If you earn most of your pay through commissions, bonuses, or variable income, you already know that your paycheck can look very different from month to month. That's exciting when business is booming — but it can feel like a hurdle when you're trying to buy a home. The good news is that lenders have established ways to evaluate non-traditional income, and understanding how the process works can put you in a much stronger position. This guide walks through how to calculate mortgage affordability with commission income, what lenders are really looking for, and how to position yourself for approval — even on a jumbo loan.

Why Commission Income Is Treated Differently by Mortgage Lenders

Most salaried borrowers can hand over a few pay stubs and call it a day. Commission earners, however, face a more detailed review. Lenders treat variable income differently because there's no guarantee that this month's commission check will match next month's. To manage that risk, underwriters typically look for a pattern of earnings over time rather than relying on a single paycheck.

This approach applies to a wide range of professionals — real estate agents, financial advisors, pharmaceutical sales reps, auto dealers, independent contractors, and many others who earn based on performance. Even if your annual income is substantial, the variability in how it arrives can trigger additional scrutiny during the loan underwriting process.

The core concern for lenders is consistency. They want to feel confident that you can make your mortgage payment not just this month, but reliably over the life of the loan. That's why income verification for commission earners often involves a more thorough document review than a standard W-2 employee would face.

How Lenders Calculate Qualifying Income for Commission Earners

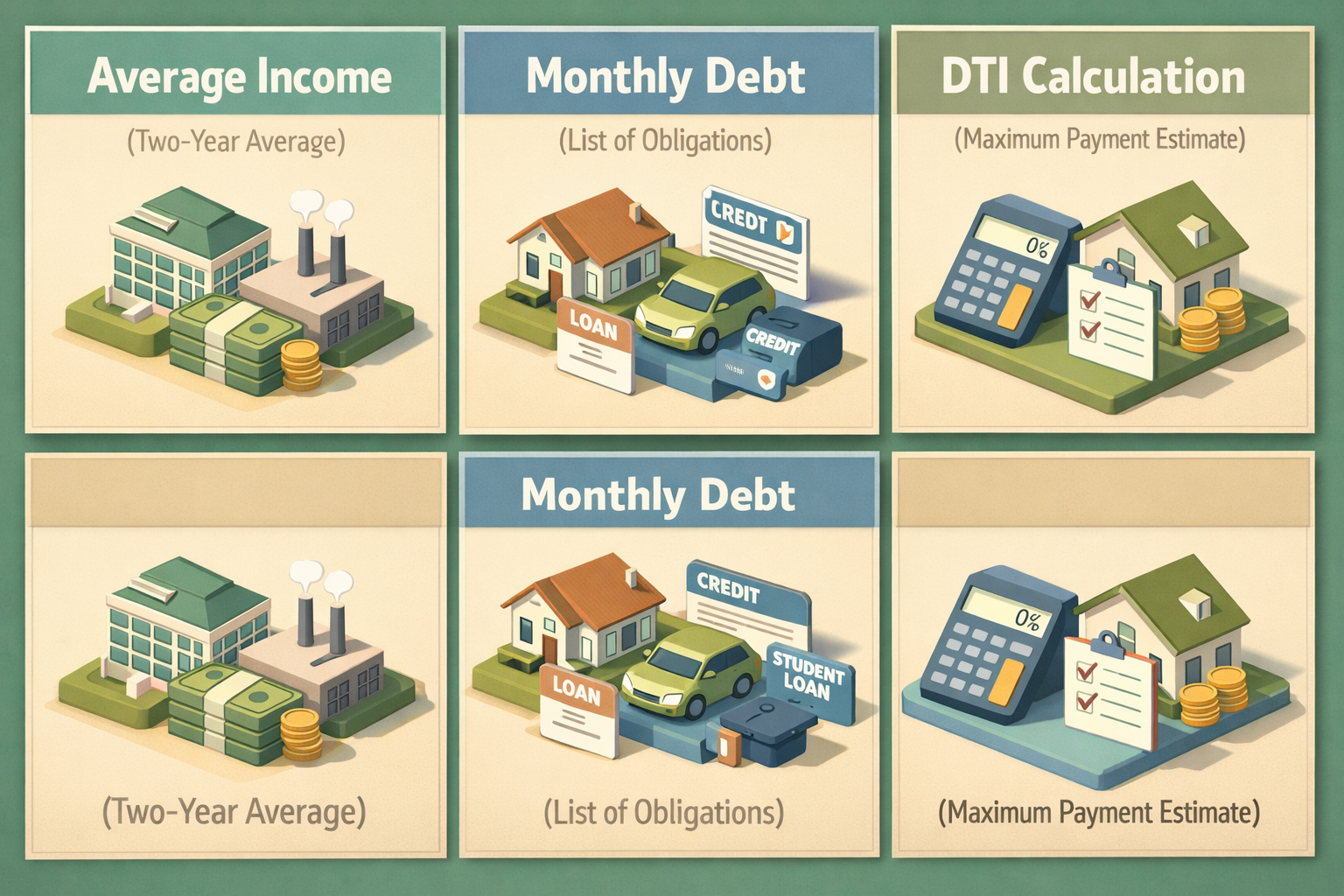

When a lender evaluates commission income, they typically average it over a two-year period. This means your qualifying income is generally the average of what you've earned in commissions over the past 24 months — not your current monthly high or what you expect to earn next quarter.

For example, if you earned $90,000 in commissions last year and $110,000 the year before, a lender would likely use $100,000 as your annual qualifying income, or roughly $8,333 per month. From there, they apply standard debt-to-income (DTI) ratio guidelines to determine how much mortgage payment you can reasonably carry.

The Debt-to-Income Ratio and What It Means for You

Your debt-to-income ratio compares your monthly debt obligations — including the proposed mortgage payment — to your gross monthly qualifying income. Most conventional loan programs prefer a DTI at or below 43%, though some lenders may allow slightly higher ratios depending on compensating factors like strong credit or significant reserves. If your qualifying income is averaged lower than your peak earnings, this ratio can tighten quickly, so it's worth running the numbers before you start shopping for homes.

To get a rough estimate of your affordability, multiply your average monthly qualifying income by your lender's maximum DTI (often 43%), then subtract your existing monthly debt payments. The remainder is the maximum monthly mortgage payment a lender may approve. From there, you can use a mortgage calculator to back into a purchase price, factoring in today's interest rates, your expected down payment, and property taxes.

