Understanding Mortgage for a Second Home Financing Options

Real estate investors increasingly turn to second home properties as a strategic way to diversify their portfolios and generate additional income streams. Whether you're targeting vacation rental markets or planning long-term appreciation plays, securing a mortgage for a second home requires careful planning and understanding of specific lending requirements.

The financing landscape for second homes differs significantly from traditional investment properties, offering unique opportunities for savvy investors. With minimum down payment requirements typically starting at 10% and various loan products available, investors can leverage these properties to expand their real estate holdings while potentially benefiting from personal use during off-seasons.

Step-by-Step Second Home Mortgage Application Process

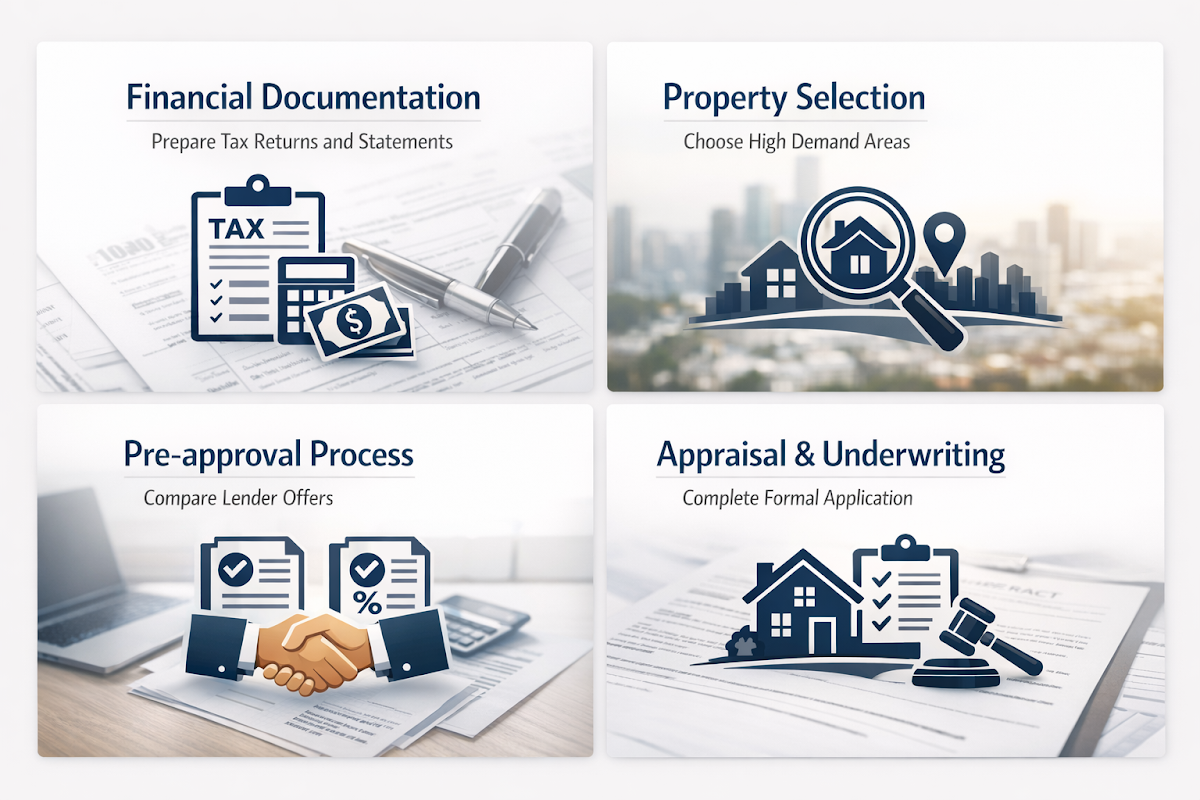

The step-by-step second home mortgage application process requires methodical preparation and documentation to ensure successful approval. Understanding each phase helps investors navigate the complexities and avoid common pitfalls that could delay or derail their financing.

- Financial Documentation Preparation: Gather two years of tax returns, bank statements, investment property income records, and current debt obligations. Lenders typically require comprehensive financial documentation to assess your ability to service multiple property loans simultaneously.

- Property Selection and Market Analysis: Choose properties in markets with strong rental demand or appreciation potential. Consider factors like seasonal occupancy rates, local regulations affecting short-term rentals, and proximity to amenities that attract vacationers or long-term tenants.

- Pre-approval and Rate Shopping: Obtain pre-approval letters from multiple lenders to compare second home mortgage rates and terms. Different lenders may offer varying programs, so exploring options helps secure the most favorable financing structure for your investment strategy.

- Property Appraisal and Underwriting: Complete the formal application process including professional appraisal and underwriter review. Be prepared for potentially longer processing times compared to primary residence mortgages, as lenders conduct additional due diligence for second home loans.

