Business Loan for Working Capital: Fueling Real Estate Investment Success

Real estate investors often find themselves in situations where property deals require immediate action, but cash flow might be temporarily tight. A business loan for working capital can bridge this gap, providing the flexible financing needed to maintain operations while building your investment portfolio.

Working capital loans serve a different purpose than traditional mortgage financing. While DSCR loans and fix and flip financing target specific properties, working capital funding addresses the day-to-day operational needs that keep your investment business running smoothly. This type of financing can help cover expenses like property maintenance, marketing costs, contractor payments, and other business expenses that arise between acquisitions.

Essential Steps to Evaluate Your Working Capital Needs

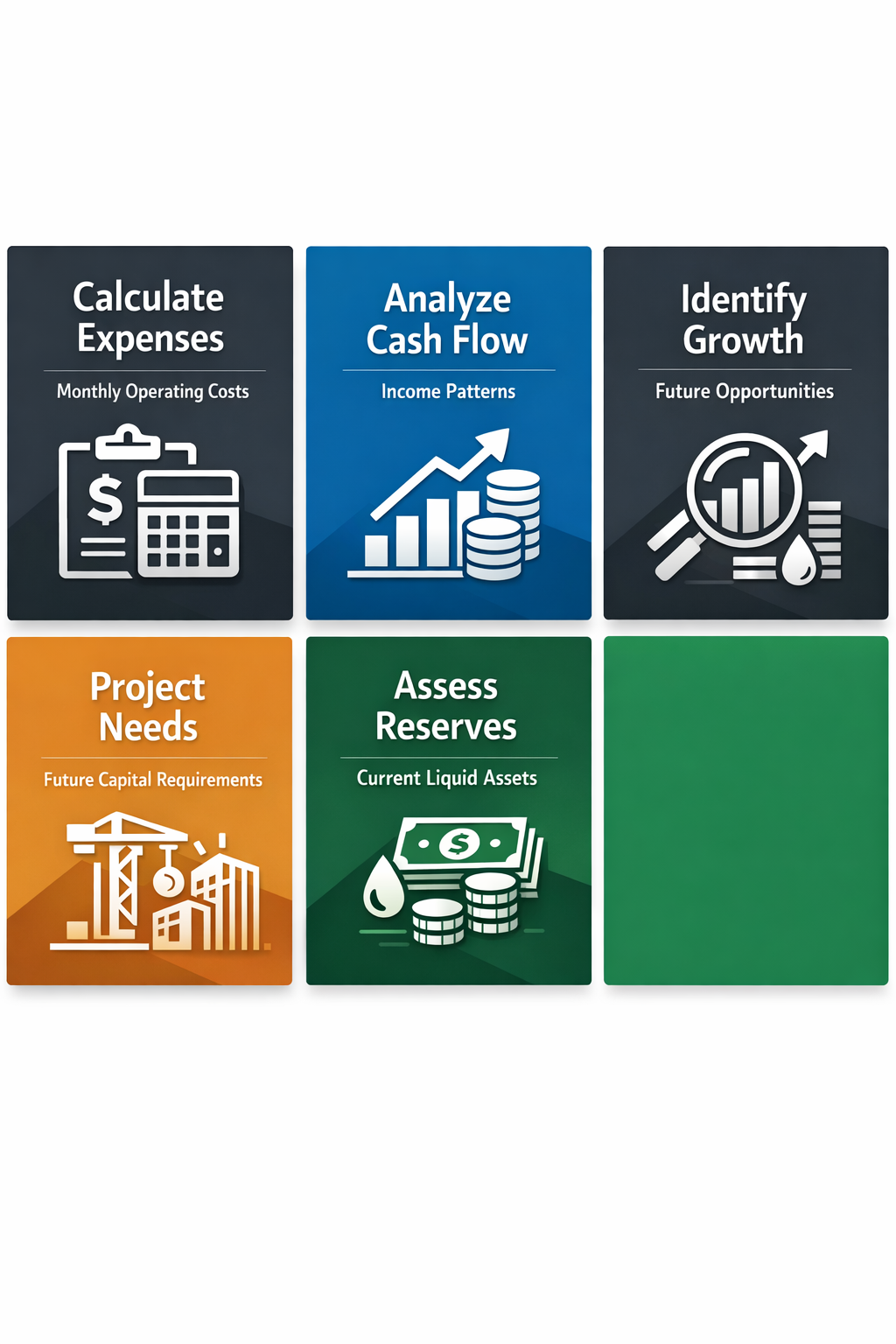

Evaluating your working capital needs requires a systematic approach to understand your business's financial requirements. Real estate investors must carefully assess their cash flow patterns and operational expenses before pursuing financing.

- Calculate your monthly operating expenses: Include property management costs, insurance premiums, utility payments, and marketing expenses. This baseline helps determine the minimum working capital needed to maintain operations.

- Analyze your cash flow cycles: Real estate investments often involve irregular income patterns. Review your rental income timing, property sale proceeds, and seasonal variations that might affect cash availability.

