Inheriting a property can feel like both a gift and a puzzle. You may suddenly own a home with significant equity, yet accessing that equity isn't always straightforward. One financing option that homeowners and heirs often explore is a Home Equity Line of Credit, commonly known as a HELOC. But if the property came to you through an estate, the lending process involves a few extra steps. Understanding what are the requirements for a HELOC on inherited property can help you move forward with confidence — whether you plan to keep the home, renovate it, or use the funds for other financial goals. This guide breaks down the key eligibility factors lenders typically look for, so you know exactly what to prepare.

Understanding How a HELOC Works on an Inherited Home

A HELOC is a revolving line of credit secured by the equity in a property. It works similarly to a credit card — you borrow what you need, repay it, and borrow again during the draw period. The amount you can access is generally based on a percentage of the home's appraised value minus any existing mortgage balance.

When the property is inherited property rather than purchased, lenders may view the application through a slightly different lens. The core mechanics of a HELOC don't change, but the underwriting process can involve additional documentation to confirm ownership, title clarity, and the borrower's financial standing. Lenders want to feel confident that the collateral — the inherited home — is legally and financially sound before extending a line of credit against it.

It's also worth noting that some lenders may impose a waiting period before they'll approving a HELOC on an inherited property. This seasoning period allows time for the estate to be settled and for the title to transfer properly into the heir's name. Not all lenders apply the same rules, so it's a good idea to shop around and ask about their specific timelines and policies.

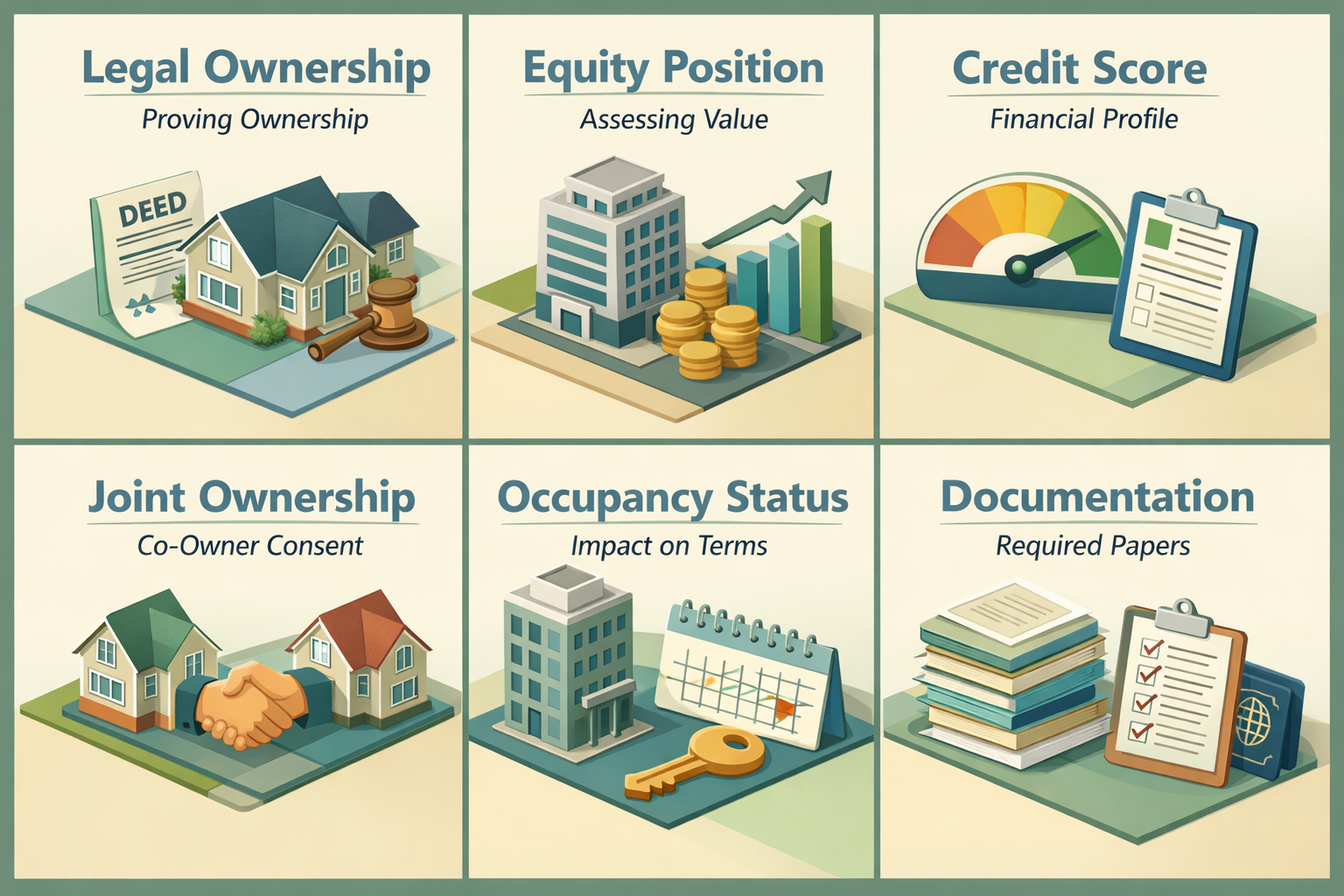

Establishing Clear Title and Legal Ownership

One of the most critical steps when applying for a HELOC on inherited property is proving that you legally own the home. Lenders will not extend credit against a property with disputed or unclear ownership. This means you'll likely need to provide documentation such as:

- A recorded deed showing the property has been transferred into your name

- Letters Testamentary or Letters of Administration if you're still acting as executor of the estate

- A copy of the will or trust document that establishes your right to the property

- Probate court records, if the estate went through probate

Title insurance may also be required. Lenders typically order a title search to confirm there are no outstanding liens, unpaid taxes, or legal claims against the property. If such encumbrances exist, they'll generally need to be resolved before a HELOC can be approved. Working with a real estate attorney during the estate settlement process can help prevent title-related delays down the road.

