If you're a first-time homebuyer or someone looking to purchase a home with a lower down payment, an FHA loan could be one of the most accessible financing options available to you. Backed by the Federal Housing Administration, FHA loans are designed to help borrowers who may not qualify for conventional financing due to credit challenges or limited savings. But before your lender can approve your application, you'll need to provide a comprehensive set of documents that verify your identity, income, employment, assets, and more. Knowing what documents are needed for FHA loan application ahead of time can save you significant time and stress. This guide walks you through every major document category so you can walk into the process fully prepared.

Why FHA Loan Documentation Matters More Than You Think

FHA loans are government-backed mortgage products, which means lenders must follow specific federal guidelines when evaluating borrowers. Because the Federal Housing Administration insures these loans against default, lenders are required to verify that applicants meet minimum eligibility standards before approving financing. This verification process is almost entirely document-driven.

Unlike some alternative lending products that rely on stated income or minimal paperwork, FHA loans require thorough documentation at every stage. Your lender needs to confirm that you earn enough to make your monthly mortgage payments, that your credit history reflects responsible borrowing behavior, and that your down payment funds come from an eligible source. Each document you provide helps build the complete financial picture your lender needs to move forward.

The good news is that once you know what to gather, the process becomes much more manageable. Most of the documents involved are things you likely already have on hand or can obtain quickly from your employer, bank, or the IRS. Being organized from the start can help prevent unnecessary delays and improve your overall experience.

Proof of Identity and Legal Residency Requirements

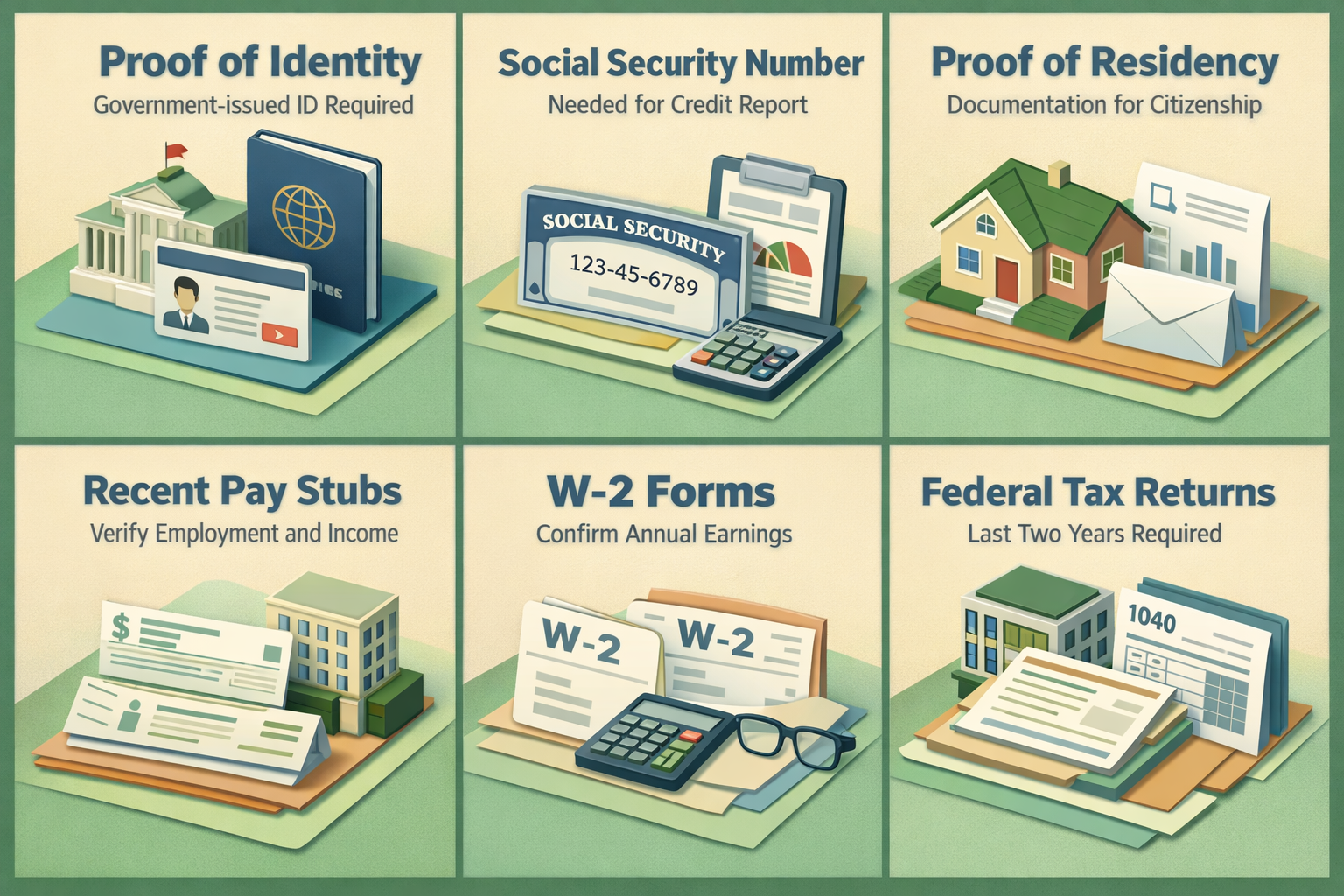

Every FHA loan application begins with verifying who you are. Lenders need to confirm your legal identity and, in some cases, your citizenship or residency status before proceeding with any other part of the review. Here's what you'll typically need to provide:

- Government-issued photo ID: A valid driver's license, state ID, or passport is usually required. This confirms your identity and ensures your application matches your financial records.

- Social Security number: Your SSN is used to pull your credit report and verify your employment history. Some lenders may ask for your Social Security card as additional confirmation.

