Filing for bankruptcy can feel like a financial reset button — and in many ways, it is. But if homeownership is one of your goals, you might be wondering whether a mortgage after bankruptcy is even possible. The good news is that it absolutely can be. While bankruptcy does create some hurdles, most loan programs have clearly defined waiting periods and qualification guidelines that allow borrowers to get back on track. With the right strategy and a bit of patience, buying a home after bankruptcy is a realistic and achievable goal for many people.

Understanding What Bankruptcy Means for Your Home Loan Journey

Bankruptcy is a legal process that provides individuals with relief from overwhelming debt. The two most common types for individuals are Chapter 7 and Chapter 13. Chapter 7 — often called "liquidation bankruptcy" — discharges most unsecured debts relatively quickly, typically within a few months. Chapter 13 involves a structured repayment plan that typically lasts three to five years before debts are discharged.

Each type affects your mortgage eligibility differently, mainly because lenders view them as carrying different levels of financial risk. Chapter 7 is generally seen as more severe since debts are wiped away without repayment, while Chapter 13 may be viewed more favorably because the borrower made an effort to repay creditors over time.

It's also worth noting that bankruptcy will remain on your credit report for several years — up to 10 years for Chapter 7 and up to 7 years for Chapter 13 — which could affect how lenders evaluate your application even after the mandatory waiting periods have passed. However, the negative impact on your credit score typically diminishes over time, especially if you're proactively rebuilding your financial profile.

