When your business needs funding, two of the most common options you'll likely come across are a business line of credit and a term loan. Both can give your company access to capital, but they work quite differently — and choosing the wrong one could cost you more than you'd expect. Whether you're a small business owner looking to manage cash flow, an entrepreneur preparing to expand, or a commercial borrower exploring your options, understanding how each product works is the first step toward making a smart financing decision. This guide walks you through the key differences, benefits, and ideal use cases for each so you can move forward with confidence.

Understanding How a Business Line of Credit Works

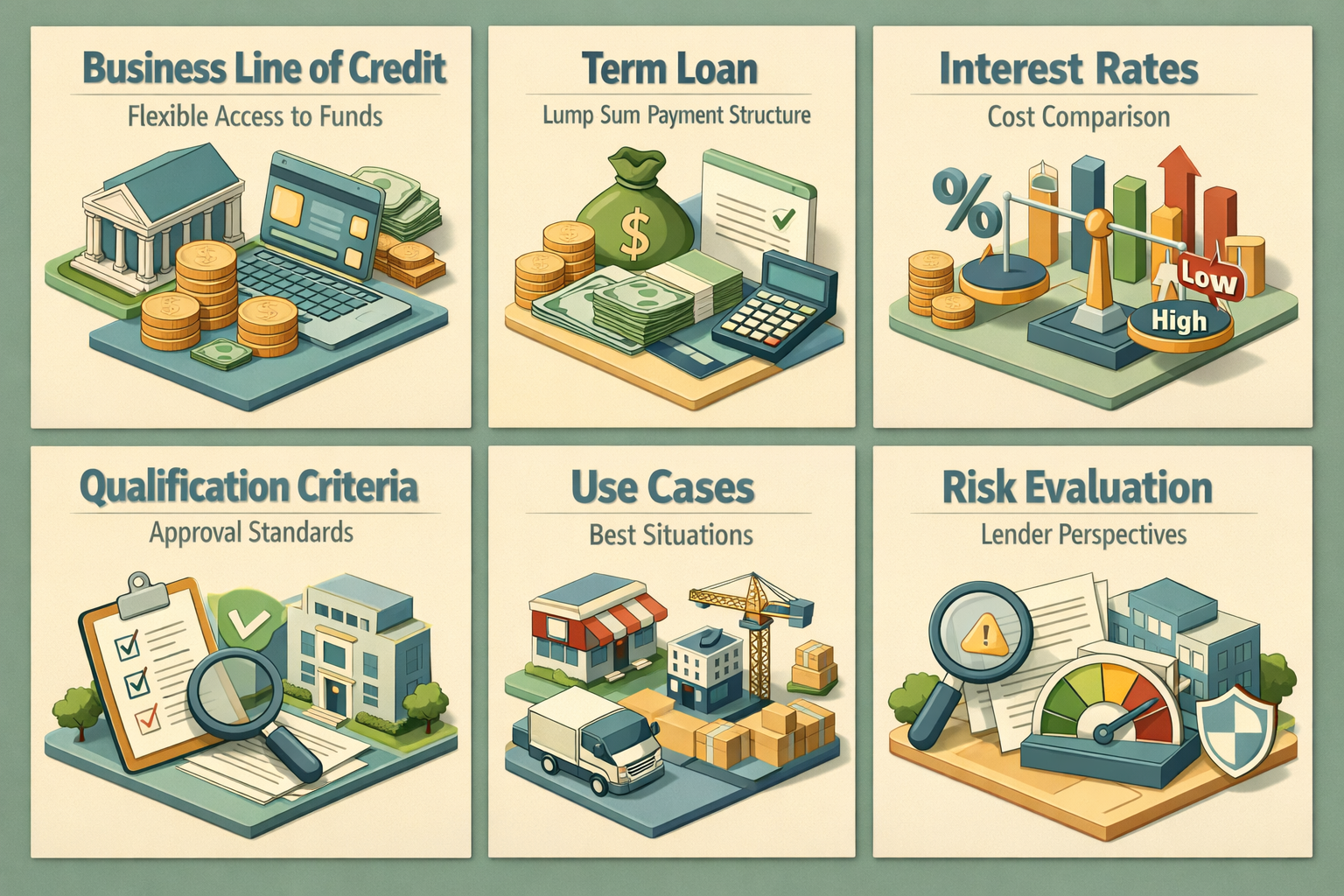

A business line of credit is a flexible borrowing arrangement that gives your company access to a set pool of funds. You can draw from that pool whenever you need money, repay it, and borrow again — much like a credit card. You're only charged interest on what you actually use, not the full credit limit.

This revolving structure makes a line of credit particularly useful for managing day-to-day operational needs. If your business experiences seasonal slowdowns, unexpected expenses, or gaps between invoices and payments, a line of credit can act as a financial safety net. It's not meant to fund a single large purchase — it's designed to keep your cash flow healthy over time.

Lines of credit can be either secured or unsecured. Secured options may require collateral such as business assets or accounts receivable, while unsecured lines typically depend more heavily on your creditworthiness. Lenders will generally look at your business credit score, revenue history, and time in operation when evaluating your application.