Essential Down Payment Requirements for Second Home Financing

Down payment requirements for a second home typically demand more capital upfront compared to primary residences, making financial planning crucial for real estate investors. The minimum threshold generally starts at 10%, though many lenders prefer higher down payments to reduce their risk exposure.

- Minimum 10% Down Payment Standard: Most conventional lenders require at least 10% down for second home purchases, significantly higher than the 3-5% options available for primary residences. This requirement ensures borrowers have substantial skin in the game and reduces lender risk.

- 20% Down for Optimal Terms: Putting down 20% or more often unlocks better interest rates and eliminates private mortgage insurance requirements. This approach may improve cash flow projections and overall return on investment calculations for your second home property.

- Cash Reserve Requirements: Lenders typically require 2-6 months of mortgage payments in reserves beyond the down payment. These reserves demonstrate your ability to handle multiple property payments during vacancy periods or unexpected expenses.

- Gift Funds and Asset Documentation: Some lenders accept gift funds for portions of the down payment, though documentation requirements are stringent. Alternative assets like stocks or retirement accounts might also qualify as acceptable sources with proper verification procedures.

Qualifying for a Second Home Mortgage Standards

Qualifying for a second home mortgage involves meeting stricter lending standards compared to primary residence loans, as lenders view these properties as higher risk investments. Understanding these qualification criteria helps investors prepare their finances and improve approval odds.

- Credit Score Requirements: Most lenders require minimum credit scores between 640-700 for second home mortgages, with better rates available for scores above 740. Higher credit standards reflect the increased risk lenders associate with non-primary residence properties.

- Debt-to-Income Ratio Limits: Maximum debt-to-income ratios typically cap at 43-45%, though some lenders may accept higher ratios with compensating factors. This calculation includes all existing mortgage payments, investment property debt service, and personal obligations.

- Employment and Income Stability: Lenders prefer borrowers with consistent employment history and stable income sources for at least two years. Self-employed investors or those with variable income may face additional documentation requirements and scrutiny during underwriting.

- Asset and Reserve Verification: Beyond down payment funds, lenders require verification of liquid assets equivalent to several months of property expenses. This requirement ensures borrowers can handle unexpected costs or temporary rental income disruptions.

Investment Property vs Second Home Mortgage Differences

The investment property vs. second home mortgage distinction significantly impacts financing terms, qualification requirements, and tax implications for real estate investors. Understanding these differences helps investors choose the most appropriate classification and financing structure.

- Intended Use Classification: Second homes are properties you plan to occupy personally for part of the year, while investment properties are purchased solely for rental income. This classification affects interest rates, down payment requirements, and available loan programs significantly.

- Interest Rate Variations: Second home mortgages typically offer rates between primary residence and investment property loans. Investment properties generally carry the highest rates due to perceived risk, while second homes fall in the middle range of pricing tiers.

- Tax Treatment Differences: Second homes may qualify for mortgage interest deductions similar to primary residences, while investment properties offer depreciation benefits and expense deductions. Consult tax professionals to understand implications for your specific situation and investment strategy.

- Rental Income Considerations: Investment property loans may allow rental income projections in qualification calculations, while second home mortgages typically don't count potential rental income. This difference affects debt-to-income ratios and overall borrowing capacity for investors.

Current Second Home Mortgage Rates and Market Conditions

Second home mortgage rates in 2026 reflect evolving market conditions that present both opportunities and challenges for real estate investors. Understanding current rate environments and trends helps investors time their acquisitions and financing decisions strategically.

- DSCR Loan Rate Environment: Current DSCR loan rates range between 6.00% and 7.50% for qualified borrowers, representing improved affordability compared to previous years' higher rates. These products might offer attractive alternatives for investors seeking rental income-based qualification methods.

- Conventional Second Home Rates: Traditional second home mortgage rates typically run 0.125% to 0.375% higher than primary residence rates, depending on loan-to-value ratios and borrower qualifications. Rate spreads may vary based on property location and loan amount tiers.

- Market Innovation Trends: Lenders are developing hybrid lending structures and innovative DSCR products that could expand financing opportunities for real estate investors. These developments may introduce more flexibility in underwriting and qualification processes throughout 2026.

- Regional Rate Variations: Mortgage rates might vary by geographic region based on local market conditions and lender competition. Investors should compare rates across multiple markets, especially when considering properties in different states or metropolitan areas.

●Conclusion

Successfully securing a mortgage for a second home requires thorough preparation, understanding of qualification requirements, and strategic financial planning. Real estate investors who master these fundamentals position themselves to capitalize on opportunities in vacation rental markets and long-term appreciation plays.

The evolving lending landscape in 2026 presents new opportunities through innovative DSCR products and potentially more favorable rate environments. Investors should stay informed about market developments while building relationships with lenders who understand investment property financing.

Whether you're expanding an existing portfolio or making your first second home purchase, partnering with experienced mortgage professionals can help navigate the complexities and secure optimal financing terms. Take time to evaluate your financial position, explore multiple lending options, and structure your acquisition strategy to maximize long-term returns on your second home investment.