Running a small business takes grit, creativity, and — more often than not — outside funding. But what happens when your credit score isn't exactly where lenders want it to be? Many entrepreneurs assume that a poor credit history means the door to financing is permanently closed. The good news is that's not necessarily true. Understanding how to get a business loan with bad credit is a matter of knowing where to look, what to prepare, and how to position your business as a worthwhile investment. This guide walks you through every important step, from exploring alternative lending options to actively rebuilding your creditworthiness over time.

What Counts as Bad Credit for a Business Loan?

Before diving into solutions, it helps to understand how lenders define "bad credit." Most traditional lenders — such as banks and credit unions — typically look for a personal credit score of 680 or higher when evaluating small business loan applications. Some may require even higher scores for larger loan amounts or longer terms. A score below 580 is generally considered poor, while scores between 580 and 669 fall into the "fair" range.

It's worth noting that lenders don't only look at your personal credit score. They may also review your business credit score, which is reported by bureaus like Dun & Bradstreet, Experian Business, and Equifax Business. A low score on either report could affect your approval odds and the interest rates you're offered.

That said, credit score thresholds vary by lender type and loan product. Alternative lenders and online financing platforms often work with borrowers who have scores well below what traditional banks require. So while a low score may limit some options, it's unlikely to eliminate all of them.

Why Traditional Banks May Not Be Your Best Starting Point

If you have a poor credit score, walking into a traditional bank and applying for a term loan may lead to a quick rejection. Banks tend to follow strict underwriting guidelines, and credit history plays a significant role in their decision-making process. They're also more likely to require collateral, several years of business tax returns, and detailed financial projections before even considering your application.

This doesn't mean banks are off the table entirely. Some community banks and nonprofit lending institutions are more flexible and mission-driven. However, for most small business owners and entrepreneurs with business loans for poor credit score needs, the traditional banking route can be slow, demanding, and often discouraging.

The key takeaway here is that knowing your options upfront saves time and energy. Rather than spending weeks pursuing a loan that's unlikely to be approved, you can direct your efforts toward lenders and products that are genuinely designed for your situation.

Exploring Alternative Lenders for Bad Credit Business Loans

One of the most significant shifts in small business lending over the past decade has been the rise of alternative lenders for bad credit business loans. These include online lenders, fintech platforms, peer-to-peer lending networks, and Community Development Financial Institutions (CDFIs). Each comes with its own set of requirements, but many are more willing to look beyond your credit score.

Here's a closer look at some of the most common alternative financing options available to small business owners with poor credit:

- Online term loans: Platforms like those offered through fintech lenders may approve borrowers with lower credit scores if the business demonstrates strong cash flow and consistent revenue history.

- Merchant cash advances (MCAs): These are advances against your future sales revenue. Repayment is typically tied to a percentage of daily card sales, making them flexible but often expensive.

- Invoice financing: If your business invoices clients, you may be able to use those unpaid invoices as collateral to access funds quickly — often with less emphasis placed on your credit score.

- Microloans: Organizations like the U.S. Small Business Administration (SBA) offer microloan programs through nonprofit intermediaries. These loans are typically smaller in size but may be accessible to borrowers with limited or damaged credit histories.

- CDFIs: Community Development Financial Institutions are mission-driven lenders that prioritize underserved business owners, including those with poor credit or limited access to traditional banking.

It's important to compare the total cost of borrowing across these options. Alternative lenders often carry higher interest rates and fees than traditional bank loans, which could affect your long-term cash flow. Always review the annual percentage rate (APR), repayment terms, and any prepayment penalties before signing.

Secured vs. Unsecured Business Loans for Bad Credit Borrowers

When your credit score is low, lenders may be more willing to work with you if you can offer some form of security. That's where the distinction between secured and unsecured business loans for bad credit becomes particularly important.

