Buying a high-value home is an exciting milestone, but it often comes with a financing challenge that many buyers don't expect: standard loan limits. When the purchase price of a property exceeds what conventional conforming loans allow, homebuyers may need to turn to a jumbo loan. These mortgages are designed specifically for properties that fall outside the boundaries set by federal housing agencies, and they come with their own set of rules, requirements, and considerations. Whether you're purchasing a luxury property, a home in a high-cost market, or a large estate, understanding how jumbo loans work could be the key to securing the financing you need.

What Makes a Jumbo Loan Different from a Conforming Loan

To understand a jumbo loan, it helps to first understand what a conforming loan is. Conforming loans are mortgages that meet the guidelines established by Fannie Mae and Freddie Mac, two government-sponsored enterprises that purchase loans from lenders and sell them on the secondary market. These guidelines include a maximum loan amount, which is updated annually by the Federal Housing Finance Agency (FHFA).

When a loan exceeds that limit, it's considered a non-conforming loan — and that's exactly where jumbo loans come in. Because lenders can't sell jumbo loans to Fannie Mae or Freddie Mac, they take on more risk by keeping them in their own portfolios. As a result, lenders typically apply stricter qualification standards to protect their investment.

Conforming loan limits can vary by location. In most areas of the United States, the standard limit applies. However, in designated high-cost areas — such as parts of California, New York, and Hawaii — higher baseline limits may apply. Any mortgage that exceeds these thresholds, regardless of location, falls into jumbo territory.

How Jumbo Loan Rates Compare to Standard Mortgages

One common question among homebuyers is whether jumbo loans carry higher interest rates. Historically, jumbo mortgage rates were noticeably higher than conforming loan rates, largely because lenders bore more risk. However, market conditions have shifted over the years, and today the gap between jumbo and conforming rates is often narrower than many buyers expect.

In some rate environments, jumbo loan rates have even been competitive with — or slightly below — conforming loan rates. This can happen when lenders are eager to attract high-net-worth borrowers who present strong credit profiles. That said, rates can fluctuate significantly depending on the lender, the borrower's financial profile, and broader economic conditions.

It's also worth noting that jumbo loans may come with fewer options in terms of loan structure. While 30-year and 15-year fixed-rate jumbo mortgages are commonly available, the range of adjustable-rate and government-backed options is typically more limited compared to conforming loans. Borrowers should shop around and compare offers from multiple lenders to find the most competitive terms.

Qualifying for a Jumbo Loan: Credit, Income, and Assets

Because jumbo loans aren't backed by federal agencies, lenders tend to apply more rigorous qualification criteria. Understanding what's typically required can help you prepare before applying.

