Smart Investment Property Refinancing Strategies

Refinancing for investment property has become a cornerstone strategy for savvy real estate investors looking to optimize their portfolios. With current market conditions presenting unique opportunities, investors can leverage refinancing to unlock equity, improve cash flow, and position their properties for long-term success. Whether you're managing a single rental property or an extensive portfolio, understanding the nuances of investment property refinancing could significantly impact your returns and growth potential.

Key Benefits of Refinancing Rental Property

Refinancing rental property offers several compelling advantages that can transform your investment strategy and financial position. These benefits extend beyond simple rate reductions and can fundamentally reshape your portfolio's performance.

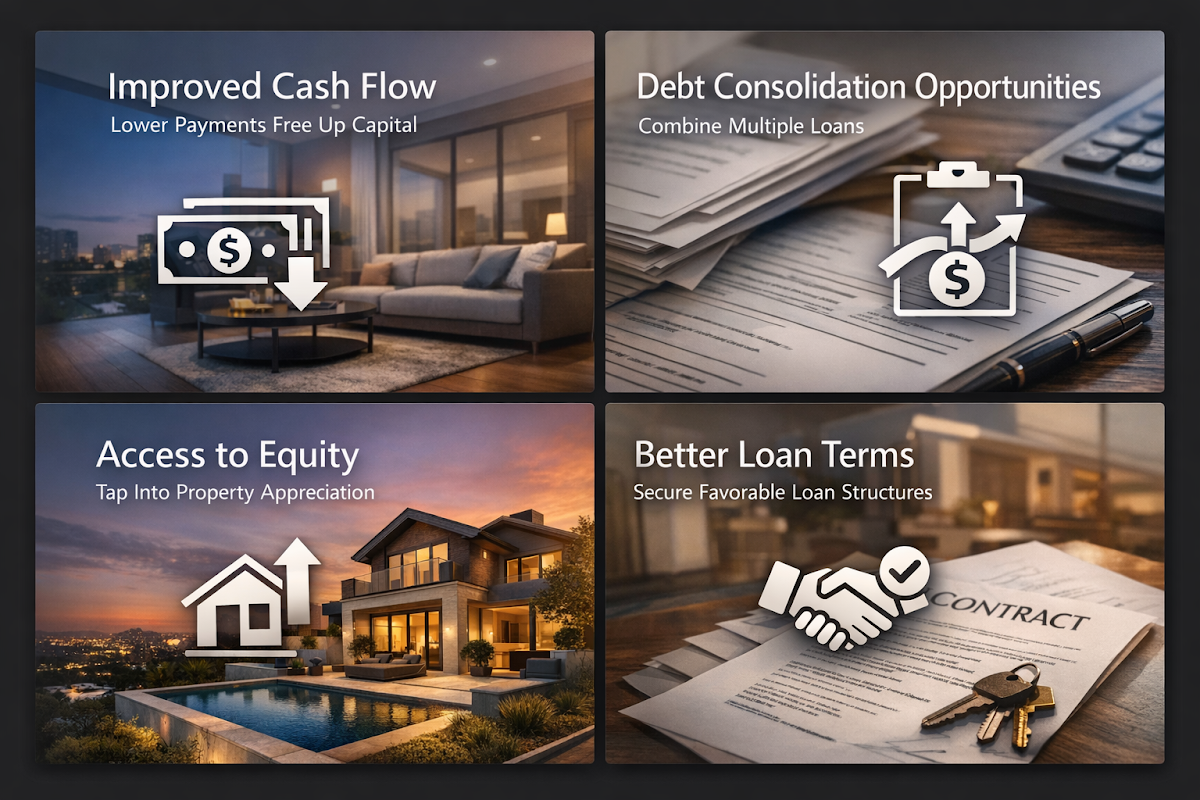

- Improved Cash Flow: Lower interest rates typically translate to reduced monthly payments, freeing up capital for additional investments or property improvements that enhance rental income potential.

- Debt Consolidation Opportunities: Refinancing allows investors to consolidate multiple property loans or high-interest debts into a single, more manageable payment structure with potentially better terms.

- Access to Equity: Cash-out refinancing enables investors to tap into accumulated property appreciation, providing funds for down payments on additional properties or major renovations.

- Better Loan Terms: Market conditions may offer opportunities to secure more favorable loan structures, including longer amortization periods or removal of prepayment penalties that previously limited flexibility.

Cash-Out Refinance Investment Property Guidelines

Cash-out refinance investment property transactions follow specific guidelines that investors must understand to maximize their refinancing potential. Current lending standards typically allow investors to access significant portions of their property equity while maintaining adequate security for lenders.

