Business Debt Consolidation Strategies

Real estate investors often juggle multiple financing sources across their portfolios, from fix and flip loans to rental property mortgages. When managing several high-interest debts becomes overwhelming, a business loan for debt consolidation might offer a strategic solution. This financing approach could help streamline your payment structure while potentially reducing overall interest costs.

Consolidating business debt involves combining multiple existing debts into a single loan, typically with more favorable terms. For real estate investors, this strategy may provide improved cash flow management and simplified bookkeeping across your investment properties.

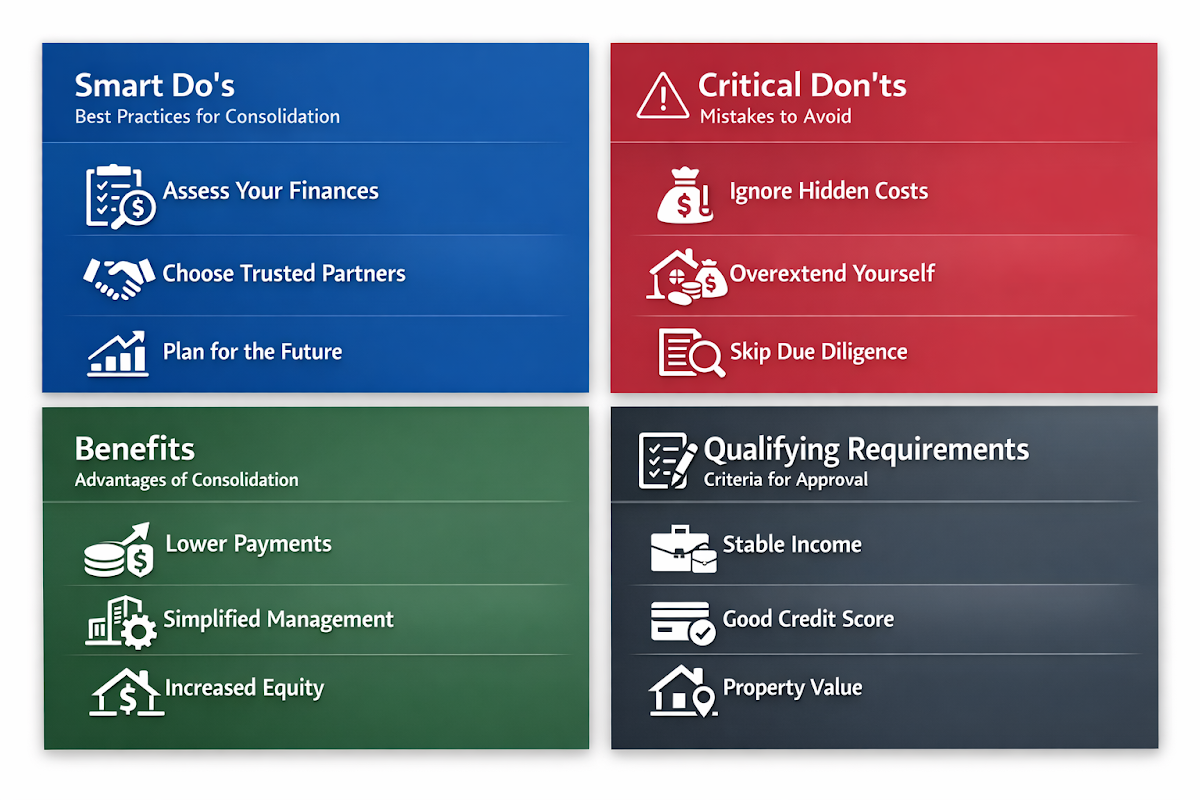

Smart Do's for Business Debt Consolidation

Smart do's for business debt consolidation can help real estate investors maximize the benefits of this financing strategy. Following these best practices may improve your chances of securing favorable terms and achieving better financial management.

- Calculate total debt and monthly obligations: Before pursuing consolidation, compile a comprehensive list of all business debts, including credit cards, equipment loans, and short-term financing used for property investments.

- Research multiple lenders and loan products: Different financial institutions may offer varying terms for debt consolidation loans, so comparing options could help you find the most suitable arrangement for your investment business.

