For many homebuyers, an FHA loan is one of the most accessible paths to homeownership. With lower down payment requirements and more flexible credit standards, these government-backed mortgages have helped millions of Americans purchase homes. But before you apply, it's important to understand one key detail: there are limits on how much you can borrow. Understanding FHA loan limits for existing homes is an essential step in planning your purchase, especially if you're buying a resale property in a competitive housing market. In this guide, we'll walk through how those limits are set, how they vary by location, what eligibility rules apply to existing construction, and how FHA stacks up against other government loan programs.

What Are FHA Loan Limits and Why Do They Matter?

FHA loans are insured by the Federal Housing Administration, a division of the U.S. Department of Housing and Urban Development (HUD). Because the federal government backs these loans, they come with specific rules — including caps on how much a borrower can finance. These caps are known as FHA loan limits.

Loan limits exist to keep the program focused on moderate-income buyers purchasing reasonably priced homes. If you're eyeing a luxury property or a high-value resale home, you may find that an FHA loan doesn't cover the full purchase price. In that case, you'd either need to make a larger down payment or explore a different loan product entirely.

Limits are set annually by HUD and are based on local median home prices. This means the cap in a rural county with lower home values will typically be much lower than the cap in a major metropolitan area where prices are higher. The FHA sets a nationwide floor — the minimum loan limit — and a nationwide ceiling — the maximum. Most counties fall somewhere between these two benchmarks.

For homebuyers considering an existing home purchase, knowing the current loan limit in your target area could save you a lot of time and frustration during the financing process.

How FHA Loan Limits Are Determined by County

One of the most important aspects of FHA loan limits by county is that they're not one-size-fits-all. HUD reviews housing market data each year and adjusts limits to reflect local real estate conditions. This geographic flexibility is what makes the FHA program relevant in both affordable rural markets and high-cost urban areas.

Here's how the structure typically works:

- Floor limit: This is the baseline loan limit that applies in lower-cost areas. It's calculated as a percentage of the conforming loan limit set by the Federal Housing Finance Agency (FHFA). Counties where homes are relatively affordable tend to fall at or near this floor.

- Ceiling limit: High-cost areas — like parts of California, New York, Hawaii, and other expensive metros — may qualify for significantly higher loan limits, up to the FHA's national ceiling for single-family homes.

- Special exception areas: Certain locations, including Alaska, Hawaii, Guam, and the U.S. Virgin Islands, may have even higher limits due to elevated construction and living costs.

Because limits are set at the county level, two neighboring counties could have noticeably different FHA maximums. If you're flexible on where you buy, it may be worth checking whether a nearby county has a higher limit that better suits your budget.

Borrowers can look up current county-specific limits through HUD's official resources or by working with an FHA-approved lender who has access to up-to-date limit tables.

Understanding the FHA Loan Maximum for Existing Houses

When people talk about the FHA loan maximum for existing houses, they're referring to how the loan limit applies specifically to resale or previously owned properties — as opposed to new construction. The good news is that the same county-level limits that apply to new homes generally apply to existing homes as well. FHA doesn't typically impose a separate, stricter cap just because a home was previously lived in.

However, while the loan limit itself may not differ, existing homes do face other requirements that could affect how much you can borrow or whether the property qualifies at all. The FHA requires that all financed properties meet minimum property standards (MPS). These standards are designed to ensure that the home is safe, sound, and structurally secure.

For existing homes, common issues that could affect FHA eligibility include:

- Roof condition — the roof must have a remaining useful life of at least two years

- Structural integrity — foundations, walls, and framing must be free of significant defects

- Safety hazards — exposed wiring, broken windows, or lead-based paint on pre-1978 homes may require remediation

- Mechanical systems — heating, plumbing, and electrical systems should be in working order

If a home doesn't meet these standards, the buyer may need to negotiate repairs with the seller or explore the FHA 203(k) rehabilitation loan, which allows borrowers to finance both the purchase and renovation costs in a single loan. This can be a powerful option for buyers interested in fixer-uppers.

FHA Eligibility for Existing Construction: Key Rules to Know

Beyond property condition, FHA eligibility for existing construction also involves borrower qualifications and loan structure requirements. Meeting these criteria is just as important as staying within the loan limit.

