Off-grid living has grown in popularity as more people seek sustainable, self-sufficient lifestyles away from traditional neighborhoods. For veterans and active-duty service members, the idea of combining that freedom with the powerful benefits of a VA home loan sounds appealing. But here's the thing — figuring out how to qualify for a VA loan with off-grid yurts is more complicated than a standard home purchase. Yurts are circular, tent-like dwellings with roots in Central Asian nomadic culture, and while they've evolved into surprisingly comfortable permanent homes, lenders and the Department of Veterans Affairs don't always see them the same way a buyer does. This guide breaks down the real requirements, the likely hurdles, and the practical steps veterans can take when pursuing VA loan for unconventional housing.

What Makes a VA Loan So Valuable for Veteran Homebuyers

Before diving into the property-specific challenges, it helps to understand why veterans are so eager to use their VA loan benefit in the first place. The VA home loan program, backed by the U.S. Department of Veterans Affairs, offers several advantages that are genuinely hard to match in the conventional mortgage market.

- No down payment required — eligible veterans can finance 100% of the purchase price

- No private mortgage insurance (PMI) — a significant monthly savings compared to FHA or conventional loans with low down payments

- Competitive interest rates — VA loans often carry rates that may be lower than conventional alternatives

- Flexible credit guidelines — lenders may work with borrowers who have less-than-perfect credit histories

- Limits on closing costs — the VA restricts certain fees that lenders can charge

These benefits make the VA loan one of the most attractive mortgage programs available. However, that value comes with a framework — specifically, the VA's Minimum Property Requirements (MPRs), which every home must meet before it can be financed through this program.