- Focus on improving your debt-to-income ratio: Consolidation works best when it genuinely reduces your monthly payment burden and frees up cash flow for new investment opportunities.

- Consider timing with your investment cycle: Plan consolidation around your property acquisition and renovation schedule to ensure the new loan structure supports your business operations.

Critical Don'ts That Could Hurt Your Investment Business

Critical don'ts that could hurt your investment business include common mistakes that real estate investors might make when pursuing debt consolidation. Avoiding these pitfalls may help protect your financial stability and investment capacity.

- Don't consolidate without addressing spending habits: If poor financial management caused the debt accumulation, consolidation alone won't solve underlying business practices that led to multiple high-interest obligations.

- Don't ignore the total cost over time: A longer repayment term might reduce monthly payments but could increase the total interest paid, potentially affecting your long-term investment returns.

- Don't rush into the first offer: Taking the initial consolidation loan proposal without shopping around may result in less favorable terms than what other lenders might provide.

- Don't overlook prepayment penalties: Some existing loans may have early payoff fees that could offset the benefits of consolidation, making it important to calculate the true cost of this strategy.

Types of Debt Consolidation Loans for Real Estate Investors

Types of debt consolidation loans for real estate investors vary based on collateral requirements and intended use. Understanding these options may help you select the most appropriate financing structure for your investment business needs.

- Secured business term loans: These loans typically use business assets or real estate as collateral, which may result in lower interest rates compared to unsecured options. The collateral requirement could make qualification easier for investors with substantial property portfolios.

- Business lines of credit: A revolving credit facility might provide flexibility for managing varying debt levels throughout your investment cycle. This option could work well for investors who experience seasonal cash flow fluctuations.

- SBA debt refinancing programs: Certain Small Business Administration programs may allow debt consolidation under specific circumstances, potentially offering favorable terms for qualifying real estate investment businesses.

- Commercial real estate refinancing: If you own investment properties with significant equity, refinancing existing mortgages while pulling out additional funds could serve as an indirect consolidation method.

Benefits of Debt Consolidation for Business Cash Flow

Benefits of debt consolidation for business cash flow extend beyond simple payment reduction. Real estate investors may find that streamlined debt management supports their overall investment strategy and operational efficiency.

- Simplified payment management: Instead of tracking multiple due dates and payment amounts, consolidation creates a single monthly obligation that may reduce administrative burden and the risk of missed payments.

- Potential interest rate reduction: If your credit profile has improved since taking on the original debts, consolidation might qualify you for lower rates, reducing the overall cost of capital for your investment business.

- Improved cash flow predictability: Fixed payment amounts make it easier to forecast monthly expenses and plan for future property acquisitions or renovations within your investment portfolio.

- Enhanced credit utilization: Paying off multiple credit cards and lines of credit through consolidation could improve your credit utilization ratio, potentially boosting your business credit scores for future financing needs.

Qualifying Requirements and Application Process Steps

Qualifying requirements and application process steps for business debt consolidation loans typically involve demonstrating your investment business's financial stability and repayment capacity. Understanding these criteria may help you prepare a stronger application.

- Financial documentation preparation: Lenders commonly require tax returns, profit and loss statements, and cash flow projections that demonstrate your real estate investment business generates sufficient income to support the consolidated loan payments.

- Credit score and history evaluation: Both personal and business credit scores may factor into approval decisions, with higher scores potentially qualifying for better interest rates and terms.

- Debt-to-income analysis: Lenders typically calculate your total monthly debt obligations against business income to ensure the consolidated payment improves rather than worsens your financial position.

- Collateral assessment if applicable: For secured consolidation loans, property appraisals or asset valuations may be required to determine the loan amount and terms you could qualify for.

●Conclusion

A business loan for debt consolidation could provide real estate investors with a pathway to streamlined financial management and improved cash flow. However, success depends on carefully evaluating your current debt structure, shopping for favorable terms, and ensuring the consolidated loan supports your investment goals.

Before pursuing consolidation, consider how it fits into your broader investment strategy and whether the potential benefits justify any costs involved. The right consolidation approach might free up capital for new opportunities while simplifying your business operations.

At Trulo Mortgage, we understand that real estate investors need flexible financing solutions that support their unique business models. Whether you're considering debt consolidation or exploring other investment financing options, our team can help you evaluate strategies that align with your portfolio goals.