Mandatory Waiting Periods by Loan Type

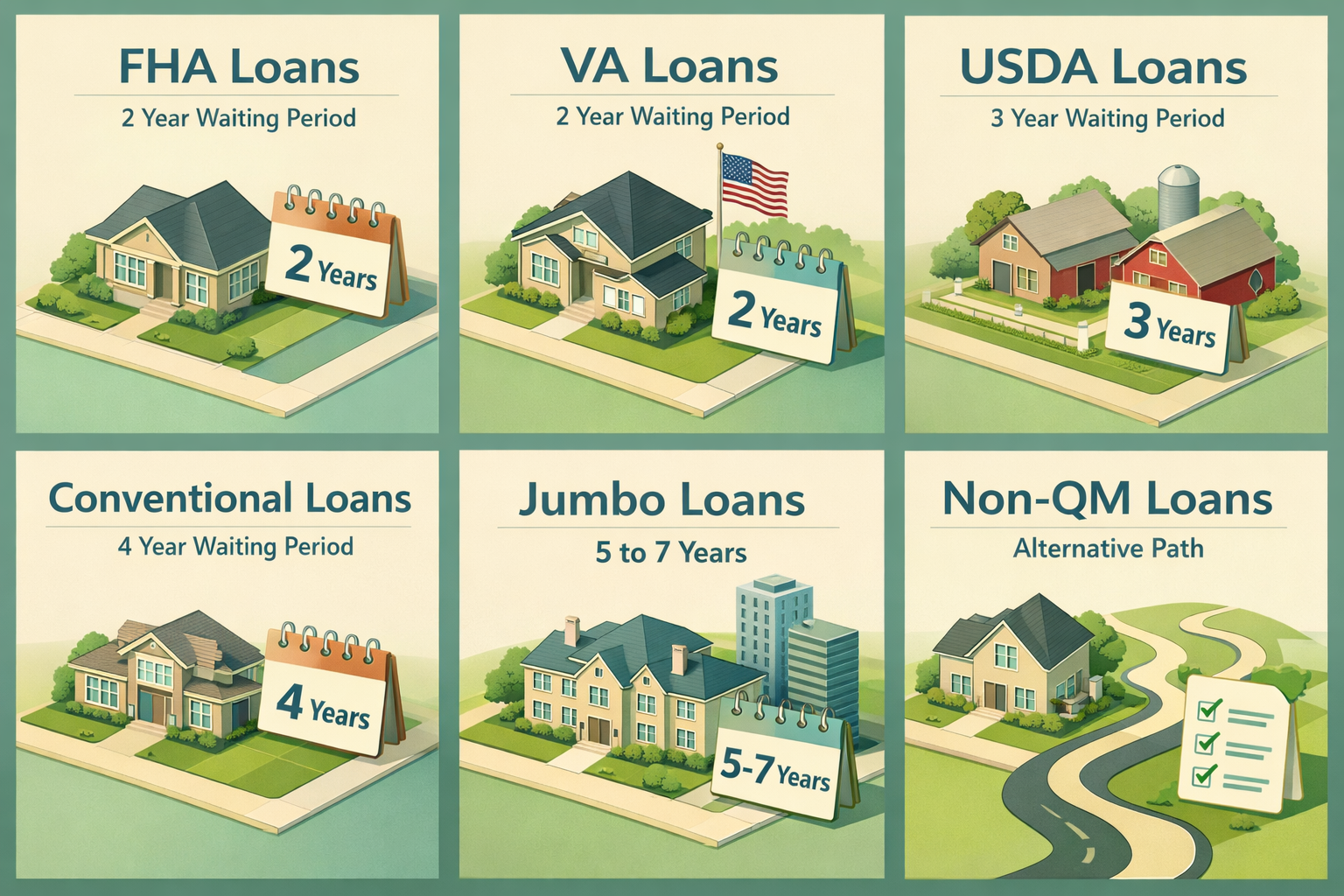

One of the most important things to understand when pursuing a mortgage after bankruptcy is that different loan programs enforce different waiting periods. These waiting periods begin from the date of your bankruptcy discharge or dismissal, not from the filing date. Here's a general overview of what most borrowers can expect:

- FHA Loans: Typically require a waiting period of 2 years after a Chapter 7 discharge. For Chapter 13, you may be eligible after 12 months of on-time repayment plan payments, with court approval.

- VA Loans: Generally require a 2-year waiting period after Chapter 7. For Chapter 13, eligibility may be possible after 12 months of satisfactory repayment.

- USDA Loans: Usually require a 3-year waiting period following a Chapter 7 discharge. Chapter 13 cases may allow earlier eligibility with consistent repayment history.

- Conventional Loans (Fannie Mae/Freddie Mac): Typically require a 4-year waiting period after Chapter 7 discharge and a 2-year waiting period after Chapter 13 discharge. These timelines may be shortened under extenuating circumstances.

- Jumbo Loans: Waiting periods are set by individual lenders and are often longer — sometimes 5 to 7 years — due to the higher loan amounts and stricter underwriting standards involved.

It's important to remember that these are general guidelines and individual lenders may apply additional overlays, meaning their own internal requirements could be stricter than the program minimums. Always consult directly with a lender to confirm current eligibility requirements.

Rebuilding Credit and Improving Your Financial Standing

The waiting period before you can qualify for a mortgage after bankruptcy isn't just about time passing — it's an opportunity to rebuild your financial foundation. Lenders will want to see that you've demonstrated responsible credit behavior since your discharge, so how you use this period matters significantly.

Steps to Strengthen Your Credit Profile

Here are some practical strategies that could help you become a stronger mortgage candidate during your waiting period:

- Open a secured credit card: Secured cards require a deposit but function like a regular card. Using one responsibly and paying the balance in full each month may help rebuild your credit score over time.

- Become an authorized user: Being added to a trusted family member's credit card account could give your score a positive boost, especially if that account has a long, clean payment history.

- Take out a credit-builder loan: Some banks and credit unions offer small loans specifically designed to help borrowers re-establish credit.

- Pay all bills on time: Payment history is one of the most significant factors in credit scoring models, so consistent on-time payments are essential.

- Keep credit utilization low: Try to use no more than 30% of your available credit limit at any given time.

- Monitor your credit report: Regularly reviewing your credit reports from all three major bureaus allows you to catch errors and track your progress.

The goal is to demonstrate to future lenders that the financial difficulties that led to bankruptcy are behind you, and that you've developed stronger money management habits since then.

Saving for a Down Payment and Meeting Lender Requirements

Beyond credit rebuilding, lenders will also evaluate other aspects of your financial profile when you apply for a qualify for a mortgage after bankruptcy. Two of the most important factors are your down payment and your debt-to-income (DTI) ratio.