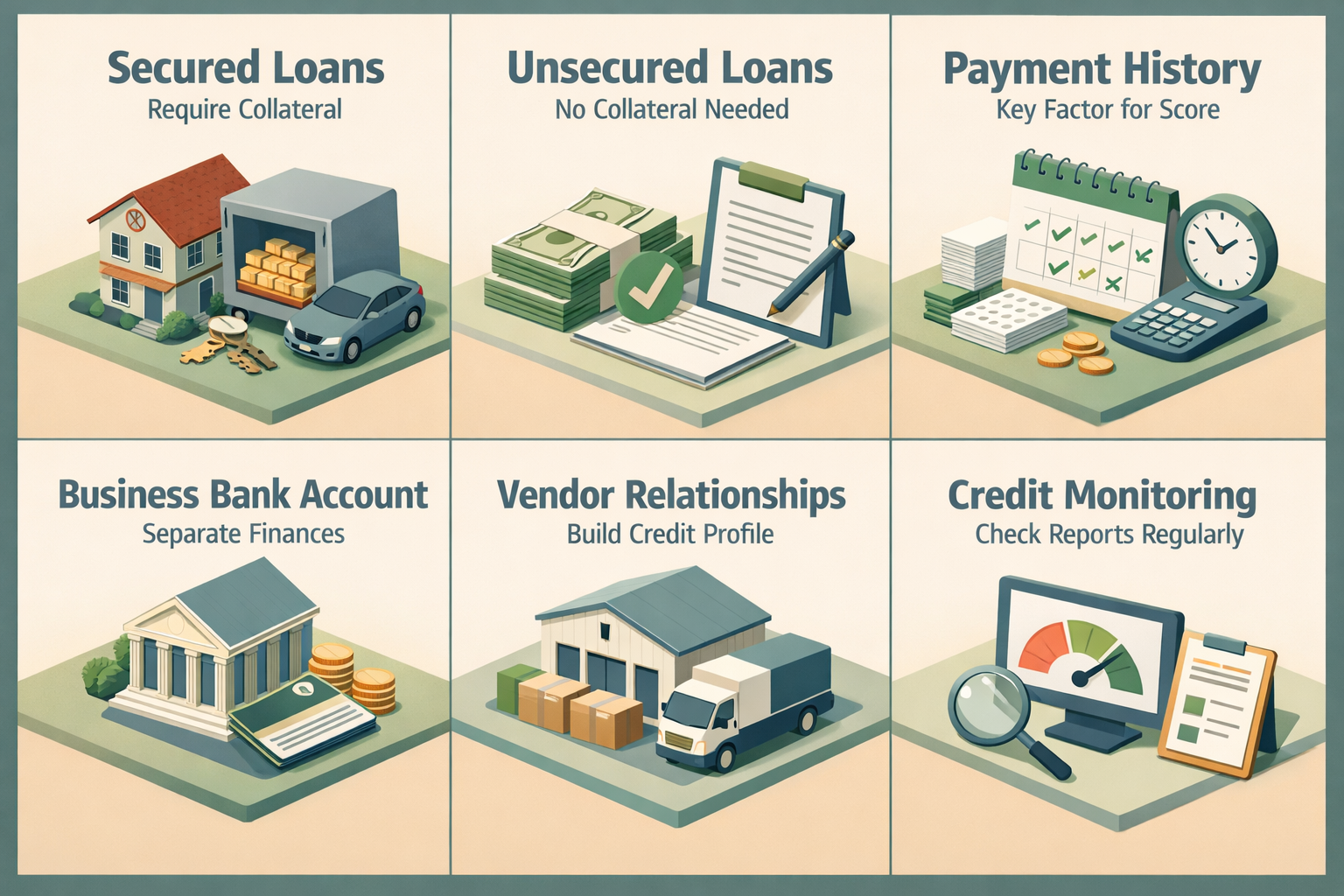

Secured loans require you to pledge an asset — such as equipment, inventory, real estate, or accounts receivable — as collateral. If you default on the loan, the lender has the right to seize that asset. Because this reduces the lender's risk, secured loans may come with lower interest rates and higher borrowing limits, even for applicants with poor credit.

