When most people think about home financing, they picture a traditional mortgage tied to a house sitting on a permanent foundation. But not every home fits that mold — and that's where a chattel mortgage enters the picture. If you're considering a manufactured home, mobile home, or other movable property, understanding this type of financing could open doors you didn't know existed. In this guide, we'll walk you through exactly what a chattel mortgage is, how it differs from a conventional home loan, and what you should think about before applying.

Understanding What a Chattel Mortgage Actually Means

A chattel mortgage is a loan secured by movable personal property — often called "chattel" — rather than real property like land. In the context of home financing, this typically applies to manufactured homes or mobile homes that are not permanently affixed to land owned by the borrower. In these cases, the home itself serves as collateral for the loan, much like a vehicle secures an auto loan.

The word "chattel" is an older legal term referring to any tangible, movable asset. When a lender extends a chattel mortgage, they hold a security interest in that personal property. If the borrower defaults, the lender may have the right to repossess the home. This structure is meaningfully different from a traditional mortgage, where both the land and the structure are typically used as collateral.

Chattel mortgages are most commonly used in situations where:

- The homebuyer owns or rents the land separately from the home

- The home is located in a manufactured housing community or mobile home park

- The home has not been converted to real property through a process called "titling" or "affixation"

It's worth noting that because the home is classified as personal property rather than real estate, chattel loans are often governed by different regulations and lending standards than conventional mortgages.

How a Chattel Mortgage Differs From a Traditional Home Loan

Understanding the distinctions between a chattel mortgage and a conventional mortgage can help you make a more informed decision. The differences touch on collateral, interest rates, loan terms, and regulatory protections.

Collateral and Property Classification

In a traditional mortgage, the lender places a lien on both the structure and the land beneath it. With a chattel mortgage, only the home itself secures the loan. This means if you're renting the land your manufactured home sits on, a chattel mortgage may be your primary financing option since you don't own the underlying real estate.

Interest Rates and Loan Costs

Chattel mortgages typically carry higher interest rates than conventional home loans. Because the collateral — a movable home — is considered higher risk by lenders, they may price that risk into the loan's terms. Borrowers should carefully review the annual percentage rate (APR) and total loan costs before committing, since even a small rate difference can add up significantly over a multi-year loan term.

Loan Terms and Amounts

Chattel loans often come with shorter repayment periods than traditional 30-year mortgages. Terms might range from 15 to 25 years in many cases, though this can vary by lender and borrower profile. Loan amounts may also be more limited, reflecting the lower appraised value of a home classified as personal property.

Regulatory Differences

Traditional mortgages are subject to federal lending protections under laws like the Real Estate Settlement Procedures Act (RESPA) and the Truth in Lending Act (TILA). Chattel loans, being personal property loans, may not carry all of the same federal protections, though the Consumer Financial Protection Bureau (CFPB) does provide some oversight. Borrowers are encouraged to review their loan disclosures carefully and ask lenders about applicable consumer protections.

Who Typically Uses a Chattel Mortgage?

Chattel mortgages serve a specific segment of the housing market, and understanding who uses them can help you determine whether this type of financing applies to your situation.

Manufactured home buyers are the most common borrowers. Many manufactured homes — particularly those placed in land-lease communities — are financed through chattel loans because the buyer doesn't own the lot. According to industry data, a significant share of manufactured home purchases are financed through chattel rather than real property loans.

Other potential users include:

- Mobile home park residents who rent their lot and need financing for the home itself

- Rural property buyers who may be placing a manufactured home on land they're purchasing separately

- Buyers with limited down payment savings who find that chattel loan entry points are sometimes more accessible than conventional mortgage minimums

- Real estate investors who acquire manufactured homes as rental properties in land-lease communities

It's important to recognize that chattel mortgage borrowers tend to skew toward lower- and moderate-income households. This makes the cost and terms of these loans especially significant from a financial planning perspective. If you fall into this category, comparing multiple lenders and loan offers is particularly worthwhile.

Key Eligibility Factors Lenders Consider for Chattel Loans

If you're considering applying for a chattel mortgage, it helps to understand what lenders typically look at when reviewing your application. While specific requirements vary from one lender to the next, several common factors tend to influence approval decisions.

