Construction Mortgage Loan Investment Guide

Real estate investors looking to expand their portfolios into new construction projects face unique financing challenges that differ significantly from traditional rental property acquisitions. A mortgage loan for construction provides the specialized funding structure needed to finance ground-up developments, major renovations, and strategic property improvements that can substantially increase investment returns.

Unlike conventional investment property loans, construction financing typically involves variable interest rates during the building phase, followed by conversion to permanent financing. This dual-phase approach requires investors to understand both the construction loan requirements and the long-term mortgage implications for their investment strategy.

The construction lending landscape offers several pathways for savvy investors, from traditional construction-to-permanent loans to government-backed programs that might reduce upfront costs and streamline the approval process.

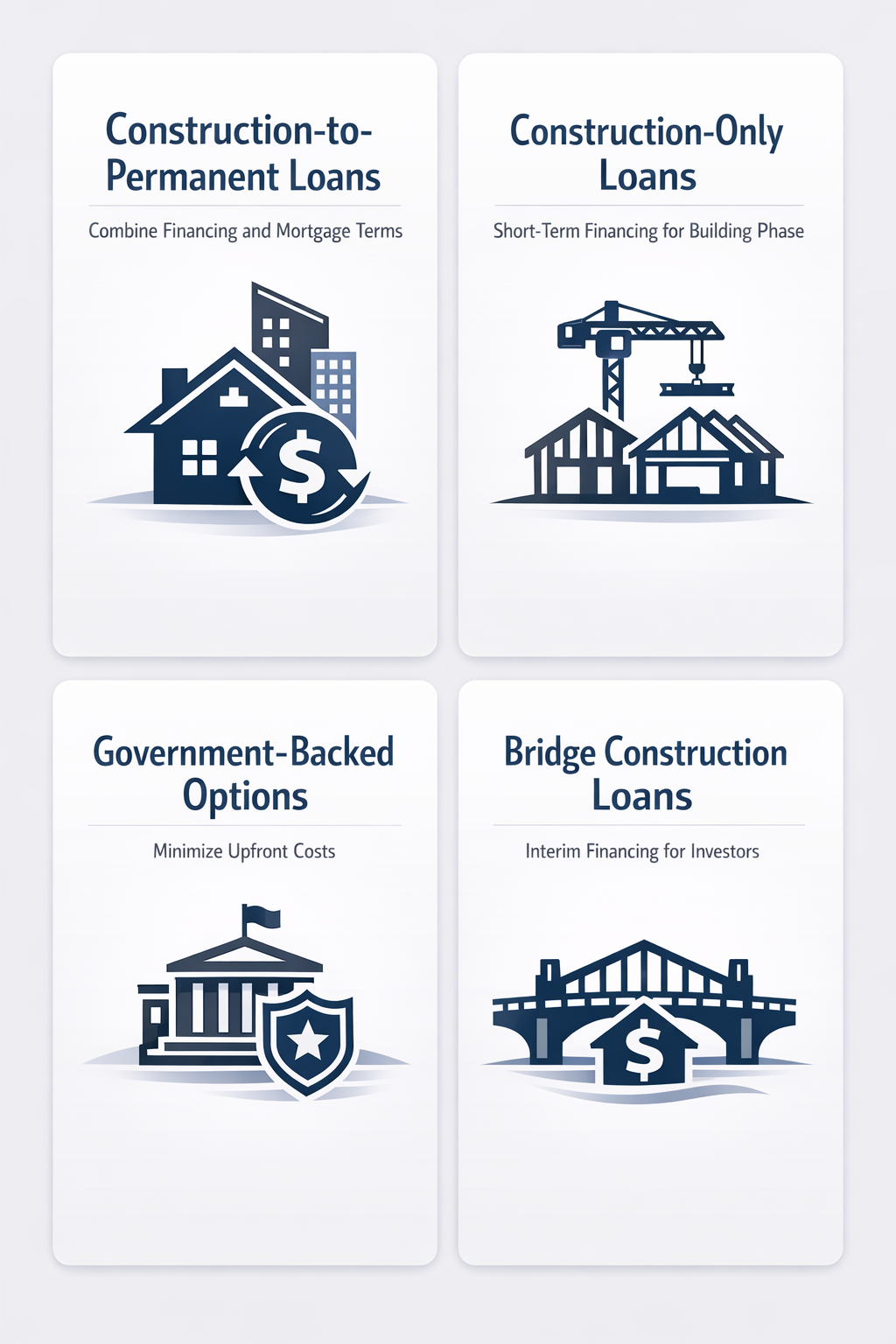

Core Construction Loan Types for Investors

Understanding the various construction loan types available helps investors select the most appropriate financing structure for their specific project needs and investment goals.

- Construction-to-Permanent Loans: These loans combine construction financing with permanent mortgage terms, eliminating the need for multiple closings and potentially reducing transactional costs while enhancing strategic long-term property investment planning.

- Construction-Only Loans: Short-term financing that covers the building phase only, requiring separate permanent financing upon completion, which may offer more flexibility for investors planning to sell immediately after construction.