Key Documents You'll Need for Income Verification as a Commission Earner

Being prepared with the right paperwork can make a significant difference in how smoothly your mortgage application moves through underwriting. Lenders generally require a more comprehensive document package from commission-based borrowers compared to salaried employees.

- Two years of federal tax returns (personal and business, if applicable): Lenders use these to verify your reported income and identify any write-offs that could reduce your qualifying figure.

- Two years of W-2s or 1099 forms: These confirm the sources and consistency of your commission income over time.

- Recent pay stubs (typically the last 30 days): These show your current year-to-date earnings and help lenders assess whether income is trending upward or downward.

- Employer verification letter: Some lenders request a letter confirming your employment status, position, and that your commission-based arrangement is expected to continue.

- Bank statements (typically two to three months): These help verify that your stated income is actually landing in your accounts and that you have sufficient reserves.

If your income has been increasing year over year, lenders may view that positively. However, if it's been declining, some underwriters may use the lower figure or require additional explanation. Consistency and an upward trend tend to work in your favor.

How to Calculate Mortgage Affordability with Commission Income Step by Step

Understanding how to calculate mortgage affordability with commission income doesn't require a finance degree — but it does require a few key inputs. Here's a practical step-by-step approach you can use before speaking with a lender.

Step 1 — Average Your Commission Income

Add up your total gross commission income from the last two full calendar years, then divide by 24 to get your average monthly qualifying income. Use your tax returns as the source of truth, since lenders will do the same.

Step 2 — Identify Your Monthly Debt Load

List all recurring monthly debt obligations: student loans, car payments, credit card minimums, and any other installment or revolving debt. Do not include utilities or living expenses — lenders focus on credit-reported debts.

Step 3 — Apply the DTI Formula

Multiply your average monthly qualifying income by 0.43 (for a 43% DTI ceiling). Subtract your existing monthly debts. The result is the approximate maximum mortgage payment — including principal, interest, taxes, and insurance — that a lender may allow.

Step 4 — Use a Mortgage Calculator

With your estimated maximum monthly payment in hand, plug it into a mortgage calculator along with current interest rates and your intended down payment. This will give you a realistic home purchase price range to work with. Keep in mind that property taxes, homeowners insurance, and any HOA fees will reduce the loan amount you can actually carry.

Step 5 — Account for Reserves

Lenders often require commission earners to have additional cash reserves — sometimes six to twelve months of mortgage payments — readily available in a verifiable account. Factor this into your overall financial planning before making an offer.

