When you close on a home, you'll sign a stack of documents — and one of the most important ones is the mortgage note. Yet many homebuyers overlook it or confuse it with other closing paperwork. Understanding what a mortgage note is, what it includes, and how it affects your financial obligations could save you from costly surprises down the road. Whether you're a first-time buyer, a seasoned homeowner refinancing your loan, or a real estate investor building your portfolio, knowing the basics of a mortgage note is a smart move. Let's break it all down in plain language.

What a Mortgage Note Actually Is

A mortgage note — sometimes called a promissory note or loan note — is a legal document that spells out your promise to repay a specific amount of money to a lender under agreed-upon terms. Think of it as your written commitment to the loan. It's the document that makes the debt official and legally enforceable.

While the mortgage or deed of trust ties the loan to the property itself as collateral, the mortgage note focuses on you — the borrower. It documents your personal obligation to repay the debt, regardless of what happens to the property. That's a distinction worth understanding before you sign.

In simple terms, the mortgage is what gives the lender the right to foreclose if you default. The note is what gives them the right to collect the debt from you personally. Both documents work together, but they serve different legal purposes.

Key Details Found Inside a Mortgage Note

A mortgage note typically contains several critical pieces of information. Reviewing each one carefully before closing can help you avoid misunderstandings later. Here's what you'll commonly find:

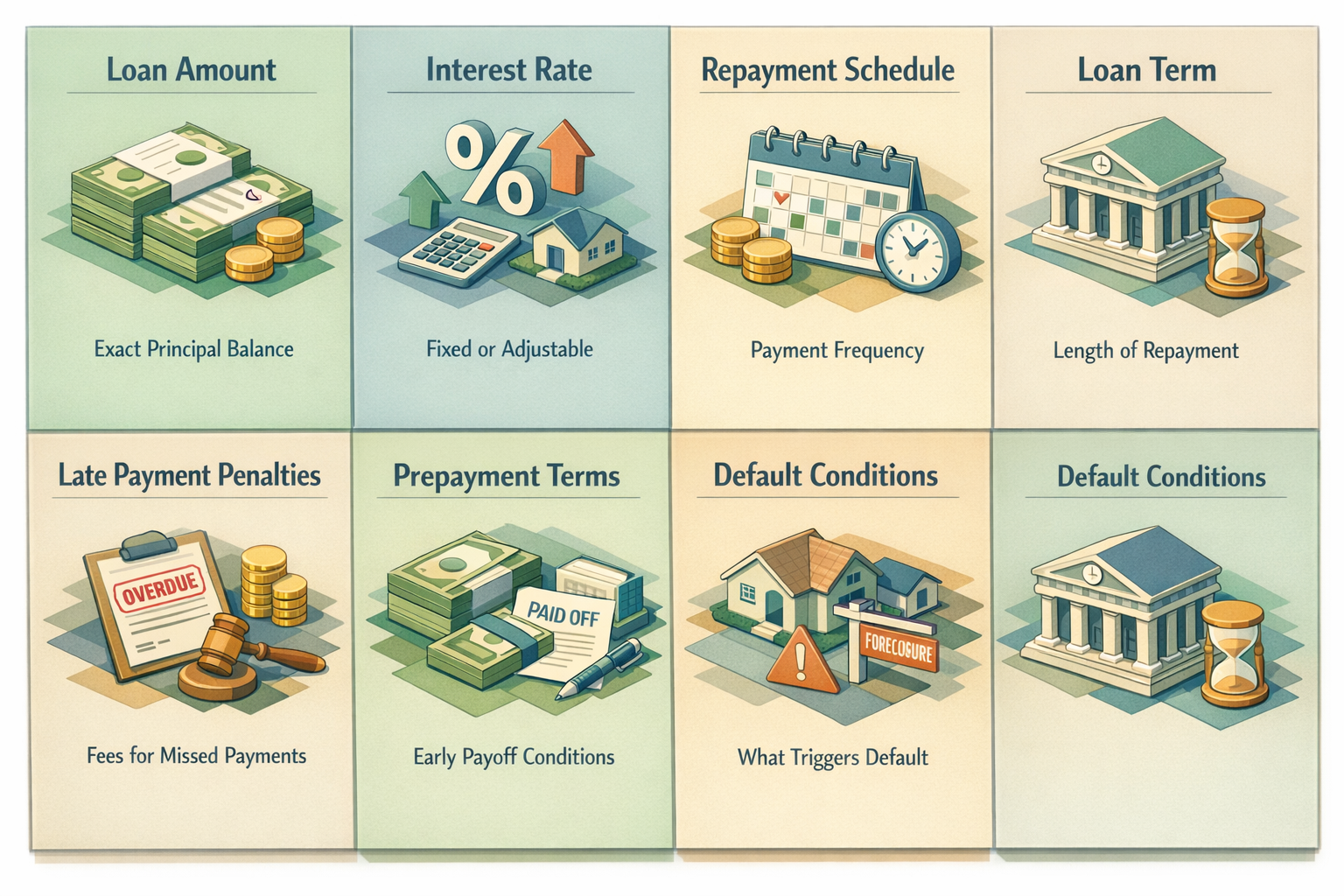

- Loan amount: The exact principal balance you're borrowing from the lender.