- Proof of residency or immigration status: U.S. citizens, permanent residents, and certain non-permanent resident aliens may be eligible for FHA loans. Non-citizens will typically need to provide documentation such as a green card or valid work visa.

Having clean, legible copies of these documents ready to submit electronically or in person can help keep your application moving without unnecessary back-and-forth with your loan officer.

FHA Loan Document Checklist: Proof of Income for FHA Loan

Income verification is one of the most important components of any FHA loan application. Lenders use your income documents to calculate your debt-to-income ratio, which helps determine how much you can reasonably afford to borrow. Here's a breakdown of the most commonly requested income documents:

- Recent pay stubs: Most lenders request your two most recent pay stubs to verify current employment and gross monthly income. Pay stubs should clearly show your employer's name, your pay frequency, and year-to-date earnings.

- W-2 forms: You'll typically need W-2s from the past two years. These forms confirm your annual earnings from each employer and help lenders identify any significant income fluctuations.

- Federal tax returns: Lenders usually request the last two years of complete federal tax returns, including all schedules. Tax returns are especially important for borrowers with variable income, investment income, or rental income.

- Profit and loss statements (self-employed borrowers): If you're self-employed, you may also need to provide a year-to-date profit and loss statement prepared by a licensed accountant, along with business tax returns.

- Additional income documentation: If you receive alimony, child support, Social Security benefits, disability income, or retirement distributions, you may need to provide award letters, court orders, or benefit statements to document those sources.

When it comes to proof of income for FHA loan applications, consistency matters. Lenders may flag significant unexplained gaps in employment history or sudden income changes, so be prepared to provide written explanations if your income history has any irregularities.

Understanding FHA Loan Credit Requirements and What to Provide

One of the reasons FHA loans are so popular among first-time homebuyers is their relatively flexible approach to credit. While FHA loan credit requirements are generally more lenient than those for conventional mortgages, lenders still need to review your full credit profile to assess your borrowing risk.

You won't need to gather your own credit report since your lender will pull it directly. However, there are a few credit-related items you should be prepared to address:

- Explanation letters: If your credit report shows late payments, collections, charge-offs, or other derogatory items, your lender may request a written letter of explanation. Being proactive and honest in these letters can strengthen your application.

- Bankruptcy or foreclosure documents: If you've gone through a bankruptcy or foreclosure in recent years, you may need to provide court discharge paperwork or related documents. FHA guidelines typically require a waiting period after these events before you can qualify.

- Landlord references or rental payment history: For borrowers with thin credit files, some lenders may accept alternative credit documentation such as 12 months of on-time rent payment records or utility bills to help establish creditworthiness.

It's worth reviewing your credit report before you apply so you're not caught off guard by anything on your file. Addressing errors or outstanding issues in advance could potentially improve your credit standing and help you secure more favorable loan terms.

FHA Loan Down Payment Documentation and Asset Verification

FHA loans are known for requiring a down payment as low as 3.5% for borrowers who meet the minimum credit score threshold. However, lenders need to verify that the funds you're using for your down payment and closing costs are legitimate and eligible under FHA guidelines. This is where FHA loan down payment documentation becomes essential.

- Bank statements: Most lenders request two to three months of complete bank statements for all checking, savings, and investment accounts. These statements should show your account balances, transaction history, and any large deposits.

- Gift letter (if applicable): FHA loans allow borrowers to use gift funds from family members, employers, or approved nonprofit organizations for the down payment. If any portion of your down payment is a gift, you'll need a signed gift letter stating the amount, the donor's relationship to you, and that the funds do not need to be repaid.

- Documentation for large deposits: If your bank statements show any large or unusual deposits, your lender may ask you to explain and document the source of those funds. This is to ensure that no undisclosed debt was taken on to fund the down payment.

- Retirement and investment account statements: If you're drawing from a 401(k), IRA, or brokerage account, you'll need current statements showing the available balance and, if applicable, documentation of any withdrawal or loan from the account.

Being transparent about where your down payment funds come from is critical. FHA guidelines are designed to ensure that borrowers have genuine equity in their home from the start, rather than funding a purchase entirely with borrowed money from unofficial sources.

Property-Related Documents and What Lenders May Request

Beyond your personal financial documents, your lender will also need information about the property you're purchasing. Some of these documents are gathered by the lender or their third-party partners, but it's helpful to know what to expect during the process.

- Signed purchase agreement: Once you're under contract, your lender will need a fully executed copy of the purchase agreement. This document outlines the sale price, closing date, and any contingencies that may affect the loan.

- FHA appraisal report: FHA loans require a special appraisal conducted by an FHA-approved appraiser. This appraisal assesses both the market value of the property and whether it meets FHA minimum property standards for safety, security, and structural soundness. Your lender typically orders this on your behalf.

- Title and homeowner's insurance documentation: Before closing, you'll need to provide evidence of homeowner's insurance coverage. Your lender will also arrange a title search to confirm there are no liens or legal issues that could affect your ownership of the property.

If you're purchasing a condominium with an FHA loan, there may be additional eligibility requirements for the condo development itself. Not all condo projects are FHA-approved, so it's worth confirming the property's status early in your search to avoid surprises later in the process.

●Conclusion

Understanding what documents are needed for FHA loan application is one of the best things you can do to set yourself up for a smooth and successful homebuying experience. From identity verification and income documentation to credit history explanations and down payment proof, each piece of paperwork serves a purpose in helping your lender confirm that you meet FHA eligibility standards. The more organized and prepared you are going into the process, the faster your lender can move your application toward approval. If you're ready to take the next step, consider connecting with a qualified mortgage professional at LoanWise who can walk you through your specific situation, review your FHA loan document checklist, and help you identify any gaps before you formally apply. A little preparation now can make a big difference when it matters most.