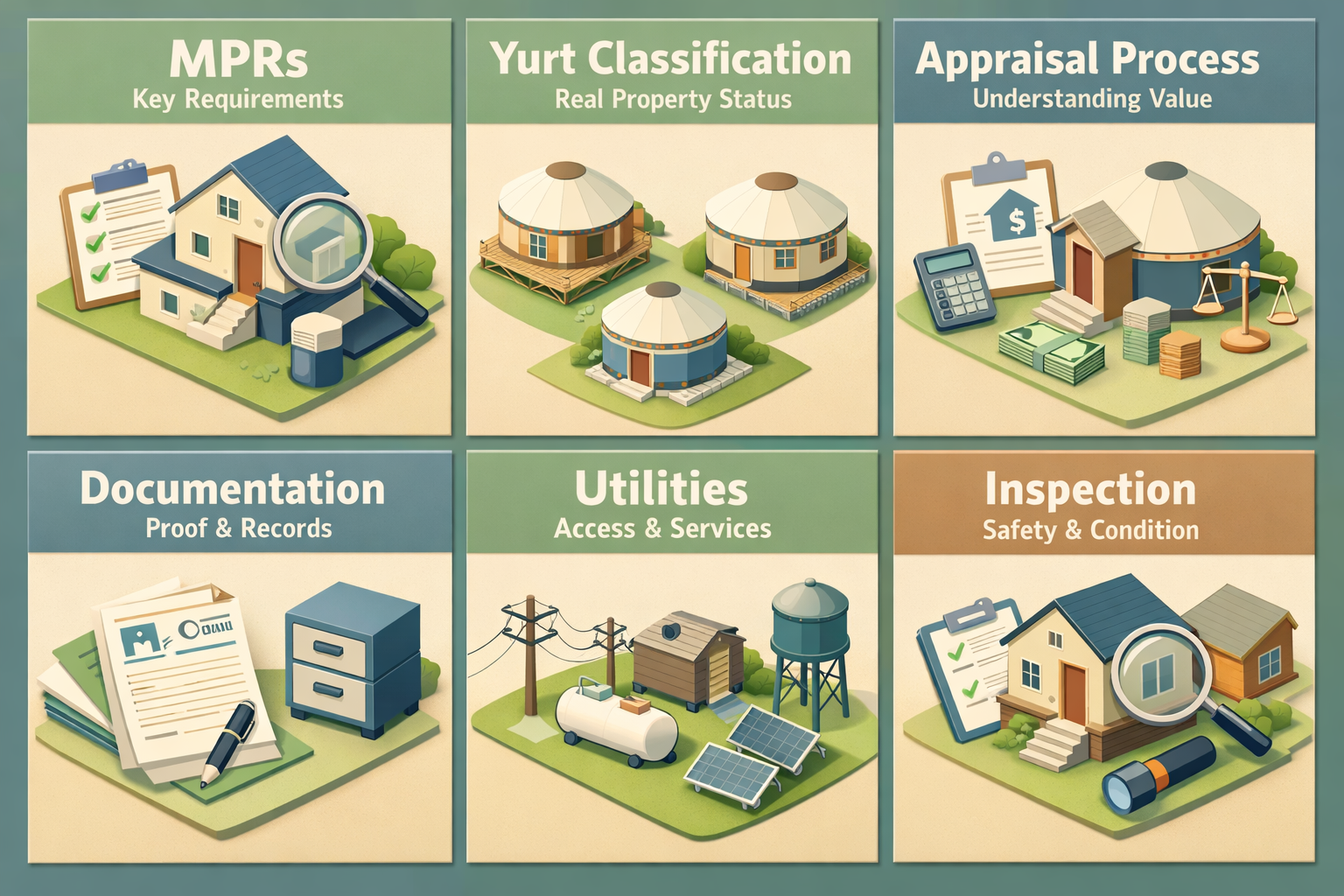

Understanding VA Minimum Property Requirements for Non-Traditional Homes

The VA's Minimum Property Requirements exist to protect both the veteran borrower and the government's financial interest. These requirements ensure the property is safe, structurally sound, and sanitary. For a traditional single-family home, meeting MPRs is usually straightforward. For a yurt — especially one that's off-grid — the evaluation becomes much more nuanced.

Key MPR areas that typically apply to any VA-financed property include:

- Structural integrity — the home must be structurally sound and free from hazards

- Roofing — the roof must be in good condition and able to protect the interior

- Heating — the home must have a heating system capable of maintaining at least 50°F in living areas

- Electrical and plumbing systems — must be functional and safe

- Water supply — access to potable water is required, whether through a municipal system or an approved well

- Sewage disposal — an approved waste disposal system is necessary

Off-grid yurts may rely on solar panels, rainwater collection, composting toilets, or propane heating. Some of these systems could satisfy MPRs if they meet local health and safety codes — but that determination often rests with the VA appraiser and the lender. There's no universal rule that says an off-grid system automatically passes or fails; much depends on how the property is built and documented.

The Core Challenge: How Lenders Classify Yurts as Real Property

One of the most significant barriers when exploring how to qualify for a VA loan with off-grid yurts involves property classification. For a VA loan to apply, the structure being financed must be considered real property — meaning it must be permanently affixed to land that the borrower owns or is purchasing.

Yurts present a classification problem. By design, traditional yurts are portable and non-permanent. Modern yurts built as permanent residences have made strides — some feature concrete foundations, full insulation, utility hookups, and permits — but they must meet specific criteria to be treated as real property:

- The yurt must be permanently attached to a foundation

- The land must be owned by the borrower (not leased)

- Local authorities must classify the structure as a dwelling under applicable building codes

- The property must be legally titled as real estate, not personal property

Without these elements in place, most lenders — and the VA itself — may decline to finance the structure. Even if a yurt is beautifully built and fully equipped, a lender's legal and appraisal teams will need documentation proving it qualifies under real property standards. This is a step many buyers underestimate.

VA Appraisals for Off-Grid Yurts: What to Expect

Every VA loan requires a VA appraisal conducted by a VA-approved appraiser. This isn't the same as a home inspection — it's an assessment of both the property's value and its compliance with the VA's MPRs. For off-grid living mortgage options, the appraisal stage is often where things get complicated.

