An adjustable-rate mortgage, or ARM, can feel like a smart choice when interest rates are low. But as rates shift, your monthly payment can climb in ways that strain your budget. Many homeowners in this situation start looking for a way out — and refinancing into a fixed-rate loan is often the most popular solution. The challenge, though, is that refinancing typically comes with closing costs that can run into the thousands of dollars. That's where no closing cost refinance options come in. In this guide, we'll walk through the best options for refinancing ARM mortgage with no closing costs, so you can make a confident, informed decision about your home financing strategy.

Understanding How Adjustable-Rate Mortgages Work Before You Refinance

Before exploring your refinancing choices, it helps to understand what makes an ARM tick. An adjustable-rate mortgage typically starts with a fixed interest rate for an initial period — often five, seven, or ten years. After that introductory phase ends, the rate adjusts periodically based on a financial index, such as the Secured Overnight Financing Rate (SOFR), plus a lender margin.

When rates rise, those adjustments can push your monthly payment significantly higher. This unpredictability is one of the main reasons homeowners decide to refinance out of an ARM. Locking into a fixed rate provides payment consistency, which can make budgeting far easier over the long term.

However, timing matters. If your ARM's fixed period hasn't expired yet, you may still have time to refinance without facing a sharp rate increase. On the other hand, if you're already in the adjustment phase, acting sooner rather than later could protect you from further payment creep.

What No Closing Cost Refinancing Really Means for Homeowners

The term "no closing cost refinance" can be a little misleading if you're not familiar with how lenders structure these deals. The costs don't simply disappear — they're handled differently. There are typically two main approaches lenders use:

- Rolling costs into the loan balance: The lender adds the closing costs to your new loan principal. You don't pay them upfront, but you do pay interest on them over the life of the loan.

- Accepting a higher interest rate: In exchange for covering your closing costs, the lender may offer you a slightly higher interest rate. This is often called a "lender credit" arrangement.

Neither approach is inherently bad. For homeowners who don't have thousands in cash readily available, or who plan to sell or refinance again within a few years, a no closing cost structure could make a lot of sense. The key is understanding the trade-off and calculating whether you'll come out ahead based on how long you plan to stay in the home.

It's also worth noting that some fees may still apply even in a no closing cost deal — such as prepaid interest, homeowner's insurance, or escrow deposits. Always ask your lender to itemize what is and isn't covered.

The Best Options for Refinancing ARM Mortgage with No Closing Costs

When evaluating the best options for refinancing ARM mortgage with no closing costs, homeowners have several loan types and lender arrangements to consider. Each comes with its own set of qualifications, benefits, and potential drawbacks.

