Business Loan Application Process Guide

The business loan application process for real estate investors requires strategic preparation and thorough understanding of lender requirements. Whether you're securing DSCR loans for rental properties or bridge financing for fix and flip projects, success depends on meeting specific criteria and submitting complete documentation packages. This comprehensive guide walks you through the essential steps to navigate the application process effectively and increase your approval chances in today's competitive lending environment.

Essential Documentation Checklist

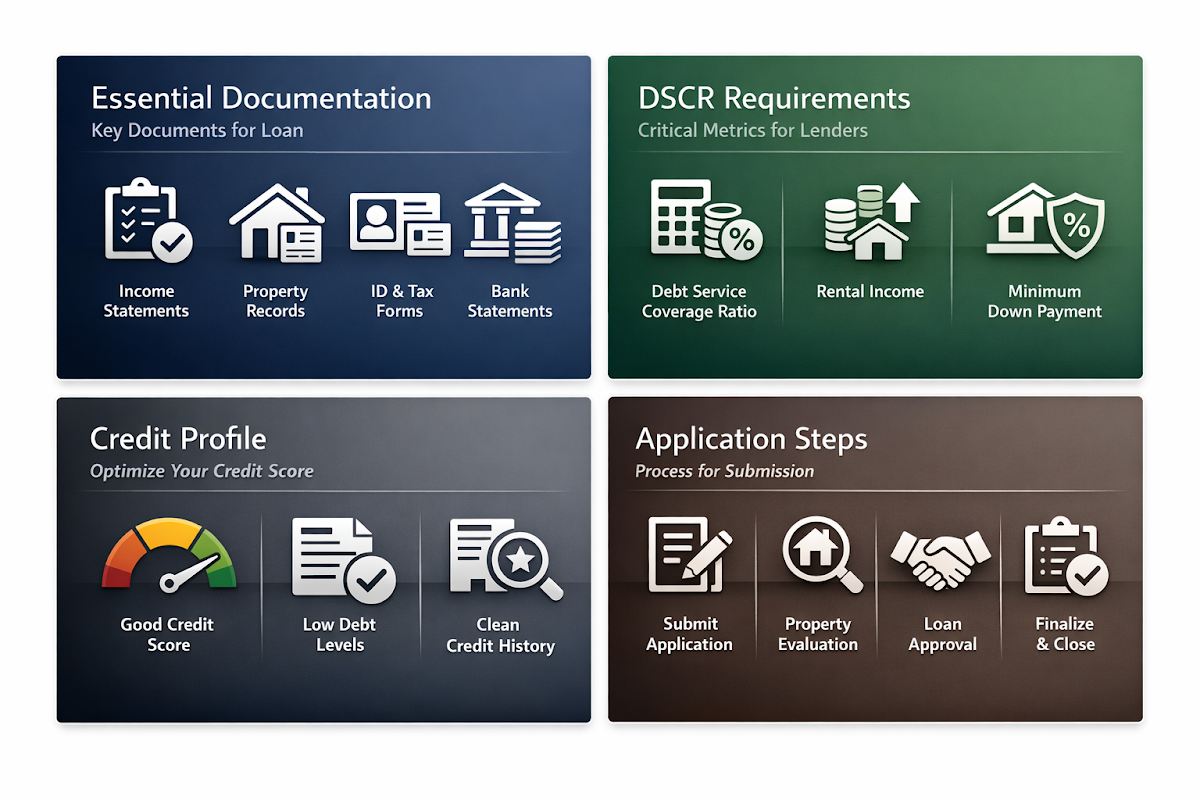

Essential documentation checklist preparation forms the foundation of any successful business loan application process. Real estate investors must gather comprehensive financial records and property-specific documents to demonstrate their investment viability to lenders.

- Financial Statements: Provide recent bank statements, tax returns for the past two years, and profit and loss statements that showcase your financial stability and cash flow management capabilities.

- Property Documentation: Include detailed property photos, current lease agreements, rent rolls, and property appraisals to demonstrate the asset's income-generating potential and market value.

- Credit Reports: Obtain current credit reports showing your creditworthiness, as most lenders typically require credit scores of 620 or higher for DSCR loan approval.