Credit Score

Your credit score plays a significant role in chattel loan eligibility, just as it does with most types of financing. Lenders may look for a minimum score in the 580 to 640 range for some programs, though higher scores generally lead to better rates and terms. If your credit score needs improvement, taking time to reduce outstanding balances and address any errors on your credit report before applying could be a smart move.

Income and Debt-to-Income Ratio

Lenders want to see that you have enough stable income to cover monthly loan payments alongside your other financial obligations. Your debt-to-income (DTI) ratio — the percentage of your gross monthly income going toward debt payments — is a key metric. A lower DTI ratio typically signals less financial risk to the lender.

Down Payment

Chattel loans may require a down payment, often ranging from 5% to 20% or more depending on the lender and the borrower's credit profile. Some specialty programs for manufactured housing may offer lower down payment options, so it's worth exploring multiple lenders.

Home Age and Condition

Lenders may have restrictions on the age or condition of the manufactured home being financed. Older homes or those in poor condition may not qualify for certain chattel loan programs. Homes built after June 15, 1976 — when the U.S. Department of Housing and Urban Development (HUD) established federal construction and safety standards — are generally more financeable than older units.

Chattel Mortgage Pros and Cons Worth Knowing Before You Decide

Like any financing product, a chattel mortgage comes with both advantages and drawbacks. Weighing them honestly against your personal situation is the best way to decide if this path makes sense for you.

