Essential Mortgage Application Checklist for Real Estate Investors

Navigating the mortgage application process as a real estate investor requires careful preparation and attention to detail. A comprehensive mortgage application checklist can mean the difference between swift approval and costly delays. With DSCR loans and investor-focused financing products becoming increasingly popular, understanding the specific requirements and documentation needed has never been more critical.

The mortgage application process timeline typically spans 30 to 45 days, but proper preparation with the right documents can streamline your experience significantly. Whether you're seeking financing for fix and flip projects, rental properties, or expanding your investment portfolio, having all required mortgage documents organized from the start positions you for success.

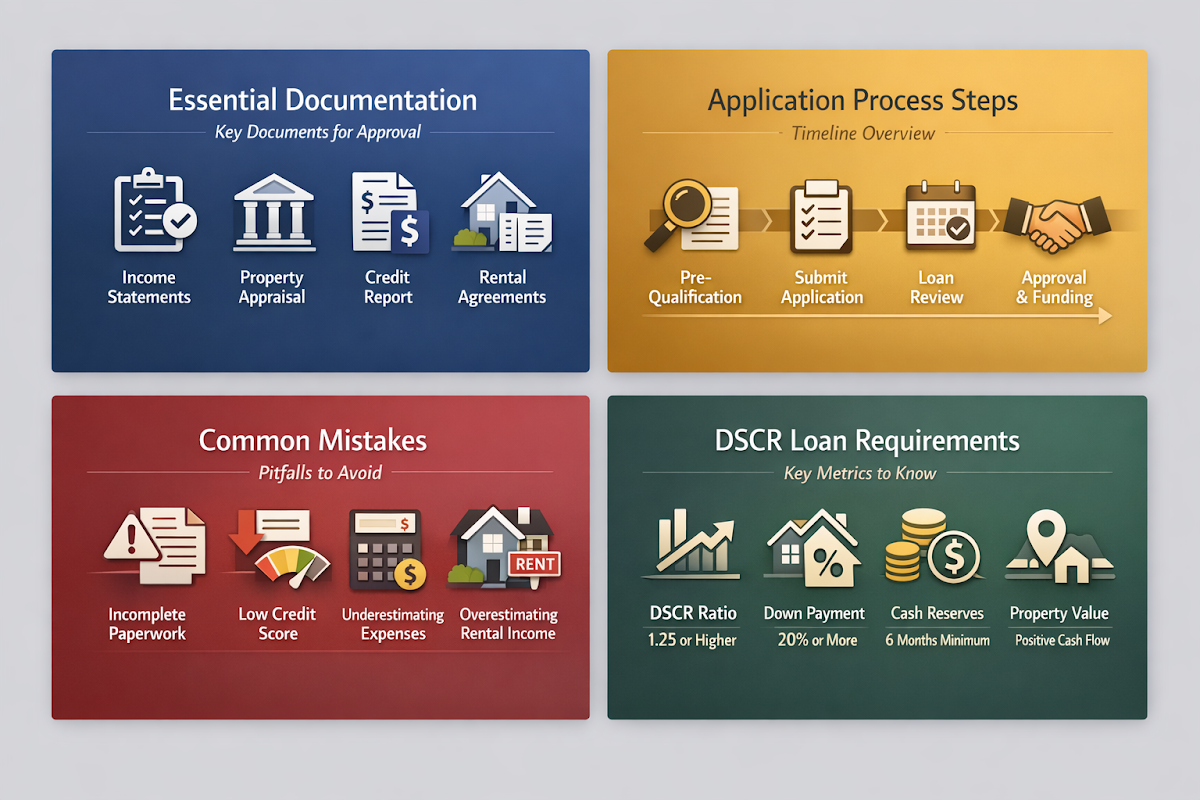

Essential Documentation for Your Mortgage Application

Having the right documentation ready is crucial when preparing your mortgage application checklist. Lenders typically require specific financial records to evaluate your creditworthiness and the property's income potential, especially for DSCR loans where rental income analysis plays a central role.

- Property appraisal and rental income analysis: For DSCR loans, lenders focus heavily on the property's income-generating potential rather than personal income metrics. A professional appraisal that includes detailed rental income projections is essential.

- Credit score documentation: Maintaining a strong credit score is increasingly important as lenders tighten DSCR loan conditions. Credit scores help gauge debt management proficiency, which is pivotal for investors planning strategic acquisitions.

- Financial statements and tax returns: While DSCR loans may rely less on personal income, having recent tax returns and financial statements readily available demonstrates financial stability to lenders.

- Property purchase agreements and contracts: For investment properties, clear documentation of the purchase agreement, including any renovation plans for fix and flip projects, helps lenders understand the investment strategy.