- Reserve Requirements: Document liquid assets and cash reserves, as lenders often require 2-6 months of mortgage payments in reserves for rental property investments.

DSCR Requirements and Ratios

DSCR requirements and ratios represent the cornerstone metrics that lenders evaluate during the business loan application process for rental property investments. Understanding these calculations helps investors position their properties for optimal financing terms.

- Minimum DSCR Threshold: Maintain a debt service coverage ratio of 1.0-1.25, ensuring your property generates 100-125% of its debt obligations to meet most lender standards.

- Income Documentation: Provide comprehensive rental income verification through lease agreements, rent rolls, and market rent analyses to support your DSCR calculations accurately.

- Expense Analysis: Account for property taxes, insurance, maintenance costs, and vacancy allowances in your DSCR calculations to present realistic cash flow projections.

- Portfolio Performance: Demonstrate consistent rental income across your investment portfolio to strengthen your overall DSCR profile and lending relationship.

Credit Profile Optimization

Credit profile optimization plays a crucial role in the business loan application process, as lenders use credit metrics to assess risk and determine loan terms for real estate investors seeking DSCR financing.

- Credit Score Management: Work toward maintaining credit scores above 620, though some lenders may require higher scores of 680 or more for the most favorable terms and rates.

- Debt-to-Income Ratios: Monitor your overall debt obligations and ensure manageable debt-to-income ratios that demonstrate your ability to handle additional investment property financing.

- Payment History: Establish consistent payment patterns across all existing credit accounts and mortgages to build credibility with potential lenders during the application review process.

- Credit Utilization: Keep credit card balances low relative to available limits to maintain strong credit utilization ratios that support your loan application strength.

Application Submission Steps

Application submission steps require careful coordination and timing to ensure your business loan application process moves smoothly through lender review and approval stages.

- Initial Application Review: Submit your complete loan application with all required documentation, ensuring accuracy and completeness to avoid delays in the preliminary approval process that could impact your investment timeline.

- Property Appraisal Coordination: Schedule and coordinate the required property appraisal once your application enters review, as this critical step typically takes 7-14 days and directly impacts your loan approval decision.

- Underwriting Communication: Respond promptly to any underwriter requests for additional documentation or clarification, maintaining open communication channels to facilitate efficient processing of your DSCR loan application.

- Final Approval Preparation: Prepare for closing by reviewing loan terms, coordinating with title companies, and ensuring all conditions are met for successful funding of your investment property financing.

Timeline and Processing Expectations

Timeline and processing expectations vary depending on loan type and lender requirements, but understanding typical timeframes helps investors plan their business loan application process effectively.

- Initial Review Phase: Expect 3-5 business days for initial application review and preliminary approval decisions, during which lenders assess your basic qualifications and documentation completeness for DSCR loan eligibility.

- Documentation Verification: Allow 5-10 business days for lenders to verify submitted documents, conduct background checks, and review your financial statements and property information in detail.

- Appraisal and Inspection: Plan for 7-14 days for property appraisal completion and any required inspections, as these steps often represent the longest portion of the approval timeline.

- Final Underwriting: Reserve 3-7 business days for final underwriting decisions and loan document preparation, ensuring all conditions are satisfied before proceeding to closing.

- Closing Coordination: Schedule closing 2-3 days after final approval, allowing time for title work completion and funding preparation for your investment property acquisition.

Key Success Factors

Key success factors in the business loan application process center on thorough preparation and strategic positioning of your investment profile. Real estate investors who demonstrate strong financial management, maintain comprehensive documentation, and present realistic cash flow projections typically experience smoother approval processes and more favorable loan terms. Working with experienced lenders who specialize in investor financing can also significantly improve your chances of securing the DSCR loans and bridge financing needed for your real estate investment goals.

●Conclusion

Successfully navigating the business loan application process requires strategic preparation, thorough documentation, and understanding of lender requirements specific to real estate investment financing. By maintaining strong DSCR ratios, optimizing your credit profile, and submitting complete application packages, you position yourself for favorable loan terms and efficient approval timelines. Remember that each lender may have slightly different requirements, so working with mortgage professionals who specialize in investor financing can provide valuable guidance throughout your application journey. With proper preparation and realistic expectations, you can secure the financing needed to grow your real estate investment portfolio effectively.