VA appraisers use comparable sales — similar properties that have recently sold nearby — to determine market value. For a yurt on off-grid land, finding true comparables can be extremely difficult. If there are few or no similar properties that have sold in the area, the appraiser may struggle to assign a reliable value, which can delay or derail the loan entirely.

Additionally, the appraiser will evaluate whether the off-grid systems in place meet MPRs. Some considerations include:

- Solar power systems — may be acceptable if they reliably power the home, but backup systems could be required

- Well water — a water quality test is typically required to confirm potability

- Composting or alternative septic systems — must comply with local health codes and may require additional documentation or permits

- Propane or wood-burning heat — could satisfy heating requirements if properly installed and capable of maintaining required temperatures

Veterans should be prepared for the possibility that an appraiser may flag items that require repair or bring additional documentation before the loan can move forward. Working with a lender who has experience in rural or specialty properties may help reduce surprises at this stage.

Steps Veterans Can Take to Improve Their Approval Odds

While the path isn't simple, it's not necessarily a dead end either. Veterans who are serious about financing an off-grid yurt through a VA loan can take concrete steps to improve their approval odds.

- Confirm the yurt is legally classified as a dwelling. Obtain documentation from local authorities confirming the structure has a building permit and is recognized as a residential dwelling under local zoning laws.

- Ensure the yurt is permanently affixed. A concrete or engineered foundation, combined with utility hookups, significantly strengthens the case for real property classification.

- Own the land outright or purchase it simultaneously. VA loans generally cannot be used to finance structures on leased land. Including the land in the purchase is usually essential.

- Gather all system documentation. Have permits, installation records, and inspection reports ready for solar, water, and septic systems. The more documented the systems are, the easier it is for an appraiser to evaluate them.

- Work with a VA-experienced lender familiar with non-traditional properties. Not all lenders will even attempt to process a yurt loan. Finding one who has navigated specialty properties before can be a significant advantage.

- Consult a VA-approved appraiser early. A preliminary conversation with a VA appraiser familiar with rural properties may help identify issues before a formal appraisal is ordered.

Patience and preparation are key. Veterans who treat this like a standard purchase may find themselves frustrated. Approaching it as a specialty transaction — with all the documentation and expert guidance that implies — tends to yield better outcomes.

Exploring Alternative Financing When VA Loans Fall Short

In some cases, a VA loan simply may not be the right tool for an off-grid yurt purchase — at least not without significant upgrades to the property. When that's the case, veterans and other buyers interested in off-grid living mortgage options may want to explore alternative financing paths.

Some options worth considering include:

- Conventional portfolio loans — some lenders hold loans on their own books rather than selling them on the secondary market, which gives them flexibility to approve properties that don't meet standard guidelines

- USDA loans — for rural properties, the USDA Rural Development program may offer financing options, though similar MPR-style requirements apply

- Personal loans or construction loans — for buyers building a new yurt, a construction loan followed by a permanent mortgage might be possible if the finished structure meets real property standards

- Land loans combined with construction financing — purchasing the land separately and then financing construction could allow the buyer to build a yurt that meets all necessary codes before seeking permanent mortgage financing

- Non-QM (non-qualified mortgage) lenders — some specialty lenders work with borrowers and properties that fall outside conventional or government-backed guidelines

It's worth noting that alternative financing options often come with higher interest rates, larger down payment requirements, or shorter loan terms than a VA loan would offer. Veterans should weigh the full cost of each path before deciding which direction makes the most financial sense.

●Conclusion

Learning how to qualify for a VA loan with off-grid yurts requires a realistic understanding of both the VA's property requirements and the unique challenges that non-traditional structures present. It's not impossible — but it does demand more preparation, documentation, and persistence than a conventional home purchase. Veterans who take the time to ensure their yurt meets real property standards, gather all system documentation, and partner with experienced lenders will be in a much stronger position. If the VA loan path isn't available for a specific property, alternative financing options exist and may still make off-grid living achievable. At LoanWise, we're here to help you explore every option and find the financing solution that fits your goals. Reach out today to speak with a lending specialist who understands both VA programs and specialty property financing.