Unsecured business loans, on the other hand, don't require collateral. They rely more heavily on your creditworthiness and financial history. For borrowers with bad credit, unsecured loans can be harder to qualify for and may come with stricter terms or higher costs. However, they're still available through certain online lenders and alternative financing platforms, especially if your business has strong monthly revenue.

Some lenders may also ask for a personal guarantee, which means you agree to be personally liable for the debt if your business can't repay it. This is common even with unsecured business loans for borrowers who present higher risk, so it's worth understanding what you're agreeing to before accepting any offer.

How to Strengthen Your Application Before Applying

Even if you can't improve your credit score overnight, there are practical steps you can take to make your loan application more compelling. Lenders evaluate multiple factors beyond just your credit score, and a strong application can sometimes offset a weaker credit history.

- Organize your financial documents: Prepare at least three to six months of bank statements, profit and loss statements, and any existing business tax returns. Lenders want to see that your business generates real, consistent income.

- Show steady cash flow: If your revenue is stable or growing, highlight that clearly. Many alternative lenders place heavy weight on cash flow when making lending decisions for borrowers with poor credit.

- Write a clear business plan: A concise, well-organized business plan that outlines how you'll use the loan and how you plan to repay it can significantly strengthen your application — especially with mission-driven lenders and CDFIs.

- Offer collateral where possible: As mentioned earlier, secured loans may be easier to access with poor credit. If you have business assets you're willing to pledge, this could improve your chances.

- Find a co-signer or guarantor: Some lenders may accept a creditworthy co-signer who agrees to be responsible for the loan if you default. This can open doors that might otherwise be closed.

- Apply for an amount you can realistically repay: Requesting a loan amount that aligns with your current revenue and repayment capacity signals financial responsibility to lenders.

Taking these steps before you submit an application shows lenders that you're serious, organized, and aware of your financial situation — all of which can work in your favor.

Improving Your Business Credit Score for Future Loan Opportunities

If you're not in an immediate rush for funding, investing time in improving your business credit score for loans could pay off significantly in the long run. A better score means access to more lenders, lower interest rates, and more favorable repayment terms.

Here are some practical ways to build or repair both your personal and business credit over time:

- Pay existing debts on time: Payment history is one of the most influential factors in your credit score. Even small, consistent payments on current obligations can begin to shift your score upward.

- Separate your business and personal finances: Open a dedicated business bank account and apply for a business credit card if you haven't already. This helps establish an independent business credit profile.

- Register your business with credit bureaus: Many small businesses don't realize they need to actively register with business credit reporting agencies. Setting up a DUNS number through Dun & Bradstreet, for example, is a starting point for building a business credit file.

- Work with vendors that report to credit bureaus: Some suppliers and vendors offer net-30 or net-60 payment terms and report those payments to business credit bureaus. Using these trade lines responsibly can help build your credit profile.

- Monitor your credit reports regularly: Errors on credit reports are more common than many people realize. Checking both your personal and business reports regularly allows you to dispute inaccuracies that may be dragging your score down unnecessarily.

Credit improvement is a gradual process, but even modest gains over a few months can expand your lending options considerably. It's worth treating credit repair as an ongoing part of your broader financial strategy.

●Conclusion

Knowing how to get a business loan with bad credit starts with accepting where you are financially and then making informed, strategic decisions from that point forward. A low credit score may narrow your options with traditional banks, but it doesn't eliminate them entirely. Between alternative lenders, secured loan products, microloans, and invoice financing, there are more pathways to small business funding than many entrepreneurs realize. At the same time, taking proactive steps — organizing your financials, strengthening your application, and steadily rebuilding your credit — positions your business for better opportunities down the road. If you're ready to explore your financing options, LoanWise can help you connect with lenders who understand your situation and are equipped to work with you.