Potential Advantages

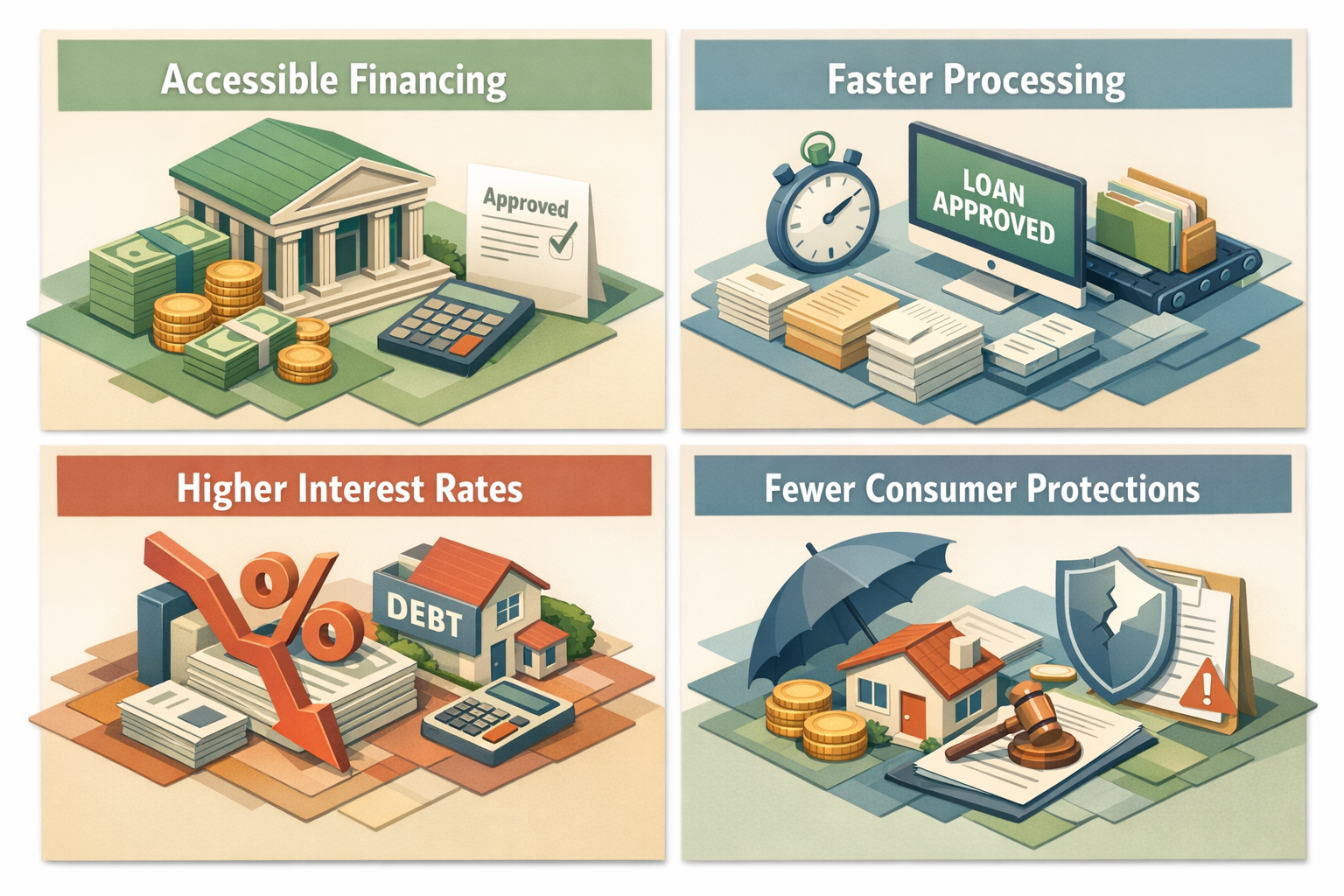

- Accessible financing: For buyers who don't own land, a chattel mortgage may be one of the few realistic financing options available for a manufactured home purchase.

- Faster processing: Chattel loans can sometimes close faster than traditional mortgages because the transaction doesn't involve real estate title searches and certain other steps.

- Lower purchase price entry point: Manufactured homes often cost less than site-built homes, making homeownership more attainable for buyers on a budget — even with chattel loan terms factored in.

Potential Drawbacks

- Higher interest rates: As noted earlier, chattel loans typically carry higher rates than conventional mortgages, which can increase the total cost of borrowing over time.

- Fewer consumer protections: Borrowers may have less federal regulatory protection compared to those with traditional real estate mortgages.

- Depreciation risk: Manufactured homes classified as personal property may depreciate rather than appreciate in value, depending on market conditions and maintenance.

- Limited refinancing options: Refinancing a chattel loan can be more complex and may come with fewer program choices than refinancing a conventional mortgage.

Taking the time to run the numbers — including total interest paid over the life of the loan — can help you assess the true cost of this financing option relative to alternatives.

Exploring Alternative Financing Paths for Manufactured Homes

A chattel mortgage isn't the only way to finance a manufactured home, and depending on your circumstances, another option might serve you better. Here are a few alternatives worth researching:

FHA Title I and Title II Loans

The Federal Housing Administration (FHA) offers two manufactured housing loan programs. Title I loans can be used to finance manufactured homes even when the borrower doesn't own the land. Title II loans apply to manufactured homes that are permanently affixed to land the borrower owns and are classified as real property. Title II loans often come with terms more similar to conventional mortgages.

Fannie Mae MH Advantage and Freddie Mac CHOICEHome

Both Fannie Mae and Freddie Mac offer specialty programs designed to bring conventional-style financing to certain manufactured homes that meet specific construction and design standards. These programs may offer lower rates and longer terms than traditional chattel loans, though qualifying homes must meet particular criteria.

VA and USDA Loans

Eligible military veterans and rural buyers may have access to VA or USDA loan programs that cover certain manufactured housing scenarios. Eligibility requirements, property standards, and financing conditions vary, so speaking with a lender familiar with these programs is a good starting point.

Converting to Real Property

In some cases, it may be possible to convert a manufactured home from personal property to real property by permanently affixing it to land you own and retiring the vehicle title. This conversion could open the door to conventional mortgage financing with potentially better terms. The process and requirements vary by state, so consulting with a local real estate attorney or lending professional is advisable.

●Conclusion

A chattel mortgage can be a practical and accessible path to homeownership for buyers of manufactured or mobile homes — especially when land ownership isn't part of the equation. However, it's important to go in with clear eyes about the higher costs, shorter terms, and different regulatory environment that often accompany these loans. Whether you're a first-time homebuyer exploring your options, a real estate investor evaluating manufactured housing, or a homeowner considering your refinancing paths, understanding how chattel financing works puts you in a stronger position to make confident decisions. At LoanWise, we believe every borrower deserves clear, honest information. Take the time to compare lenders, review all loan disclosures carefully, and consider speaking with a housing counselor or mortgage professional before moving forward.