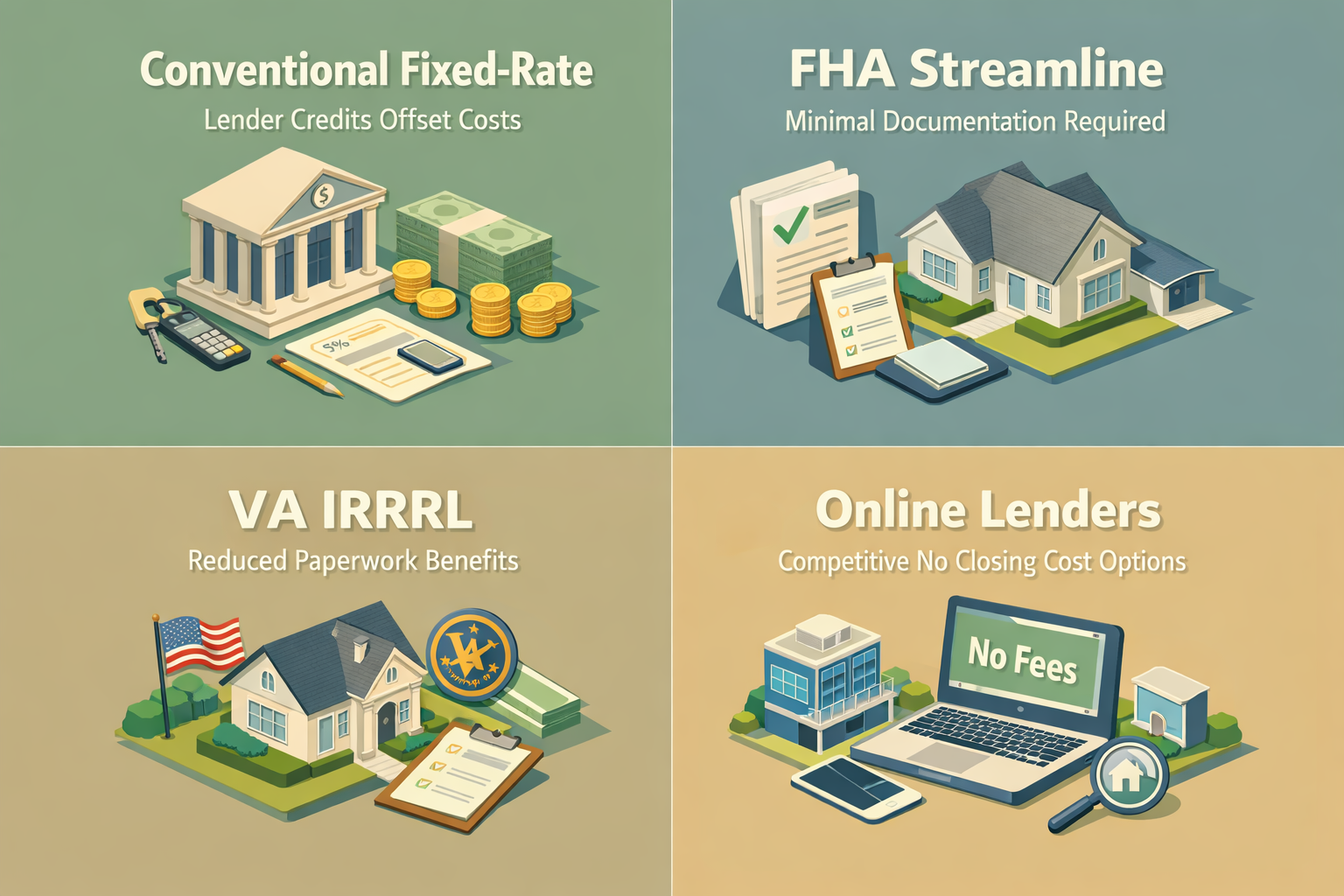

Conventional Fixed-Rate Refinance with Lender Credits

One of the most common routes is refinancing ARM mortgage with no closing costs into a conventional fixed-rate mortgage while using lender credits to offset closing costs. Many banks, credit unions, and mortgage lenders offer this structure. You'll typically need a credit score of 620 or higher, a stable income history, and sufficient equity in your home — usually at least 20% to avoid private mortgage insurance (PMI).

Borrowers with strong credit profiles may find that the rate increase associated with lender credits is relatively modest, making this a cost-effective path forward.

FHA Streamline Refinance

If your current mortgage is FHA-backed, you may qualify for an FHA Streamline Refinance. This program is designed to reduce the interest rate on an existing FHA loan with minimal documentation and, in many cases, limited out-of-pocket costs. While it's typically used to lower rates rather than switch loan types, it can be a helpful option if your ARM is an FHA loan.

Keep in mind that the FHA Streamline Refinance does come with mortgage insurance premiums, which could affect your overall savings. It's worth running the numbers carefully with a licensed mortgage professional.

VA Interest Rate Reduction Refinance Loan (IRRRL)

Eligible veterans and active-duty service members with a VA loan may have access to the VA IRRRL — sometimes called the VA Streamline Refinance. This program allows VA borrowers to refinance from an ARM to a fixed-rate loan with reduced paperwork and potentially no out-of-pocket costs, depending on how the loan is structured. The VA funding fee may be rolled into the loan balance.

The VA IRRRL is widely regarded as one of the most borrower-friendly refinance programs available, offering a streamlined path for those who qualify.

No Closing Cost Refinance Through Online Lenders and Credit Unions

The mortgage market has become increasingly competitive, and many online lenders and credit unions now offer no closing cost mortgage refinance options as a standard part of their product lineup. These institutions may have lower overhead costs, which could allow them to offer more favorable terms.

Shopping around and comparing multiple lenders is especially important in this category. Rates, credit requirements, and the specific costs covered under a "no closing cost" label can vary considerably from one lender to the next.