- Identify growth opportunities: Consider upcoming property acquisitions, renovation projects, or expansion plans that may require additional capital beyond regular operations.

- Assess your current liquid reserves: Evaluate existing cash reserves and determine how much additional working capital would provide comfortable breathing room for your business operations.

- Project future needs: Estimate working capital requirements for the next 12-24 months, factoring in business growth and market conditions that might impact your investment activities.

Understanding Working Capital Loan Requirements and Qualification Criteria

Working capital loan requirements can vary significantly among lenders, but understanding common qualification criteria helps investors prepare stronger applications. Most financial institutions evaluate several key factors when considering working capital financing.

- Review credit score requirements: Most lenders typically require personal credit scores of 650 or higher for working capital loans, though some may consider lower scores with additional collateral or guarantees.

- Prepare financial documentation: Gather recent tax returns, bank statements, profit and loss statements, and cash flow projections. Lenders want to see consistent business income and responsible financial management.

- Document business experience: Demonstrate your track record in real estate investing, including successful property transactions, rental income history, and overall business management experience.

- Calculate debt-to-income ratios: Ensure your existing debt obligations don't exceed acceptable levels. Lenders typically prefer debt-to-income ratios below certain thresholds, though requirements may vary.

- Establish business banking relationships: Maintain organized business banking records and consider working with institutions familiar with real estate investment businesses and their unique cash flow patterns.

Strategic Application Process for Working Capital Financing

The strategic application process for working capital financing requires careful preparation and timing. Real estate investors can improve their approval chances by following a structured approach to their loan applications.

- Research appropriate lenders: Identify financial institutions that specialize in business lending and understand real estate investment operations. Some lenders may be more familiar with the unique needs of property investors.

- Prepare comprehensive application materials: Compile all required documentation including business plans, financial statements, and supporting materials that demonstrate your investment strategy and repayment capability.

- Present a clear use of funds: Articulate specifically how the working capital will be used to support business operations and potentially generate returns that ensure loan repayment.

- Consider timing strategically: Apply for working capital loans when your financial position is strongest and when you can demonstrate stable cash flow from your investment activities.

- Negotiate terms that align with cash flow: Work with lenders to structure repayment terms that match your business's cash flow patterns and seasonal variations in income.

Smart Ways to Use Working Capital Loans in Real Estate Investing

Smart use of working capital loans can significantly enhance your real estate investment operations and create opportunities for business growth. Understanding how to deploy these funds effectively maximizes their impact on your investment success.

- Bridge financing gaps between deals: Use working capital to cover expenses while waiting for property sales to close or rental income to stabilize, maintaining business continuity during transition periods.

- Fund property improvements and maintenance: Address urgent repairs, cosmetic improvements, or preventive maintenance that helps preserve property values and maintain rental income streams.

- Support marketing and business development: Invest in marketing efforts to find better deals, attract quality tenants, or expand your network of contractors and service providers.

- Manage seasonal cash flow variations: Cover expenses during periods when rental income might be lower or when property-related costs typically increase, such as winter heating expenses or spring maintenance.

- Take advantage of time-sensitive opportunities: Having working capital available allows you to move quickly on attractive investment opportunities that require immediate action or deposits.

Securing Funds for Daily Operations Through Business Credit Lines

Securing funds for daily operations often works better through business lines of credit rather than traditional term loans. A business line of credit for cash flow provides more flexibility for real estate investors who need ongoing access to capital.

- Access funds as needed: Business credit lines allow you to draw funds only when necessary, potentially reducing interest costs compared to taking a lump sum loan that sits unused in your account.

- Revolving credit structure: As you repay borrowed amounts, that credit becomes available again, creating a renewable source of working capital for ongoing business needs.

- Lower initial costs: Many business lines of credit have lower upfront fees compared to term loans, making them more cost-effective for short-term working capital needs.

- Flexible repayment options: Credit lines often offer more flexible repayment terms, allowing you to make interest-only payments during low cash flow periods and larger payments when income is stronger.

- Emergency fund capability: Having an established credit line provides peace of mind and quick access to funds during unexpected situations or urgent property-related expenses.

●Conclusion

Working capital financing represents a valuable tool for real estate investors who need operational flexibility and cash flow support. Whether through traditional business loans or lines of credit, these funding options can help bridge gaps between property transactions, fund necessary improvements, and support business growth initiatives.

Success with working capital loans depends on careful planning, understanding your true financial needs, and working with lenders who understand the real estate investment business. By following the evaluation steps, meeting qualification requirements, and using funds strategically, investors can leverage working capital financing to build stronger, more resilient investment operations.

At Trulo Mortgage, we understand that real estate investors need more than just property financing. While we specialize in DSCR loans, fix and flip financing, and rental property loans, we recognize that working capital needs are an important part of your overall investment strategy. Consider how different financing tools can work together to support your long-term success in real estate investing.