- Government-Backed Options: Programs like FHA One-Time Close loans can minimize investor upfront costs and simplify the funding process for single-unit projects, though these typically focus on owner-occupied properties.

- Bridge Construction Loans: Specialized products that provide interim financing for investors who need to begin construction before selling existing properties or securing long-term financing.

Credit Requirements and Financial Qualifications

Construction loan approval standards typically exceed those of traditional investment property financing, requiring investors to demonstrate both creditworthiness and project viability.

- Credit Score Thresholds: A credit score of 680 is typically needed to secure a construction loan, though investors should aim for a credit score of 700 or higher for the best construction loan rates and terms.

- Down Payment Requirements: Construction loans often require larger down payments than conventional mortgages, with 20-30% being common for investment properties, though some government-backed programs may offer reduced credit requirements.

- Cash Flow Verification: Lenders typically require extensive documentation of income sources, existing property performance, and liquid reserves to cover potential cost overruns during construction.

- Construction Experience: Many lenders prefer working with investors who have previous construction or major renovation experience, or require partnership with qualified general contractors.

Interest Rate Structures and Cost Considerations

Construction loan interest rates and fee structures differ substantially from traditional mortgage products, requiring careful financial planning and cash flow management throughout the project timeline.

- Variable Rate Periods: Most construction loans feature variable interest rates during the building phase, typically tied to prime rate plus a margin, which can impact project profitability if rates rise during construction.

- Interest-Only Payments: During construction, investors typically make interest-only payments on funds actually drawn, rather than the full loan amount, which can help manage cash flow during the building period.

- Conversion Rate Terms: Construction-to-permanent loans may lock in the permanent mortgage rate at closing or at conversion, affecting long-term investment returns and refinancing strategies.

- Additional Fee Structures: Construction loans often include inspection fees, draw fees, and other costs that traditional mortgages don't carry, requiring careful budget planning for total project costs.

Strategic Project Planning for Maximum Returns

Successful construction loan utilization requires comprehensive project planning that aligns financing terms with investment objectives and market conditions.

- Timeline Coordination: Construction loan terms typically range from 6-12 months, requiring realistic scheduling that accounts for potential delays while avoiding costly extensions that can erode investment returns.

- Cost Control Systems: Implementing detailed budgeting and change order management helps prevent cost overruns that could exceed loan amounts or require additional out-of-pocket investment.

- Market Timing Analysis: Construction projects should align with local market cycles, ensuring completion during favorable selling or rental conditions to maximize investment outcomes.

- Exit Strategy Planning: Whether planning to sell immediately, convert to rental property, or refinance into long-term investment financing, having clear exit strategies helps optimize loan selection and project execution.

Building a Home Loan Process Navigation

The building a home loan process involves multiple stages that require careful coordination between investors, lenders, and construction teams to ensure smooth project execution.

- Pre-Approval and Planning: Investors must secure loan pre-approval, finalize construction plans, obtain permits, and select qualified contractors before accessing construction funds, establishing a solid foundation for project success.

- Draw Schedule Management: Construction loans typically disburse funds in predetermined stages based on completion milestones, requiring investors to coordinate with contractors and lenders to ensure timely fund availability throughout the project.

- Inspection and Compliance: Regular lender inspections verify construction progress and code compliance before releasing each draw, making quality control and timeline adherence critical for maintaining project momentum and avoiding delays.

Portfolio Integration and Scaling Strategies

Integrating construction projects into existing real estate investment portfolios requires strategic planning to optimize returns while managing increased complexity and risk exposure.

- Risk Distribution Methods: Experienced investors often limit construction projects to a specific percentage of their total portfolio, maintaining diversification across different property types and investment strategies to minimize overall risk exposure.

- Capital Allocation Planning: Construction projects typically require more active management and higher cash reserves than traditional rental properties, necessitating careful planning around existing property cash flows and available investment capital.

- Scaling Timeline Development: Investors may start with smaller construction projects to develop expertise and lender relationships before pursuing larger developments, building both experience and credibility in the construction lending market.

Long-Term Investment Considerations

Construction loan decisions should align with broader investment strategies and long-term portfolio objectives. Successful investors typically evaluate construction opportunities within the context of their overall investment timeline, risk tolerance, and market expertise. The specialized nature of construction financing requires ongoing education and relationship building with experienced lenders who understand real estate investors needs and project requirements.

●Conclusion

A mortgage loan for construction opens significant opportunities for real estate investors willing to navigate the additional complexity and requirements of development financing. Success depends on thorough preparation, realistic project planning, and selecting the right loan structure for each specific investment scenario.

While construction loans require higher credit standards and more extensive documentation than traditional investment property financing, they provide access to potentially higher returns through value-add strategies and new development opportunities. Investors who master construction financing often find it becomes a valuable component of their overall investment approach.

Working with experienced construction lenders who understand real estate investment objectives can streamline the process and provide ongoing support throughout project execution, helping investors achieve their development goals while maintaining portfolio growth and profitability.