- Reserve requirements: Many programs require borrowers to maintain cash reserves equal to several months of mortgage payments. These reserves provide additional security for lenders when income documentation is non-traditional.

Common Self-Employed Mortgage Application Mistakes

Avoiding these common mistakes can significantly improve your chances of mortgage approval and secure better loan terms for your investment properties.

- Mixing personal and business finances: Commingled accounts make income verification difficult and may raise red flags during underwriting. Maintain separate business and personal banking relationships to simplify the documentation process.

- Inadequate financial documentation: Incomplete records or missing documents can delay approval or result in loan denial. Prepare comprehensive financial documentation well before applying to avoid last-minute scrambling.

- Unrealistic income claims: Overstating income or cash flow projections can backfire during verification. Be honest and conservative in your financial representations to build creditor trust and avoid complications.

- Ignoring debt-to-income ratios: Even with alternative documentation, lenders still evaluate your ability to service debt. Pay down existing obligations before applying to improve your qualification profile.

- Poor timing of major purchases: Large purchases or new credit obligations during the application process can derail approval. Avoid major financial changes until after closing to maintain your qualification status.

●Conclusion

Successfully securing a mortgage loan for self-employed borrowers requires strategic planning, proper documentation, and understanding of alternative lending programs. Bank statement loans and DSCR financing provide viable paths for real estate investors who don't fit traditional employment models. By maintaining organized financial records, optimizing credit profiles, and working with experienced mortgage professionals, self-employed investors can access the financing needed to build profitable real estate portfolios. The key is preparation and choosing the right loan program that aligns with your business structure and investment goals.