Business Line of Credit Explained: A Flexible Financing Tool for Real Estate Investors

Real estate investors often face unique cash flow challenges that traditional mortgage products can't address. While DSCR loans and fix and flip financing serve specific property acquisition needs, a business line of credit explained in simple terms represents a flexible financing solution that could complement your investment strategy. This revolving credit facility might provide the working capital flexibility needed to seize time-sensitive opportunities, manage renovation costs, or bridge gaps between property transactions.

Unlike term loans that provide a lump sum upfront, a business line of credit functions more like a corporate credit card with typically higher limits and potentially lower interest rates. For real estate investors managing multiple properties or renovation projects, this financing tool could offer the agility needed to respond quickly to market opportunities while maintaining cash flow stability.

What Is a Business Line of Credit

Q: How does a business line of credit work for real estate investors?

A business line of credit typically functions as a revolving credit facility that allows investors to draw funds as needed, up to a predetermined limit. Unlike traditional loans where you receive the full amount upfront, you may only pay interest on the funds you actually use. This could make it particularly valuable for real estate investors who need flexible access to capital for opportunities like property improvements, holding costs, or quick property acquisitions that don't qualify for conventional financing.

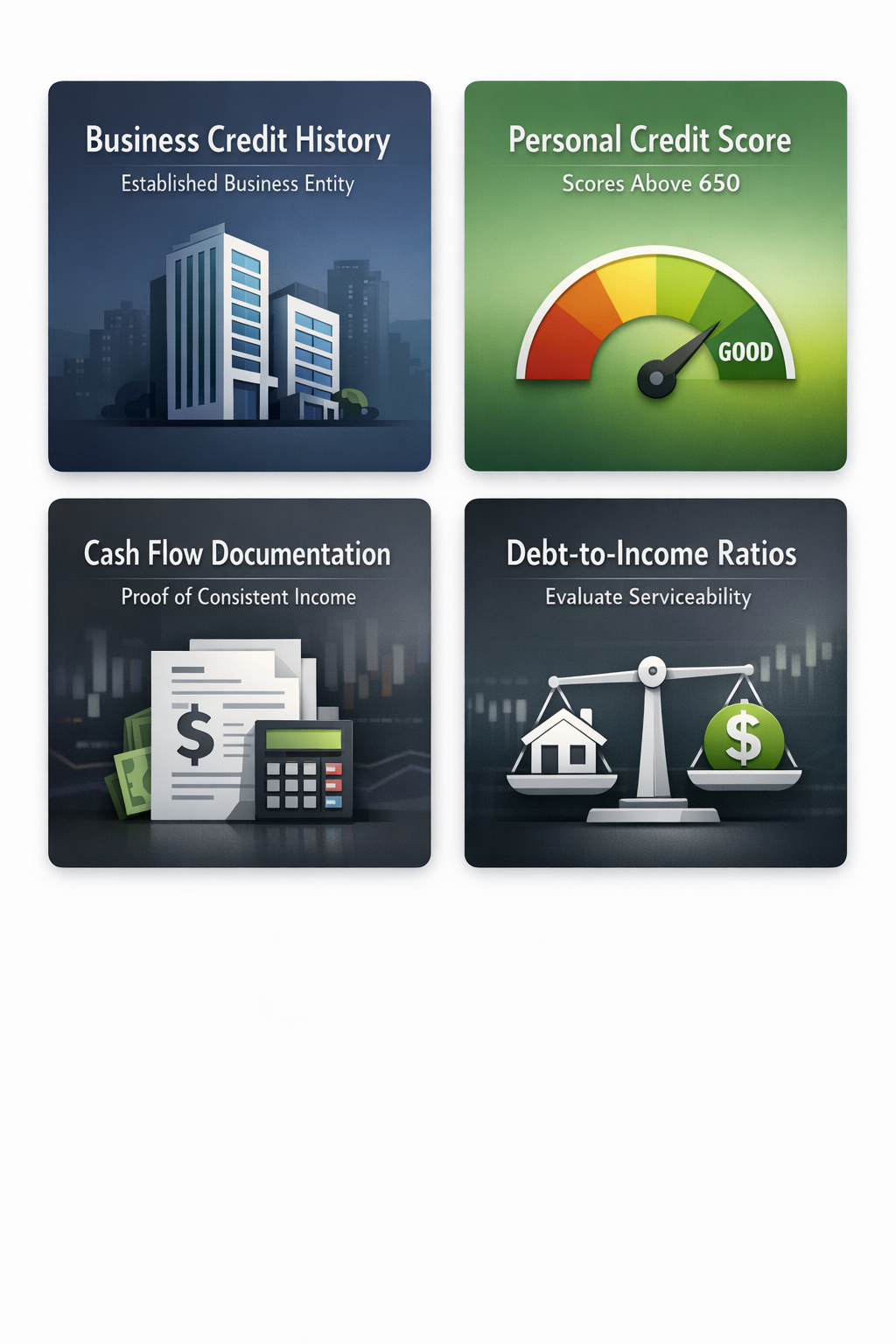

Key Requirements for Business Line of Credit

Business line of credit requirements might vary among lenders, but real estate investors typically need to meet several core criteria to qualify for this financing option.