- Interest rate: Whether your rate is fixed or adjustable, and the specific percentage that applies to your loan.

- Repayment schedule: How often payments are due (usually monthly), and when they're considered late.

- Loan term: The length of time you have to repay the loan — often 15, 20, or 30 years.

- Late payment penalties: What fees may apply if you miss a due date or pay after the grace period.

- Prepayment terms: Whether you can pay off your loan early and if any penalties might apply for doing so.

- Default conditions: What constitutes a default and what actions the lender may take if it occurs.

It's worth reading through all of these terms carefully — ideally with the help of a real estate attorney or a trusted mortgage advisor. Some details, like prepayment penalties or rate adjustment caps on an adjustable-rate loan, could have a meaningful impact on your long-term costs.

Fixed vs. Adjustable Rate Notes: What Borrowers Should Understand

One of the most significant details in any mortgage note is how your interest rate is structured. This directly affects how much you'll pay each month and over the life of the loan.

A fixed-rate mortgage note locks in your interest rate for the entire loan term. Your monthly principal and interest payment stays the same from the first payment to the last. This makes budgeting more predictable and may be a strong choice for buyers who plan to stay in their home long-term or who prefer financial stability.

An adjustable-rate mortgage note, on the other hand, typically starts with a lower introductory rate that can change periodically based on a market index. Your note will specify the initial rate period, how often adjustments occur, and how much the rate can move up or down at each adjustment — known as rate caps. Borrowers who plan to sell or refinance within a few years might find an adjustable-rate structure appealing, though there's always some degree of uncertainty involved with future rate changes.

Understanding which type of note you're signing is essential. If you're unsure about any terms in the document, ask questions before closing day — not after.

How a Mortgage Note Differs From a Deed of Trust or Mortgage

Many homebuyers use the terms "mortgage" and "mortgage note" interchangeably, but they're actually two separate legal instruments. Understanding the difference matters, especially if you ever face a dispute with your lender or need to refinance.

The mortgage note is your personal promise to repay. It's the debt instrument. It doesn't describe the property or give the lender any rights to the home itself — it simply documents your financial obligation.

The mortgage (or deed of trust, depending on your state) is a security instrument. It links the loan to the property and gives the lender the legal right to foreclose if you stop making payments. In states that use a deed of trust, a third-party trustee holds the title until the loan is paid off.

Together, these documents form the legal foundation of your home loan. Your mortgage note travels with the debt — meaning if your lender sells your loan to another servicer (which is common), the note transfers to the new holder. The new servicer then has the right to collect your payments. This is why it's important to keep a copy of your signed mortgage note for your own records.

What Happens to Your Mortgage Note Over Time

Once you sign your mortgage note, it doesn't just sit in a filing cabinet and collect dust. It becomes an active legal and financial instrument that can move through the lending system in several ways.

Lenders frequently sell mortgage notes on the secondary market — to entities like Fannie Mae or Freddie Mac — as a way of freeing up capital to fund new loans. When this happens, your loan terms don't change, but the company collecting your payments (your loan servicer) might. If you ever receive a notice that your loan has been transferred, don't panic. Your original note terms remain in effect.

Over time, as you make payments, the principal balance listed in your note decreases. Eventually, when you've made your final payment, the lender is required to release the lien and provide documentation showing the debt has been satisfied — sometimes called a "satisfaction of mortgage" or "deed of reconveyance." Holding onto this document is important for your property records.

If you refinance your home, your existing mortgage note is effectively paid off and replaced with a new one reflecting your updated loan terms. This is why refinancing is sometimes described as taking out a new mortgage — because you're essentially signing a fresh note.

Important Considerations Before Signing Your Loan Documents

Closing day can feel overwhelming with the volume of paperwork involved. But taking the time to review your mortgage note carefully is one of the most valuable things you can do as a borrower. Here are some practical tips to keep in mind:

- Request your documents in advance: Ask your lender or closing attorney to provide your loan documents a day or two before closing so you have time to review them without pressure.

- Compare to your Loan Estimate: The terms in your mortgage note should closely align with the Loan Estimate you received earlier in the process. Flag any discrepancies immediately.

- Check the rate type and caps: Confirm whether your rate is fixed or adjustable, and if adjustable, understand the caps that limit how much your rate can move.

- Review the prepayment clause: Some notes include penalties for paying off the loan early. This may affect your plans if you're considering refinancing or selling in a few years.

- Understand default provisions: Know what could trigger a default and what options you'd have — such as a forbearance or loan modification — if you ran into financial hardship.

If anything in your mortgage note is unclear, don't hesitate to ask your lender or a licensed real estate professional to walk you through it. You have every right to understand what you're agreeing to before you sign.

●Conclusion

A mortgage note is more than just another piece of closing paperwork — it's the legal backbone of your home loan. It defines your repayment obligations, your interest terms, and the conditions under which your lender can act if things go wrong. Whether you're buying your first home, refinancing for a better rate, or investing in real estate, taking the time to understand your mortgage note could help you make smarter, more confident financial decisions. At LoanWise, we believe informed borrowers are empowered borrowers. If you're ready to explore your home financing options or need guidance on your loan documents, our team is here to help every step of the way.