Finding an affordable home in today's competitive real estate market is challenging for anyone — but veterans and active-duty service members have a powerful tool at their disposal: the VA home loan benefit. With no down payment requirement and competitive interest rates, VA loans are among the most borrower-friendly mortgage products available. But what happens when the home you want needs serious work? Can I get a VA loan for a fixer-upper property? The short answer is: it depends. VA loans come with specific property condition requirements, but there are also specialized renovation options that may help eligible borrowers purchase and repair a distressed home. This guide walks you through everything you need to know.

Understanding How VA Loans Approach Property Condition

Before exploring renovation financing options, it's important to understand why property condition matters so much with VA loans in the first place. Unlike some conventional loan programs, VA-backed mortgages are designed to ensure that veterans are purchasing homes that are safe, structurally sound, and sanitary. These are not arbitrary standards — they exist to protect the borrower from taking on a property that could pose health or safety risks.

The Department of Veterans Affairs requires that every property purchased with a VA loan meet what are known as Minimum Property Requirements (MPRs). These requirements are evaluated during a mandatory VA appraisal conducted by a VA-approved appraiser. The appraiser's job is not just to assess market value — they're also responsible for identifying any conditions that may disqualify the home from VA financing.

Common issues that could trigger MPR concerns include:

- Roof damage or deterioration that could allow water intrusion

- Exposed or faulty electrical wiring

- Evidence of pest infestation, particularly wood-destroying organisms

- Foundation problems or significant structural damage

- Inoperable heating systems

- Lack of adequate plumbing or hot water

- Lead-based paint hazards in homes built before 1978

If any of these issues are present, the VA appraisal will typically note them as required repairs before the loan can close. This means that a heavily distressed fixer-upper may not qualify for a standard VA loan purchase loan unless repairs are completed first — which creates a financial challenge for many buyers.

Can I Get a VA Loan for a Fixer-Upper Property With Standard Financing?

A standard VA purchase loan may work for a fixer-upper — but only if the property's issues are minor. If the needed repairs are cosmetic in nature, such as outdated flooring, worn paint, or aging appliances, the home might still pass the VA appraisal and qualify for standard VA financing. In those cases, the buyer could purchase the home and handle those improvements out of pocket after closing.

However, if the property has more significant deficiencies — the kind that affect habitability or safety — a standard VA loan likely won't work without pre-close repairs. In some situations, sellers may agree to make the required repairs before closing as part of the negotiation process. But when dealing with bank-owned properties, foreclosures, or deeply distressed homes, sellers often aren't willing or able to make those fixes.

This is where many veterans hit a wall. The home is priced attractively because of its condition, but standard VA financing won't cover it as-is. That's exactly why understanding VA rehab loan options is so critical for buyers interested in fixer-uppers.

VA Rehab Loan Options: The VA Renovation Loan Explained

The most directly relevant solution for veterans pursuing a distressed property is the VA renovation loan, sometimes called a VA rehab loan. This product is designed to roll the cost of eligible repairs and improvements into a single VA-backed mortgage. Rather than financing the purchase and renovation separately, the borrower takes out one loan that covers both.

VA renovation loans allow eligible borrowers to:

- Purchase a home that needs repairs and finance those repairs within the same loan

- Refinance an existing home and include renovation costs

- Bring a property up to VA Minimum Property Requirements so it can qualify for VA financing

It's worth noting that not every VA-approved lender offers renovation loans. This is a specialty product, and lenders who do offer it may have their own overlays — meaning additional requirements beyond what the VA itself mandates. Working with a lender experienced in VA renovation financing is important.