Qualifying for a Jumbo Loan When Your Income Comes from Bonuses and Commissions

For borrowers targeting higher-priced properties, a jumbo loan for variable income borrowers may be the path forward. Jumbo loans — those that exceed conforming loan limits set by the Federal Housing Finance Agency — come with their own set of stricter requirements, and lenders tend to apply even more scrutiny to income documentation when the loan amount is large.

That said, many high-earning commission professionals are excellent candidates for jumbo financing. Successful salespeople, executives with performance bonuses, and senior financial professionals often have the income profile and asset base that jumbo lenders want to see. The key is presenting that income in a way that lenders can clearly verify and feel confident about.

How Bonus Income Factors Into Jumbo Underwriting

When qualifying for a jumbo loan with bonuses, lenders typically apply the same two-year averaging rule. Bonus income is usually counted only if it has been received consistently for at least two years and there's a reasonable expectation it will continue. A one-time bonus, even a large one, may not be counted in full — or at all — depending on the lender's guidelines.

Credit score requirements for jumbo loans tend to be higher than conventional loans, often starting around 700 or above, though specific thresholds vary by lender. Down payment requirements are also typically larger, with many jumbo programs requiring at least 10% to 20% down depending on loan size and borrower profile. Reserves requirements can be particularly rigorous — some jumbo lenders want to see 12 months or more of mortgage payments sitting in liquid accounts.

Self-Employed Commission Earners and Specialized Mortgage Options

If you're self-employed and earn through commissions or 1099 income, your mortgage path may look a little different. Self-employed borrowers often take advantage of legitimate tax deductions that reduce their taxable income — which is great for tax purposes, but can make qualifying for a mortgage more challenging when lenders use your net income rather than gross.

This is where a self-employed jumbo mortgage calculator becomes particularly useful. These tools are designed to help self-employed borrowers estimate their qualifying income after accounting for business deductions, depreciation, and other adjustments that lenders may add back to arrive at a usable income figure.

Bank Statement Loans and Non-QM Programs

For self-employed commission earners who struggle to qualify under conventional income documentation rules, non-qualified mortgage (non-QM) programs may offer a viable alternative. Bank statement loans, for example, allow lenders to calculate qualifying income based on 12 to 24 months of bank deposits rather than tax returns. This can be particularly helpful if your tax returns show significantly less income than what actually flows through your accounts.

These programs may carry slightly higher interest rates compared to conventional or conforming loans, reflecting the additional flexibility in underwriting. However, for borrowers with strong credit, meaningful assets, and a solid deposit history, they can open doors that standard programs might keep closed. Working with a lender experienced in non-QM or specialty mortgage programs is often worth the extra effort for self-employed and commission-based borrowers.

Strategies to Strengthen Your Mortgage Application as a Commission Earner

The good news is that there are concrete steps you can take to improve your standing as a commission-based borrower before you apply for a mortgage affordability assessment. These strategies won't happen overnight, but planning ahead — even six to twelve months in advance — can meaningfully improve your outcome.

- Maintain clean, consistent tax returns: If possible, work with an accountant to optimize your returns without reducing your qualifying income more than necessary. Some deductions may save you less in taxes than they cost you in borrowing power.

- Build substantial reserves: Having six to twelve months of mortgage payments in savings is not just a lender requirement — it also demonstrates financial stability and can serve as a compensating factor that offsets income variability concerns.

- Pay down existing debts: Reducing your DTI by eliminating credit card balances or paying off installment loans can directly increase the mortgage amount you qualify for.

- Protect your credit score: Commission earners benefit from strong credit just like any other borrower, and often more so. Avoid opening new credit accounts in the months before you apply, and monitor your credit report for errors.

- Document everything thoroughly: Keep organized records of your earnings, contracts, commission agreements, and any employer correspondence that confirms your income arrangement is ongoing.

- Work with a lender experienced in variable income: Not all lenders handle commission income the same way. A lender who understands the nuances of how to calculate mortgage affordability with commission income can make a significant difference in how your application is evaluated.

●Conclusion

Commission income doesn't disqualify you from homeownership — it simply means the path to approval may require a bit more preparation and documentation. By understanding how lenders average variable income, what they look for in a borrower's financial profile, and how jumbo and non-QM programs might expand your options, you're already better equipped to navigate the mortgage process with confidence. Whether you're a first-time buyer, moving up to a larger home, or exploring a high-value property purchase, taking the time to organize your income documentation and strengthen your overall financial picture can make a real difference. LoanWise is here to help you find the right lending solution for your unique income situation — reach out to one of our mortgage specialists today to get started.