Business Credit Score Requirements Transform DSCR Loan Access for Investors

Your business credit score might determine whether you secure that next rental property investment or miss out entirely. As DSCR loans continue evolving with stricter credit standards in 2026, real estate investors need to understand how their business credit profile affects financing opportunities. With interest rates ranging from 6.00% to 7.50%, getting approved for these income-focused loans requires more than just strong rental cash flow.

Unlike traditional mortgages that rely heavily on personal income, DSCR loans evaluate your property's rental income potential. However, lenders still scrutinize your business credit report to assess risk and determine loan terms. This shift toward more rigorous underwriting means investors can't ignore their business credit health when planning portfolio expansion strategies.

Understanding Business Credit Score Impact on DSCR Lending

Understanding business credit score impact on DSCR lending reveals why many investors struggle with loan approvals despite strong rental income. DSCR lenders typically examine both personal and business credit profiles to evaluate overall borrower risk, especially as the lending landscape becomes more competitive in 2026.

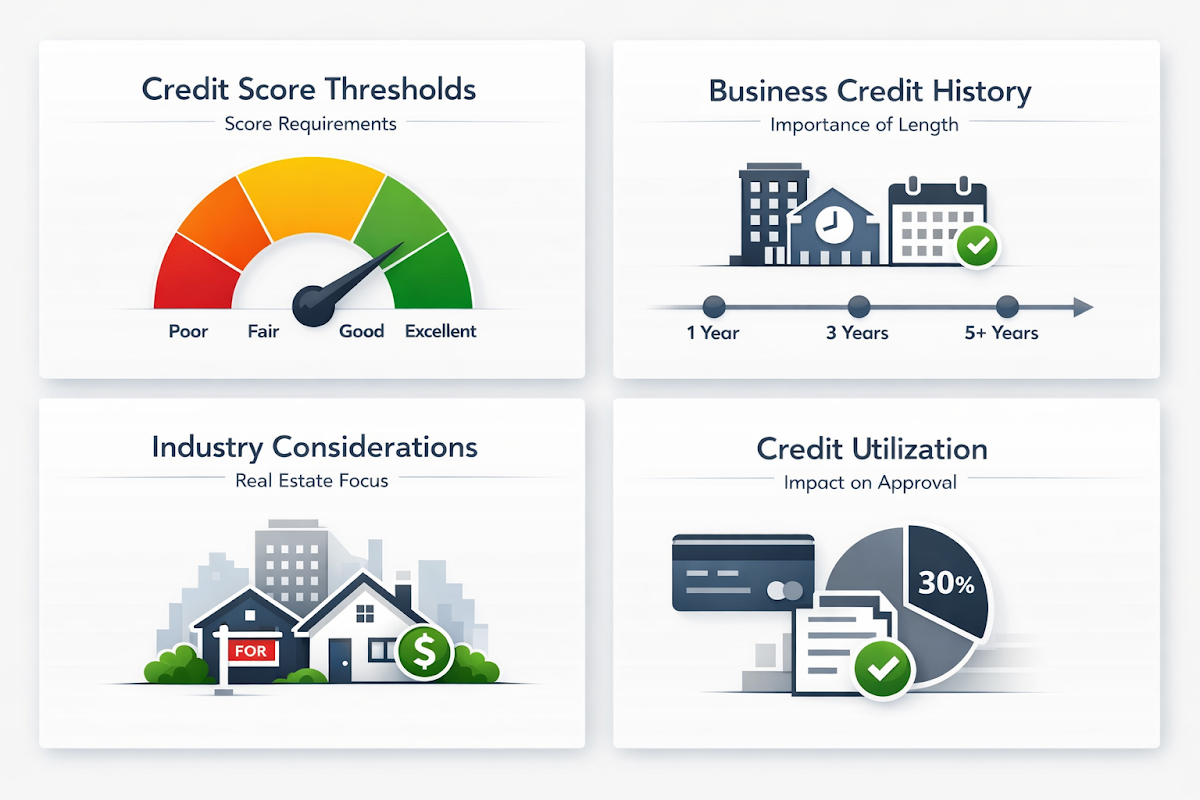

- Credit score thresholds vary significantly: Most DSCR lenders require business credit scores above 650, though some may accept lower scores with compensating factors like larger down payments or stronger cash reserves.

- Business credit history length matters: Lenders often prefer established business credit profiles spanning at least two years, as this demonstrates consistent financial management and payment history.

- Industry-specific considerations apply: Real estate investment businesses may receive different treatment than traditional businesses, with lenders evaluating property management experience and rental income stability.

- Credit utilization ratios affect approval odds: Business credit utilization below 30% typically strengthens loan applications, while higher utilization might trigger additional scrutiny or higher interest rates.