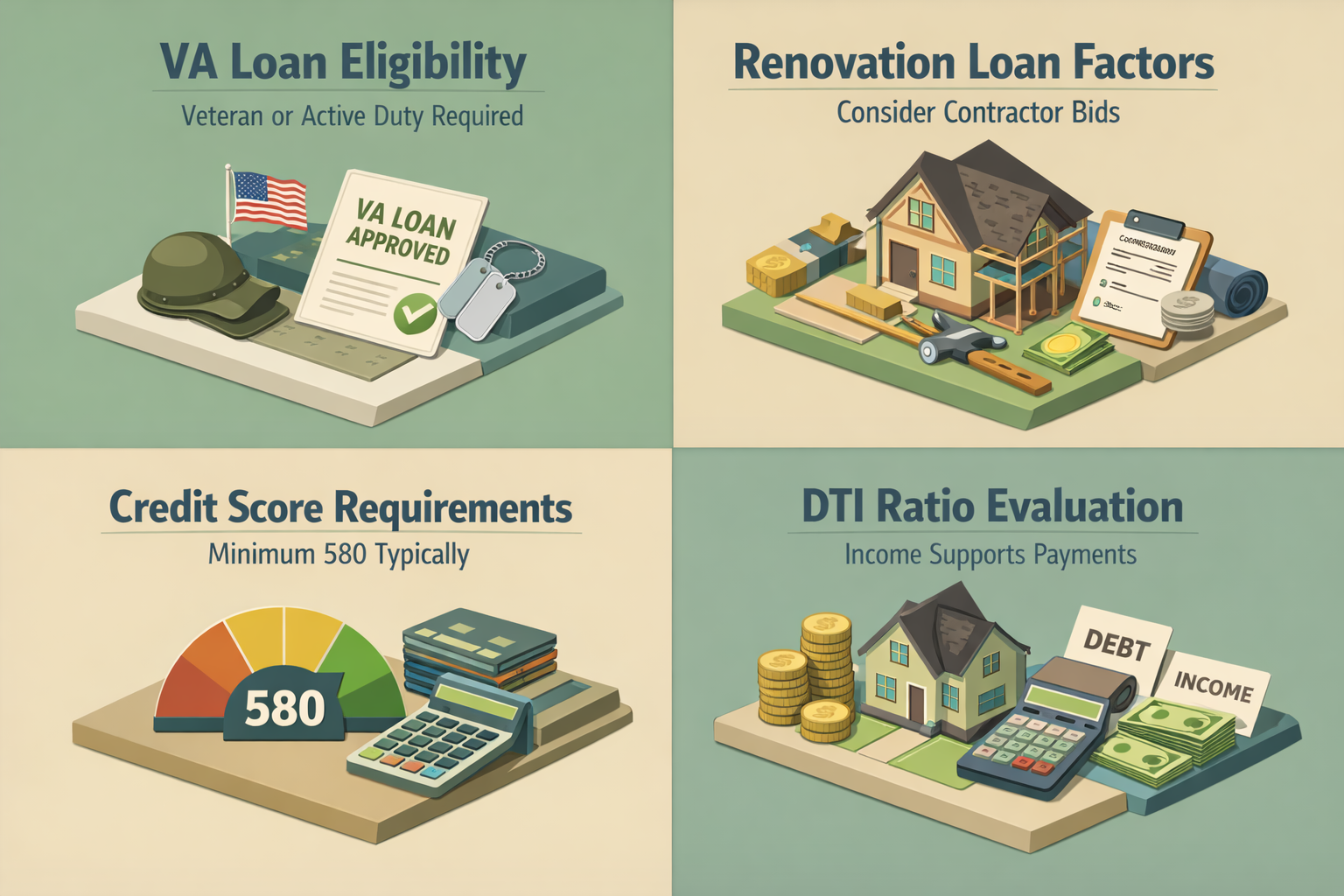

Eligible repairs under VA rehab loan programs typically include items that improve the safety, habitability, or energy efficiency of the home. Examples might include roof replacement, HVAC upgrades, plumbing and electrical repairs, foundation work, and accessibility modifications. Purely luxury upgrades — like adding a pool or high-end landscaping — are generally not covered.

Loan limits for renovation amounts can vary by lender, and the total loan amount must still fall within VA loan limits for the area (though veterans with full entitlement may be exempt from these limits). Working closely with a knowledgeable loan officer helps ensure you're structuring the loan correctly from the start.

How VA Minimum Property Standards Shape Your Purchase Strategy

Understanding minimum property standards for VA loans isn't just about avoiding disqualified homes — it's about planning your purchase strategy more effectively. When you know what the VA appraiser will be looking for, you can evaluate potential fixer-uppers with a clearer eye before making an offer.