What Sets a Term Loan Apart from Revolving Credit

A term loan provides a lump sum of money upfront that you repay over a fixed period — typically with regular monthly payments that include both principal and interest. Unlike a line of credit, once you've used the funds, you can't re-borrow from the same loan. The repayment schedule is set from the beginning, giving you a predictable financial commitment each month.

Term loans are well suited for one-time investments where you know exactly how much you need. Think equipment purchases, commercial real estate acquisitions, business expansions, or large-scale renovations. Because the loan amount and purpose are clearly defined, lenders may offer more competitive interest rates on term loans compared to revolving credit products — especially for borrowers with strong financials.

Term loans can be short-term (a few months to a couple of years) or long-term (up to ten years or more, depending on the lender and purpose). Short-term loans often come with higher rates but faster access to funds, while long-term loans typically offer lower monthly payments spread across a longer horizon.

Comparing Interest Rates and Overall Cost of Borrowing

Cost is one of the most important factors when choosing between these two financing tools. With a business line of credit, interest accrues only on the amount you've drawn. This can make it more cost-effective for businesses that don't need to use the full credit limit all at once. However, lines of credit may carry variable interest rates, which means your borrowing costs could rise if market rates increase.

Term loans, on the other hand, often come with fixed interest rates, offering more predictability in your monthly budget. If you're locking in a loan during a period of relatively favorable rates, a fixed-rate term loan could save you money over the life of the loan. That said, some term loans do carry variable rates — so it's worth confirming the rate structure before you sign.

Additional fees can also affect the total cost. Lines of credit may include annual maintenance fees, draw fees, or inactivity fees. Term loans may come with origination fees, prepayment penalties, or processing charges. Always review the full fee schedule before committing to any financing product, and consider using a loan cost calculator to compare total repayment amounts.

Credit and Qualification Requirements for Each Option

Qualifying for either product requires demonstrating that your business is a reliable borrower. Lenders typically evaluate a mix of personal and business credit scores, annual revenue, time in business, and existing debt obligations. However, the threshold for approval may differ between the two products.

Term loans — particularly those backed by the Small Business Administration (SBA) or offered through traditional banks — often have stricter qualification standards. Lenders may require at least two years of business history, a minimum annual revenue figure, and a solid credit profile. The larger the loan amount, the more documentation you'll likely need to provide, including tax returns, financial statements, and a business plan.

Lines of credit can sometimes be easier to access, especially for businesses with shorter operating histories, because the lower borrowing amounts carry less risk for the lender. Online lenders and fintech platforms may offer lines of credit with more flexible requirements — though this often comes at the cost of higher interest rates or lower credit limits. Entrepreneurs just starting out might find that building business line of credit options down the road by improving their credit over time opens up better opportunities.

Best Use Cases: Matching the Product to Your Business Need

The right financing tool depends largely on what you're trying to accomplish. Here's a practical breakdown of when each option tends to make the most sense:

- Choose a business line of credit if you need ongoing access to working capital, manage fluctuating cash flow, want flexibility to borrow only what you need, or are covering short-term expenses like payroll, inventory, or vendor payments.

- Choose a term loan if you're funding a specific one-time investment, need a large lump sum, want a predictable repayment schedule, or are purchasing equipment, real estate, or making a significant business improvement.

Some business owners find that using both products simultaneously works well. For example, you might take out a term loan to finance new commercial equipment while maintaining a line of credit as a cash flow buffer. This combined approach gives your business both stability and flexibility — as long as you manage both responsibly.

Commercial real estate investors may also find term loans particularly useful when financing property acquisitions, while a line of credit could help bridge gaps between closing costs, rent collections, or renovation phases.

How Lenders Evaluate Risk Differently for Each Product

It's worth understanding that lenders don't view a line of credit and a term loan the same way from a risk standpoint. With a term loan, the lender knows exactly how much you're borrowing and how long they're extending credit. The fixed repayment structure makes it easier for them to model risk and price the loan accordingly.

A revolving line of credit, however, presents ongoing risk because you could potentially draw the full amount at any time. This is one reason why lenders may periodically review your financial health and could adjust or reduce your credit limit if your business performance declines. It's not uncommon for lenders to conduct annual reviews on existing lines of credit.

For small business owners and entrepreneurs, this distinction matters. If your business is growing and your financials are improving, your line of credit limit might increase over time. On the other hand, if revenues dip or your credit score takes a hit, your access to revolving funds could shrink. Keeping your finances organized and maintaining strong creditworthiness is essential for preserving access to both types of funding.

●Conclusion

Choosing between a business line of credit and a term loan doesn't have to be overwhelming. Both serve important roles in a well-rounded business financing strategy — it just comes down to what your business needs right now and where you're headed. If flexibility and ongoing access to capital matter most, a line of credit may be the stronger fit. If you're making a defined, one-time investment, a term loan could offer better rates and a clearer repayment path. The key is to evaluate your current cash flow, your short-term goals, and your long-term growth plans before committing. At LoanWise, we're here to help small business owners and entrepreneurs find the right financing solutions for every stage of the journey. Ready to explore your options? Connect with a lending specialist today and take the next step toward smarter borrowing.