- Business Credit History: Most lenders may require an established business entity with a track record of revenue generation and responsible credit management

- Personal Credit Score: Individual credit scores often play a significant role, with many lenders preferring scores above 650 for competitive rates

- Cash Flow Documentation: Proof of consistent income from rental properties or investment activities could be essential for approval

- Debt-to-Income Ratios: Lenders typically evaluate your ability to service additional debt alongside existing mortgage obligations and property expenses

Interest Rates and Cost Structure

Understanding business line of credit interest rates helps investors evaluate whether this financing option aligns with their investment returns and cash flow projections.

- Variable Rate Structure: Most business lines of credit feature variable interest rates that may fluctuate with market conditions, typically tied to prime rate or similar benchmarks

- Draw Period Costs: During the draw period, you might only pay interest on outstanding balances, potentially making this more cost-effective than term loans for sporadic funding needs

- Additional Fees: Some lenders may charge annual fees, maintenance fees, or draw fees that could impact the total cost of the facility

- Secured vs. Unsecured Rates: Lines of credit secured by real estate or business assets often carry lower interest rates than unsecured options

Using Business Credit Lines for Working Capital

Using a business line of credit for working capital could provide real estate investors with strategic advantages in managing their investment portfolio and cash flow timing.

- Bridge Funding Gaps: Cover holding costs, property taxes, or maintenance expenses while waiting for rental income or property sales to materialize

- Renovation Project Management: Fund property improvements and renovations on a draw-as-needed basis, potentially improving cash flow management during extended projects

- Opportunity Financing: Quickly access capital for time-sensitive investment opportunities that may not wait for traditional loan processing timelines

- Portfolio Expansion Support: Supplement down payments or closing costs when traditional financing alone might not provide sufficient liquidity for new acquisitions

Strategic Applications in Real Estate Investing

Real estate investors might find business lines of credit particularly valuable in specific investment scenarios where flexibility and speed matter more than long-term, low-cost financing.

- Fix and Flip Support: Supplement traditional fix and flip loans by providing additional renovation capital or covering unexpected project costs that exceed initial estimates

- Rental Property Management: Handle vacancy periods, emergency repairs, or seasonal maintenance costs without disrupting other investment activities or depleting cash reserves

- Market Timing Advantages: Respond quickly to below-market property opportunities or distressed sales that require fast closing timelines

- Cash Flow Optimization: Smooth out irregular rental income or manage the timing differences between property sales and new acquisitions

Comparison with Traditional Real Estate Financing

While DSCR loans, fix and flip financing, and bridge loans serve specific property-related needs, business lines of credit offer different advantages that could complement these traditional real estate financing options.

- Flexibility vs. Structure: Lines of credit provide more flexible access to funds compared to the structured disbursement schedules of renovation loans or the property-specific nature of DSCR loans

- Speed of Access: Once established, drawing from a line of credit might be faster than applying for new loans for each investment opportunity or unexpected expense

- Cost Efficiency for Short-Term Needs: For temporary funding needs, paying interest only on amounts used could be more cost-effective than the closing costs and fees associated with new mortgage originations

- Portfolio-Level Financing: Unlike property-specific loans, a business line of credit could support multiple properties or investment activities under a single facility

●Conclusion

A business line of credit explained in the context of real estate investing represents a flexible financing tool that could complement traditional mortgage products like DSCR loans and fix and flip financing. While it may not replace property-specific financing for major acquisitions, it might provide the working capital flexibility needed to optimize your investment strategy and respond to market opportunities.

The key to successfully using a business line of credit lies in understanding how it fits within your broader financing strategy. Consider factors like interest rate environments, your typical holding periods, and cash flow patterns when evaluating whether this financing option aligns with your investment goals. For real estate investors seeking greater financial agility in their operations, exploring business line of credit options might provide the flexibility needed to enhance investment performance and capitalize on time-sensitive opportunities.