Think of it this way: a home with a damaged roof and faulty wiring may be a difficult standard VA loan candidate, but it could be a strong candidate for VA renovation financing — provided you've budgeted appropriately for repairs and found a lender willing to structure the deal.

Here are a few strategic tips for veterans considering fixer-uppers:

- Get a home inspection before ordering the VA appraisal. A general home inspection can flag potential MPR issues early, so you're not surprised during the appraisal process.

- Request repair cost estimates before making an offer. If you're considering renovation financing, having contractor quotes upfront helps you determine if the numbers make sense.

- Work with a real estate agent familiar with VA transactions. Not all agents understand VA property requirements, and an experienced one can help you avoid homes that are unlikely to qualify.

- Ask your lender early about renovation loan availability. Since not all lenders offer this product, confirming availability upfront saves time.

Being proactive about these steps may significantly reduce stress and improve your chances of a smooth transaction — especially when working with VA home loans for distressed properties.

Other Financing Paths Worth Exploring for Distressed Homes

While VA renovation loans are the most targeted solution, veterans aren't limited to that single option. Depending on your situation, there may be other financing approaches worth considering alongside or instead of a VA rehab product.

FHA 203(k) Loans

The FHA 203(k) loan is a government-backed renovation mortgage that allows borrowers to purchase and renovate a property in one loan — similar in concept to the VA renovation loan. Veterans who don't wish to use their VA entitlement, or who are purchasing a property that doesn't meet VA eligibility criteria, might consider this as an alternative. Keep in mind that FHA loans require mortgage insurance premiums, which VA loans do not.

Conventional Renovation Loans

Fannie Mae's HomeStyle Renovation loan and Freddie Mac's CHOICERenovation loan are conventional products that offer similar purchase-plus-renovation financing. These may carry stricter credit requirements and typically require a down payment, but they offer flexibility in terms of the types of improvements covered.

Using a VA Cash-Out Refinance After Purchase

Some veterans choose to purchase a fixer-upper through alternative financing, make repairs, and then refinance into a VA loan once the home meets MPRs. A VA cash-out refinance could allow borrowers to tap into equity built through renovation work — though this approach requires short-term financing for the initial purchase and repairs.

Each path comes with trade-offs, and the best option depends on your entitlement status, credit profile, timeline, and renovation scope. A trusted lending advisor can help you model out the scenarios most relevant to your situation.

VA Loan Eligibility Basics and Renovation Loan Qualification Factors

Before diving into renovation financing specifically, it's useful to revisit VA loan eligibility at a high level. To use a VA-backed loan, you generally must be an eligible veteran, active-duty service member, National Guard or Reserve member who meets service requirements, or a surviving spouse of a veteran who died in service or from a service-connected disability. You'll need a Certificate of Eligibility (COE) to confirm your entitlement with your lender.

From a credit and income standpoint, VA loans don't have a strict minimum credit score set by the VA itself — but individual lenders typically require a score of at least 580 to 620, with some requiring higher scores for renovation products. Debt-to-income (DTI) ratios are also evaluated, and lenders will want to confirm that your income can support both the purchase and renovation loan payments.

For renovation loans specifically, additional qualification factors may include:

- Detailed contractor bids or renovation plans submitted at underwriting

- Use of licensed, insured contractors approved by the lender

- A renovation contingency reserve (often 10–20% of renovation costs) built into the loan

- A draw schedule for releasing renovation funds as work is completed

These added layers of documentation and process exist because renovation loans are more complex than standard purchase loans. Having your paperwork organized and working with contractors who understand construction lending timelines can make a meaningful difference in how smoothly your loan closes.

●Conclusion

So, can I get a VA loan for a fixer-upper property? The answer is a qualified yes — with the right approach and the right loan product. Standard VA purchase loans require homes to meet Minimum Property Requirements, which means heavily distressed properties often won't qualify as-is. But VA renovation loans provide a meaningful pathway for eligible veterans to purchase and repair a home through a single, streamlined financing solution. Understanding the distinctions between standard VA financing, VA rehab loan options, and alternative renovation products empowers you to make smarter decisions as a homebuyer. At LoanWise, we're here to help veterans and service members navigate these options with confidence. If you're exploring a fixer-upper purchase, connect with one of our experienced loan advisors today to find the financing path that fits your goals.