From a borrower standpoint, FHA guidelines typically require:

- Minimum credit score: Borrowers with a credit score of 580 or higher may qualify for the standard 3.5% down payment. Those with scores between 500 and 579 might still be eligible but may need to put down 10%.

- Debt-to-income ratio (DTI): FHA guidelines generally allow a DTI of up to 43%, though some lenders may approve higher ratios with compensating factors.

- Primary residence requirement: FHA loans are intended for owner-occupied properties. The borrower must plan to live in the home as their primary residence.

- FHA mortgage insurance: All FHA loans require an upfront mortgage insurance premium (UFMIP) and an annual mortgage insurance premium (MIP). These costs are built into the loan and protect the lender in case of default.

It's also worth noting that FHA loans are only available through FHA-approved lenders. Not every lender offers FHA financing, so working with a lender experienced in government-backed programs can make the process smoother.

For existing construction specifically, an FHA appraisal is required. This appraisal differs from a standard home appraisal because it evaluates both the property's market value and its compliance with FHA's minimum property standards. If issues are found, they typically must be resolved before the loan can close.

Rural Housing Loan Limits vs. FHA: What's the Difference?

Homebuyers in less densely populated areas often find themselves comparing rural housing loan limits vs. FHA options. The USDA Rural Development loan program is the primary alternative for buyers in eligible rural and suburban areas, and it comes with its own structure that differs meaningfully from FHA financing.

Here's a quick comparison of the two programs:

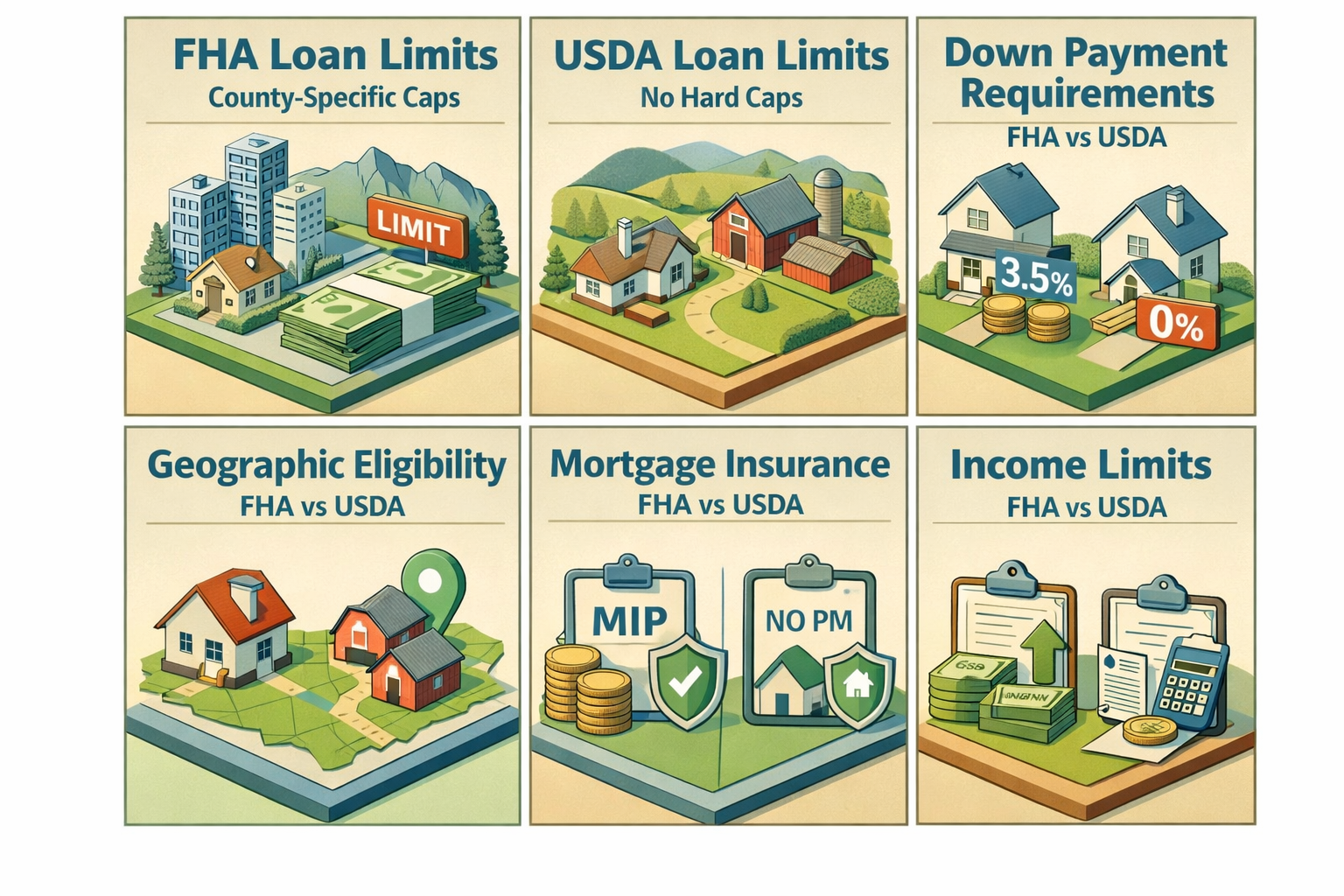

- Down payment: USDA loans may offer 100% financing with no down payment for eligible borrowers. FHA loans require at least 3.5% down for borrowers with qualifying credit scores.

- Loan limits: USDA loans don't set hard loan limits in the traditional sense. Instead, approval is based on the borrower's ability to repay relative to local income limits and property eligibility. FHA, by contrast, imposes a specific dollar cap by county.

- Geographic eligibility: USDA loans are restricted to properties in USDA-designated rural and some suburban areas. FHA loans can be used anywhere in the country, regardless of location.

- Mortgage insurance: Both programs require mortgage insurance, though the structure and cost differ. USDA charges a guarantee fee, while FHA uses upfront and annual MIP.

- Income limits: USDA imposes household income caps to ensure the program serves moderate-income borrowers. FHA does not have income limits.

For buyers in rural areas, USDA loans can sometimes offer more favorable terms — particularly the no-down-payment benefit. However, if the property you want isn't in a USDA-eligible zone, or if your income exceeds USDA thresholds, FHA may be the better path. Consulting with a knowledgeable lender can help you determine which program aligns best with your situation.

Strategies for Staying Within FHA Loan Limits When Buying a Resale Home

If you've found an existing home you love but the purchase price is close to — or above — your county's FHA limit, you have a few options worth considering.

Make a larger down payment. The FHA loan limit applies to the loan amount, not the purchase price. If a home is priced slightly above the limit, you could make up the difference with a larger down payment. This keeps the financed amount within the allowable cap while still letting you purchase the home you want.

Negotiate the purchase price. In some markets, sellers may be open to negotiating. If the listing price exceeds the FHA limit by a small margin, bringing the seller down could make the deal work within FHA financing terms.

Explore a different county or neighborhood. If you have flexibility in where you buy, checking FHA limits in adjacent counties might reveal a higher cap — or a more affordable area where the same budget goes further.

Consider an FHA 203(k) loan for value-add properties. If you're buying a fixer-upper, this rehab loan may allow you to finance both the purchase price and renovation costs under a single loan, potentially getting more value from the existing FHA limit in your area.

Look at conventional alternatives. If your credit score is strong and you can manage a slightly higher down payment, a conventional loan might allow you to finance a higher purchase price without the FHA cap constraints.

●Conclusion

Understanding FHA loan limits for existing homes is a foundational step for any homebuyer considering government-backed financing. From county-level caps and property condition requirements to how FHA compares with USDA rural housing programs, there's a lot to navigate — but the knowledge puts you in a much stronger position at the negotiating table and with your lender.

Whether you're a first-time buyer looking at resale properties, a homeowner researching refinance options, or simply trying to understand your financing choices, FHA loans remain one of the most flexible and widely available mortgage programs in the country. The key is knowing how the limits work in your specific area and ensuring the home you choose meets FHA's eligibility standards.

Ready to take the next step? Connect with an FHA-approved lender at LoanWise to explore your options, get a loan limit check for your target county, and find out how much home you may qualify for today.