Checking Business Credit Score Before DSCR Applications

Checking business credit score before DSCR applications helps investors identify potential issues that could delay or derail financing. Many successful investors make credit monitoring a regular part of their investment preparation process, especially when planning multiple property acquisitions.

- Multiple reporting agencies provide different insights: Business credit scores from different agencies might vary significantly, so checking reports from major bureaus helps create a complete picture of your credit standing.

- Recent inquiry patterns influence lending decisions: Excessive credit inquiries within short timeframes could signal financial distress to DSCR lenders, potentially affecting loan terms or approval likelihood.

- Accuracy verification prevents application delays: Incorrect information on business credit reports might cause unnecessary loan processing delays, making pre-application review essential for smooth transactions.

- Timing considerations optimize approval chances: Checking business credit scores 60-90 days before applying allows time for addressing issues without rushing into time-sensitive property purchases.

Key Business Credit Report Elements DSCR Lenders Review

Key business credit report elements DSCR lenders review extend beyond simple credit scores to encompass comprehensive financial behavior patterns. Understanding these evaluation criteria helps investors position their applications more strategically in an increasingly selective lending environment.

- Payment history carries significant weight: Consistent on-time payments to suppliers, contractors, and other business creditors demonstrate reliability that DSCR lenders value highly when assessing loan risk.

- Credit mix diversity shows financial sophistication: A balanced portfolio of business credit accounts, including credit cards, equipment financing, and trade lines, might indicate experienced financial management.

- Public record information affects approval decisions: Tax liens, judgments, or bankruptcy filings on business credit reports could significantly impact DSCR loan eligibility, even with strong rental property financing projections.

- Financial statement consistency matters: Discrepancies between business credit reports and submitted financial statements might trigger additional documentation requests or underwriting delays.

Improving Business Credit Score for Better DSCR Terms

Improving business credit score for better DSCR terms requires strategic planning and consistent execution, especially as lenders implement more stringent qualification standards. Investors who actively manage their business credit profiles often secure more favorable interest rates and loan terms.

- Establishing vendor trade lines builds credit foundation: Regular payments to suppliers, utilities, and service providers that report to business credit bureaus help establish positive payment history and improve credit scores over time.

- Business credit card management affects scores significantly: Maintaining low balances relative to credit limits while making timely payments demonstrates responsible credit management to potential DSCR lenders.

- Dispute resolution improves credit accuracy: Addressing incorrect information on business credit reports through formal dispute processes might result in score improvements that enhance loan qualification prospects.

- Credit monitoring enables proactive management: Regular monitoring helps investors identify score changes quickly, allowing them to address issues before they impact important DSCR loan applications.

Strategic Steps for Optimizing DSCR Loan Success

Strategic steps for optimizing DSCR loan success combine business credit management with broader portfolio planning. As product innovation continues reshaping the DSCR lending landscape, investors need comprehensive approaches that address both credit score requirements and market opportunities.

- Develop comprehensive credit improvement timeline: Create a 6-12 month plan addressing specific business credit weaknesses while maintaining current investment momentum, allowing time for meaningful score improvements before major acquisitions.

- Build relationships with multiple DSCR lenders: Establish connections with various lenders who have different credit requirements and risk tolerances, creating options when opportunities arise in high-growth rental markets.

- Coordinate credit activities with investment goals: Time business credit building activities around planned property purchases, ensuring credit profiles peak when needed for important DSCR loan applications.

- Document business credit improvements systematically: Maintain detailed records of credit enhancement efforts and score changes, creating compelling narratives for lenders about financial responsibility and investment experience.

- Leverage business credit for portfolio scaling: Use improved business credit scores to access better DSCR loan terms, enabling more efficient cash flow management and faster portfolio expansion in target markets.

●Conclusion

Your business credit score increasingly determines DSCR loan success as lenders implement stricter underwriting standards throughout 2026. While these loans focus primarily on rental income potential, comprehensive credit evaluation remains central to approval decisions and loan terms. Investors who proactively manage their business credit profiles position themselves for better financing opportunities in competitive markets.

The evolving DSCR lending landscape rewards preparation and strategic thinking. By understanding how business credit scores affect loan applications, regularly monitoring credit reports, and implementing improvement strategies, investors can access more favorable financing terms. This enhanced access to capital becomes particularly valuable when targeting high-growth rental markets or executing cash-out refinance strategies for portfolio expansion.

Success in today's DSCR lending environment requires balancing multiple factors: strong rental income projections, solid business credit profiles, and strategic market timing. Investors who master this combination will find themselves better positioned to capitalize on the opportunities that innovative DSCR loan products continue to provide in an evolving real estate investment landscape.