- Loan-to-Value Limits: Most lenders extend loans up to 75% of the appraised property value, allowing investors to access substantial equity while maintaining a 25% cushion that satisfies risk requirements.

- Reserve Requirements: Lenders often require cash reserves equivalent to 6-12 months of mortgage payments, ensuring investors maintain adequate liquidity post-refinance for property management and unexpected expenses.

- Equity Minimums: Investors typically need at least 25-30% equity in their property before refinancing, providing the foundation for both cash-out opportunities and favorable loan terms.

- Income Verification: Rental income documentation and debt service coverage ratios become critical factors in qualifying for investment property refinancing, with lenders evaluating the property's ability to support the new loan structure.

Investment Property Refinance Rates Considerations

Investment property refinance rates differ significantly from primary residence mortgages, and understanding these distinctions helps investors make informed timing decisions. Rate environments and market conditions can create windows of opportunity for strategic refinancing.

- Rate Premiums: Investment properties typically carry interest rates that are 0.125% to 0.75% higher than primary residence loans, reflecting the increased risk lenders associate with rental properties.

- Market Timing: The anticipated low-rate environment through 2026 may provide exceptional opportunities for investors to refinance existing high-rate loans and optimize their portfolio's cost structure.

- Rate Lock Strategies: Investors should consider rate lock options when market conditions are favorable, as investment property rates can fluctuate more dramatically than residential mortgage rates.

- DSCR Impact: Properties with strong debt service coverage ratios may qualify for more competitive rates, making property performance optimization a key factor in refinancing success.

Financial Preparation Strategies Before Refinancing

Successful investment property refinancing requires thorough financial preparation and strategic positioning. Investors who prepare comprehensively often secure better terms and smoother transaction processes.

- Credit Profile Optimization: Maintaining strong personal and business credit scores becomes crucial, as investment property loans often require higher credit thresholds than primary residence mortgages.

- Documentation Organization: Assembling rental income records, tax returns, and property expense documentation streamlines the underwriting process and demonstrates professional property management practices.

- Property Condition Assessment: Ensuring properties are well-maintained and addressing deferred maintenance issues can positively impact appraisal values and loan approval odds.

- Cash Flow Analysis: Conducting thorough cash flow projections with new loan terms helps investors evaluate whether refinancing aligns with their investment objectives and risk tolerance.

Step-by-Step Investment Property Refinancing Process

The investment property refinancing process involves several distinct phases that require careful coordination and timing. Following a systematic approach can help investors navigate potential challenges and optimize their outcomes.

- Market Research and Lender Comparison: Begin by researching current market rates and comparing offers from multiple lenders, as investment property loan terms can vary significantly between institutions. Focus on lenders who specialize in investor financing and understand rental property investments cash flow dynamics.

- Financial Documentation and Application: Compile comprehensive financial documentation including rental agreements, property tax records, insurance policies, and personal financial statements. Submit applications to pre-selected lenders to begin the underwriting process and lock favorable rates when available.

- Property Appraisal and Final Approval: Coordinate property appraisals and work with lenders through the final underwriting phase. Be prepared to address any conditions or requirements that emerge during this stage, and maintain flexibility to adjust loan terms if market conditions change.

Optimizing Refinancing Timing and Market Conditions

Timing plays a crucial role in investment property refinancing success, and astute investors monitor multiple market indicators to identify optimal refinancing windows. Understanding these timing considerations can significantly impact the financial benefits of refinancing.

- Interest Rate Environment Analysis: Monitor Federal Reserve policies and economic indicators that influence mortgage rates. The expected low-rate environment through 2026 may create sustained opportunities for investors to refinance high-rate existing loans and improve cash flow metrics.

- Property Value Appreciation Timing: Consider refinancing when local market conditions have driven property values higher, as increased equity positions provide better loan-to-value ratios and access to larger cash-out amounts for portfolio expansion or improvements.

- Portfolio Performance Evaluation: Assess overall portfolio performance and cash flow needs to determine whether refinancing individual properties or multiple properties simultaneously aligns with broader investment strategies and liquidity requirements.

●Conclusion

Refinancing for investment property represents a powerful tool for real estate investors seeking to optimize their portfolios and enhance returns. With current market conditions potentially offering favorable opportunities through 2026, investors who understand the guidelines, prepare thoroughly, and time their refinancing strategically may realize significant benefits. Whether pursuing cash-out refinancing to fund additional acquisitions or simply seeking better loan terms to improve cash flow, the key lies in comprehensive preparation and working with lenders who understand the unique aspects of investment property financing. Success in investment property refinancing often comes down to having adequate equity, maintaining strong financials, and partnering with experienced mortgage professionals who can navigate the complexities of investor-focused loan products.