How to Determine If a No Closing Cost Refinance Makes Financial Sense

Not every homeowner will benefit equally from a no closing cost refinance. To figure out whether this approach works for your situation, consider a few key factors.

Your Break-Even Point

In a traditional refinance, you'd calculate how many months it takes for your monthly savings to recoup the upfront closing costs. With a no closing cost refinance, there's no upfront cost to recoup — but if the lender is charging a higher rate, you need to weigh that against your monthly savings compared to your current ARM payment.

If you plan to stay in the home for only a short period, a no closing cost option with a slightly higher rate may actually save you more money than paying costs upfront. If you're planning to stay long-term, a traditional refinance with closing costs might result in lower total interest paid over the life of the loan.

Your Current Equity Position

Lenders typically require a minimum level of home equity to approve a refinance. If your home's value has increased since you purchased it, you may have more equity than you realize, which could open up better loan terms and rate options.

Your Credit Score and Debt-to-Income Ratio

A stronger credit profile generally unlocks better rates and more favorable no closing cost structures. If your credit score has improved since you originally took out your ARM, you may be in a strong position to negotiate favorable terms. Lenders also look at your debt-to-income (DTI) ratio, so reducing other debts before applying could strengthen your application.

Common Pitfalls to Watch Out For When Refinancing an ARM

Refinancing can be a powerful financial move, but it's not without potential missteps. Here are some things to keep in mind as you navigate the process.

- Not reading the fine print: Some lenders advertise no closing costs but exclude certain fees from that promise. Always request a Loan Estimate document so you can see exactly what's included and what isn't.

- Focusing only on the rate: A lower interest rate doesn't automatically mean a better deal. Consider the total cost of the loan, including any rate premium for lender credits, over your expected ownership timeline.

- Ignoring prepayment penalties: Some ARMs — especially older ones — may carry prepayment penalties. Review your current loan documents before committing to a refinance to avoid unexpected fees.

- Refinancing too late: Waiting until your ARM has already adjusted multiple times could mean you've already absorbed significant payment increases. Acting before a scheduled rate adjustment may give you more leverage and better options.

- Skipping professional guidance: Mortgage refinancing involves complex calculations and legal documentation. Working with a licensed mortgage professional can help you avoid costly mistakes and identify opportunities you might otherwise miss.

Steps to Take When You're Ready to Start the Refinancing Process

If you've decided that refinancing your ARM makes sense, here's a practical roadmap to get started.

Step 1: Review Your Current Loan Terms

Pull out your existing mortgage documents and review the remaining fixed period, the adjustment caps, the index your rate is tied to, and any prepayment penalties. Understanding where you stand now makes it easier to evaluate what you're moving toward.

Step 2: Check Your Credit and Financial Profile

Order your credit reports and check for any errors that could be dragging down your score. Pay down high-balance credit cards if possible, and avoid opening new credit accounts before applying for a refinance.

Step 3: Get Multiple Loan Estimates

Don't settle for the first offer you receive. Reach out to at least three lenders — including your current lender, an online lender, and a local credit union or bank — and ask specifically about no closing cost mortgage refinance options. Compare the Loan Estimates side by side to understand the true cost differences.

Step 4: Calculate Your Long-Term Cost

Use an online mortgage calculator or work with a loan officer to model out the total cost of each option over your expected time in the home. Factor in the rate premium for any lender credits, the impact of rolling costs into the loan, and your projected monthly savings.

Step 5: Lock Your Rate and Proceed with the Application

Once you've chosen a lender and a loan structure, ask about rate lock options to protect yourself from market fluctuations during the underwriting process. Gather your financial documents — pay stubs, tax returns, bank statements, and identification — and submit a complete application to move forward efficiently.

●Conclusion

Refinancing an adjustable-rate mortgage doesn't have to be an expensive or overwhelming process. With the right approach and a clear understanding of your options, you could move into a more stable, predictable loan without draining your savings on upfront costs. The best options for refinancing ARM mortgage with no closing costs will ultimately depend on your financial profile, your timeline, and the lenders you work with — so taking the time to compare offers and ask the right questions is well worth the effort. At LoanWise, we're here to help homeowners like you navigate every step of the mortgage refinancing process with confidence. Reach out today to connect with a lending expert who can help you find the solution that fits your unique situation.