Equity Position and Appraised Value Requirements

Just like any other HELOC application, lenders will assess how much equity is available in the inherited property. Most lenders use a metric called the Combined Loan-to-Value ratio, or CLTV. This calculation accounts for any existing mortgage balance on the property plus the HELOC amount you're requesting, divided by the home's appraised value.

Lenders typically allow a CLTV of up to 80% to 85%, though this can vary by institution and market conditions. For example, if an inherited home appraises at $400,000 and carries no existing mortgage, you might be able to access a line of credit of up to $320,000 to $340,000, depending on the lender's guidelines.

Here's what typically influences how much equity you can access:

- The current appraised value of the inherited property

- Any outstanding mortgage balance inherited with the home

- The lender's maximum CLTV threshold

- Local real estate market conditions that may affect valuation

If the property has appreciated significantly since it was originally purchased, heirs may find themselves sitting on substantial equity — making a HELOC a potentially attractive option for financing renovations, consolidating debt, or covering other major expenses.

Credit Score and Income Standards Lenders Typically Apply

Beyond the property itself, lenders will carefully evaluate your personal financial profile. A strong credit score is generally a key requirement when applying for a HELOC. While minimum thresholds can vary by lender, many institutions look for a credit score of at least 620, though scores of 700 or higher may help you qualify for better terms and lower interest rates.

Your income and debt-to-income ratio (DTI) will also come under scrutiny. Lenders want to see that you have sufficient, stable income to repay what you borrow. Common income documentation may include:

- Recent pay stubs or W-2 forms for salaried borrowers

- Tax returns and profit-and-loss statements for self-employed applicants

- Bank statements showing consistent cash flow

- Documentation of rental income, retirement distributions, or investment income, if applicable

Most lenders prefer a DTI ratio of 43% or below, meaning your monthly debt obligations — including the projected HELOC payment — shouldn't exceed 43% of your gross monthly income. Meeting these financial benchmarks may significantly improve your chances of approval and help you secure more favorable borrowing terms.

HELOC Eligibility for Jointly Owned Inherited Real Estate

Things can get more complex when a property is inherited by more than one person. HELOC eligibility for jointly owned inherited real estate often requires that all co-owners agree to use the property as collateral. In most cases, every individual who holds title to the property must sign the HELOC agreement, because the lender's lien applies to the entire property — not just one person's share.

This means all co-inheritors would need to:

- Consent to the HELOC and be willing to sign the loan documents

- Meet the lender's creditworthiness standards, or at least not present significant financial red flags

- Agree on how the funds will be used, since the credit line will be tied to a shared asset

If co-owners disagree about taking out a HELOC, it may be necessary to explore alternative options such as buying out the other heirs' shares, partitioning the property, or pursuing other financing avenues. In some situations, working with an estate attorney or a financial advisor before approaching a lender can help co-inheritors reach a shared plan and avoid complications during underwriting.

Occupancy Status and How It May Affect Your Application

Whether the inherited property is your primary residence, a second home, or an investment property can have a meaningful impact on your HELOC terms and eligibility. Lenders generally view primary residences as lower-risk collateral, which may translate to more favorable rates and higher borrowing limits. Non-owner-occupied properties — such as inherited homes that are rented out or left vacant — might face stricter lending criteria.

Here's a general breakdown of how occupancy can affect a HELOC application:

- Primary residence: Typically eligible for the most competitive HELOC terms and higher CLTV allowances

- Second home: May still qualify, but lenders could apply slightly tighter guidelines and higher interest rates

- Investment or rental property: Some lenders offer HELOCs on non-owner-occupied properties, but expect more conservative lending limits and potentially higher rates

If you've moved into the inherited home as your primary residence, be prepared to show proof of occupancy, such as a utility bill or updated driver's license reflecting the new address. This documentation can support your application and help lenders classify the property correctly.

●Conclusion

Understanding what are the requirements for a HELOC on inherited property is the first step toward making a smart financial decision with your newly acquired real estate. From establishing clear title and confirming equity to meeting credit and income standards, each piece of the puzzle matters. If the property was inherited alongside siblings or other family members, the co-ownership dynamic adds another layer of planning that's best addressed early in the process.

The good news is that with the right preparation, a HELOC on inherited property is a realistic option for many heirs. Take time to gather your documentation, review your credit profile, and speak with a licensed mortgage professional who can walk you through the specific guidelines that apply to your situation. At LoanWise, our team is here to help you evaluate your options and move forward with clarity. Reach out today to explore whether a HELOC could be the right fit for your inherited property.