Having a larger down payment can work in your favor by reducing the lender's risk and potentially offsetting concerns about your credit history. While FHA loans may allow down payments as low as 3.5% for eligible borrowers, a larger down payment — such as 10% or more — could strengthen your application and potentially help you secure better loan terms.

Your DTI ratio compares your monthly debt obligations to your gross monthly income. Most lenders prefer a DTI ratio below 43%, though some programs may be more flexible. In the time between your bankruptcy discharge and your mortgage application, it's wise to avoid taking on new significant debts such as car loans or personal loans unless absolutely necessary.

Building Reserves and Demonstrating Stability

Lenders may also look for evidence of financial stability beyond just your credit score and down payment. Having cash reserves — funds set aside in savings beyond your down payment and closing costs — can signal that you're better prepared to handle unexpected expenses. Employment stability is another key factor; lenders generally want to see at least two years of consistent employment history in the same field. If you're self-employed, you'll likely need to provide additional documentation such as tax returns and profit-and-loss statements.

Loan Programs Worth Exploring After Bankruptcy

Once you've completed the required waiting period and made meaningful progress on your financial recovery, it's time to explore which mortgage products might be the best fit for your situation. Each program has its own advantages depending on your credit profile, military status, location, and down payment resources.

FHA Loans: A Common Starting Point

FHA loans are government-backed mortgages insured by the Federal Housing Administration, and they're often among the first options considered by borrowers with past credit challenges. With relatively accessible credit score requirements and low down payment options, FHA loans may be a practical entry point for many post-bankruptcy homebuyers. Keep in mind that FHA loans require mortgage insurance premiums, which will add to your monthly costs.

VA Loans: A Strong Option for Veterans

If you're a veteran, active-duty service member, or eligible surviving spouse, a VA loan could offer significant benefits — including no down payment requirement and no private mortgage insurance. The VA's relatively shorter waiting period after bankruptcy makes this a program worth exploring for those who qualify.

Non-QM Loans: An Alternative Path

Non-qualified mortgage (Non-QM) loans are offered by some lenders outside the standard Fannie Mae and Freddie Mac guidelines. These products may accommodate borrowers with recent bankruptcy on their record, though they often come with higher interest rates and fees to compensate for the additional risk. Non-QM loans could be worth exploring if you don't yet meet the waiting period requirements of conventional programs, but it's important to carefully evaluate the total cost of borrowing before committing.

Working With the Right Lender and Setting Realistic Expectations

Not all lenders approach post-bankruptcy applications the same way. Some lenders may be more experienced in working with borrowers who have complex credit histories, while others may apply stricter internal overlays that go beyond program minimums. Shopping around and comparing multiple lenders is particularly important in this situation.

Here are a few tips to help you navigate the lender selection process:

- Ask about lender overlays: Confirm whether a lender's in-house requirements are stricter than the loan program's official guidelines.

- Get pre-qualified first: A pre-qualification can give you a realistic sense of where you stand before submitting a full application.

- Be transparent about your history: Attempting to hide or downplay your bankruptcy will only create problems later in the underwriting process. Lenders appreciate honesty and can often provide guidance based on your specific circumstances.

- Work with a mortgage broker: A knowledgeable broker may have access to multiple lenders and can help match you with options that are well-suited to your situation.

It's also wise to set realistic expectations about interest rates. Borrowers with bankruptcy on their record may receive slightly higher rates than borrowers with clean credit histories, at least initially. Over time, as your credit improves and you build equity in your home, refinancing to a better rate may become an option.

●Conclusion

Pursuing a mortgage after bankruptcy requires patience, planning, and a commitment to rebuilding your financial health — but it's far from impossible. By understanding the waiting periods that apply to different loan programs, actively working to strengthen your credit, saving strategically, and working with lenders who have experience in this area, you can position yourself for homeownership success. The path may take a little longer, but many borrowers have walked it before you and come out the other side as proud homeowners. If you're ready to start exploring your options, speaking with a qualified mortgage professional is a great first step.