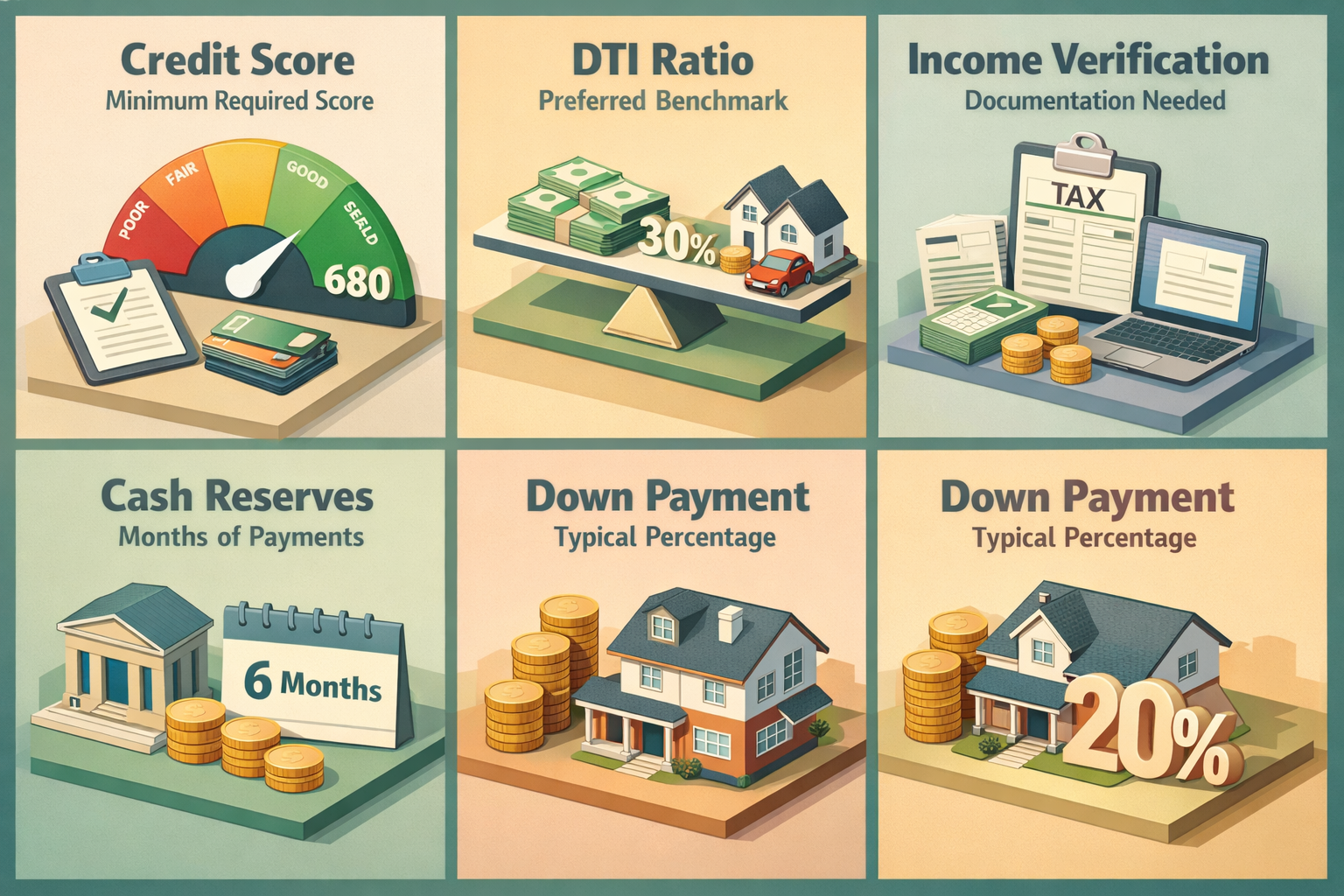

- Credit score: Most lenders require a higher minimum credit score for jumbo loans compared to conforming mortgages. A score of 700 or above is often the baseline, though some lenders may look for 720 or higher to offer the most favorable rates.

- Debt-to-income ratio (DTI): Lenders generally prefer a lower DTI for jumbo borrowers. A ratio at or below 43% is a common benchmark, though stricter lenders may require even lower ratios depending on the loan size and borrower profile.

- Income verification: Jumbo loan applicants typically face more thorough income documentation requirements. Lenders may request multiple years of tax returns, W-2s, bank statements, and proof of consistent income sources.

- Cash reserves: A key distinguishing factor for jumbo loans is the cash reserve requirement. Lenders may want to see anywhere from 6 to 18 months — or more — of mortgage payments held in liquid assets after closing.

- Down payment: While conforming loans may allow down payments as low as 3%, jumbo loans typically require a more substantial upfront investment, often starting around 10% to 20% or higher, depending on the loan amount and lender.

These requirements can vary considerably from one lender to another, so it's wise to consult with a knowledgeable mortgage professional who can guide you toward lenders with criteria that match your financial situation.

The Appraisal Process for High-Value Properties

One area where jumbo loans differ meaningfully from standard mortgages is in the appraisal process. Because high-value and luxury properties are less common, finding comparable sales — often called comps — can be more challenging. Lenders want to be confident that the property's value supports the loan amount, which sometimes leads to more detailed or even dual appraisals.

Some lenders require two independent appraisals for larger jumbo loans, particularly when the property is unique, located in a rural area, or priced significantly above local market norms. This extra step adds time and cost to the closing process, but it gives lenders greater confidence in the collateral backing the loan.

For buyers, this means it's especially important to work with a real estate agent who has experience with luxury or high-value transactions. An agent familiar with this segment of the market can help set realistic price expectations and ensure the transaction timeline accounts for the additional due diligence involved.

Who Is a Jumbo Loan Best Suited For

A jumbo loan isn't just for buyers of sprawling estates or beachfront mansions. In many high-cost metropolitan areas, even moderately sized homes can carry price tags that push them into jumbo territory. Understanding who typically benefits from this type of financing a high-value home can help you decide whether it's the right path for your homebuying journey.

Jumbo loans tend to work best for borrowers who have strong financial profiles, including excellent credit, stable high income, substantial savings, and low existing debt. These are often professionals, business owners, real estate investors, or executives who are purchasing primary residences, vacation homes, or investment properties in competitive markets.

That said, self-employed buyers or those with non-traditional income sources may face additional documentation hurdles, even if their overall financial picture is strong. Some lenders offer non-QM (non-qualified mortgage) jumbo products specifically designed for borrowers who don't fit the traditional income verification mold. These programs can be worth exploring if your income structure is complex.

Real estate investors purchasing high-value rental properties or multi-unit buildings may also find jumbo financing relevant, though lenders will likely apply additional scrutiny to rental income projections and property cash flow.

Tips for Improving Your Jumbo Loan Approval Odds

If you're planning to apply for a jumbo mortgage, a little advance preparation can go a long way. Here are some practical steps that may strengthen your application:

- Build and protect your credit: Review your credit report for any errors and work to resolve outstanding issues well before applying. Avoid opening new credit accounts or making large purchases in the months leading up to your application.

- Document everything: Gather at least two years of tax returns, recent pay stubs, bank statements, and any documentation of additional income sources such as investments, rental income, or business distributions.

- Reduce your debt load: Paying down existing debts before applying can improve your debt-to-income ratio and make your application more attractive to lenders.

- Increase your liquid reserves: Demonstrating robust savings beyond your down payment signals financial stability to lenders. The more reserves you can show, the more confidence lenders may have in your ability to manage a large loan.

- Work with a specialist: Not every mortgage lender offers jumbo products, and those that do may have very different requirements. Working with a broker or lender who specializes in high-value financing can help you find the best fit for your needs.

Being proactive about your financial health before applying could meaningfully improve your chances of approval and help you secure more favorable loan terms.

●Conclusion

Jumbo loans open the door to financing properties that fall beyond the reach of standard conforming mortgages, but they require careful preparation and a solid financial foundation. From higher credit score expectations to larger down payments and more detailed documentation, the qualification process is more demanding — yet entirely achievable for well-prepared buyers. If you're considering a high-value home purchase, refinancing an existing jumbo mortgage, or simply exploring your options in a competitive market, speaking with an experienced lending professional could be your most valuable next step. At LoanWise, we're here to help you navigate the complexities of high-value home financing with confidence and clarity.