- Existing portfolio documentation: If you own other rental properties, providing lease agreements and income statements from your current portfolio can strengthen your application by demonstrating successful property management experience.

What You Should Do When Applying

Following best practices during the mortgage application process can significantly improve your chances of approval and help maintain a smooth timeline. These strategic approaches are particularly important for investor-focused financing products.

- Organize all required mortgage documents in advance: Create a comprehensive file with all necessary paperwork before beginning the application process. This proactive approach can reduce processing time and demonstrate professionalism to lenders.

- Utilize rental income figures effectively: For DSCR loans, rental income from short-term rentals like vacation properties can enhance qualification chances. Present detailed income projections and market analysis to support these figures.

- Maintain clear communication with your lender: Stay responsive to requests for additional documentation and provide updates promptly. This helps keep your application moving through the approval pipeline without unnecessary delays.

- Prepare for potential regulatory changes: Stay informed about evolving DSCR loan requirements and regulations that might affect your application strategy, especially as the lending landscape continues to shift in 2026.

Critical Mistakes to Avoid During Applications

Understanding common pitfalls can help you navigate the mortgage application process more effectively. These mistakes could potentially derail your financing plans or create unnecessary complications during the approval process.

- Don't overlook hidden fees and costs: Regulatory shifts in the DSCR loan landscape may introduce additional fees that could affect your investment calculations. Budget for potential cost increases and factor these into your deal analysis.

- Don't submit incomplete financial documentation: Missing or outdated financial records can significantly delay the mortgage application process timeline. Ensure all documents are current and properly formatted before submission.

- Don't ignore credit score requirements: With lenders increasingly focusing on credit scores for debt management assessment, neglecting to address credit issues before applying can result in rejection or less favorable terms.

- Don't underestimate property income potential: Failing to provide comprehensive rental income analysis, especially for properties with short-term rental potential, can limit your borrowing capacity under DSCR loan programs.

Understanding DSCR Loan Requirements in 2026

The DSCR loan landscape continues to evolve, with lenders adjusting their qualification metrics and focusing more heavily on property performance rather than personal income. Understanding these updated requirements helps real estate investors optimize their mortgage application checklist for success.

- Debt-Service Coverage Ratio calculations: Lenders typically require the property's net operating income to exceed the debt service by a specific margin. This ratio demonstrates the property's ability to cover mortgage payments through rental income.

- Property type and location considerations: Different property types may have varying DSCR requirements. Short-term rental properties might face additional scrutiny due to income volatility concerns, while traditional long-term rentals may have more standardized requirements.

- Down payment and reserve requirements: DSCR loans often require larger down payments compared to traditional mortgages, with some lenders requiring 20-25% down. Additionally, maintaining adequate cash reserves for property maintenance and vacancy periods is typically expected.

- Portfolio lending considerations: Investors with multiple properties may benefit from portfolio lending approaches, where lenders evaluate the overall performance of the investment portfolio rather than individual property metrics.

Optimizing Your Mortgage Application Process Timeline

The mortgage application process timeline can vary significantly based on preparation, property type, and lender efficiency. Understanding typical timeframes and potential bottlenecks helps investors plan their acquisition strategies more effectively.

- Pre-application preparation phase (1-2 weeks): Gathering all required mortgage documents, obtaining credit reports, and organizing financial statements before beginning the formal application process can save considerable time later.

- Application submission and initial review (3-5 days): Once submitted, lenders typically conduct an initial review to ensure all basic requirements are met. Complete applications with proper documentation move through this stage more quickly.

- Property appraisal and income analysis (1-2 weeks): For DSCR loans, the appraisal process includes detailed rental income analysis, which may take longer than traditional appraisals. Market conditions and appraiser availability can affect this timeline.

- Underwriting and final approval (2-3 weeks): The underwriting process involves thorough review of all documentation, verification of income projections, and final risk assessment. Well-prepared applications with complete documentation typically move through underwriting more efficiently.

●Conclusion

A well-organized mortgage application checklist serves as your roadmap to successful investor financing. By understanding the specific requirements for DSCR loans, maintaining proper documentation, and avoiding common mistakes, real estate investors can navigate the application process more efficiently and secure the financing needed to grow their portfolios.

The key to success lies in preparation and understanding that DSCR loans evaluate properties differently than traditional mortgages. Focus on demonstrating the income-generating potential of your investments, maintain strong credit profiles, and stay informed about evolving requirements in the lending landscape. With proper preparation and attention to detail, your mortgage application checklist becomes a powerful tool for achieving your real estate investment goals.