SBA Loan Application Guide for Real Estate Investors

While real estate investors typically focus on DSCR loans and bridge financing, understanding the SBA loan application process can open additional funding opportunities for investment ventures. The Small Business Administration offers various loan programs that might complement your investment strategy, particularly when expanding your real estate business operations or acquiring commercial properties.

Navigating the SBA loan application timeline requires careful preparation and attention to detail. Unlike traditional investment property loans, SBA financing involves more extensive documentation and longer processing periods. However, the potential benefits may justify the additional effort for certain investment scenarios.

Essential SBA Loan Application Requirements

Understanding the essential SBA loan application requirements helps real estate investors determine if this financing option aligns with their investment goals. The application process typically involves more comprehensive documentation than conventional investment loans.

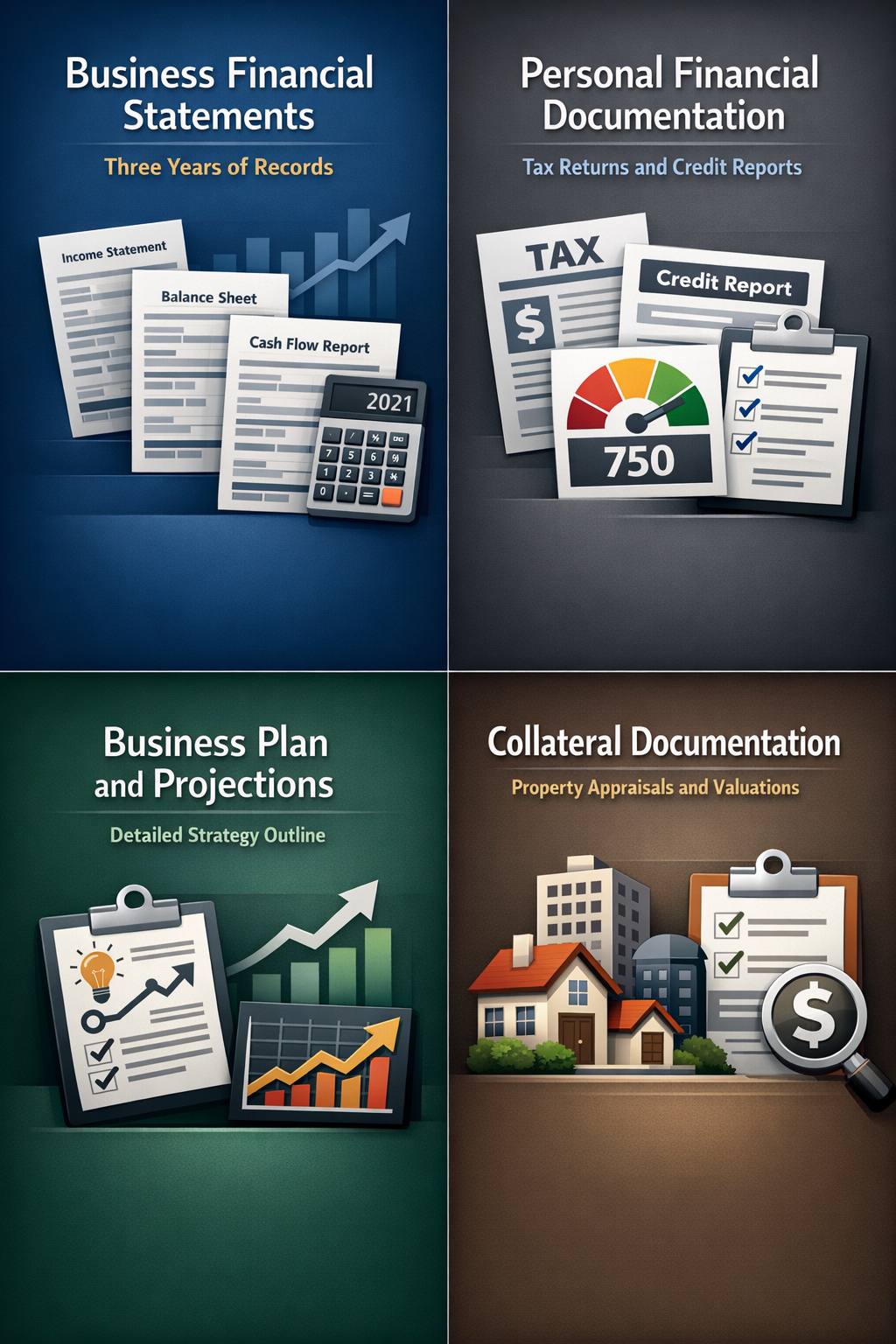

- Business financial statements: Three years of tax returns, profit and loss statements, and balance sheets for your real estate investment business

- Personal financial documentation: Personal tax returns, credit reports, and net worth statements for all owners with 20% or greater stake

- Business plan and projections: Detailed business plan outlining your real estate investment strategy and financial projections for the next two years

- Collateral documentation: Property appraisals, lease agreements, and other asset valuations that may secure the loan

SBA Loan Documentation Checklist for Property Investors

The SBA loan documentation checklist for real estate investors extends beyond typical mortgage paperwork. Proper preparation of these documents can significantly impact your application timeline and approval odds.

- Corporate documents: Articles of incorporation, operating agreements, business licenses, and any franchise agreements if applicable to your investment business

- Property-specific documentation: Purchase agreements, property management contracts, tenant lease agreements, and rental income verification

- Banking records: Three months of business and personal bank statements, plus reconciliation reports for all accounts

- Insurance documentation: Current insurance policies for existing properties and proposed coverage for new acquisitions

Understanding the SBA Loan Application Process Timeline

The SBA loan application process timeline typically extends longer than conventional investment property financing. Real estate investors should plan accordingly when incorporating SBA loans into their acquisition strategies.

- Initial application review: Lenders typically take 30-45 days to review your complete application package and request additional documentation

- SBA approval process: Once submitted to the SBA, the approval process may take an additional 60-90 days depending on loan size and complexity

- Closing preparation: Final underwriting and closing preparations usually require 15-30 days after SBA approval is received

- Total timeline expectation: Most SBA loan applications take 3-6 months from submission to funding, significantly longer than bridge loans or DSCR financing

Common SBA Loan Application Mistakes Real Estate Investors Make

Real estate investors often encounter specific challenges when completing their SBA loan application. Understanding these common pitfalls can help streamline your application process and improve approval chances.

- Incomplete financial documentation: Failing to provide comprehensive business financial records or mixing personal and business expenses without clear separation

- Inadequate business justification: Not clearly demonstrating how the SBA loan fits into your overall real estate investment business strategy and growth plans

- Property use restrictions: Misunderstanding SBA guidelines regarding investment property purchases versus owner-occupied commercial real estate requirements

- Timeline mismanagement: Underestimating the application timeline and creating pressure on deal closings or missing investment opportunities

Alternative Financing Options for Real Estate Investors

While SBA loans might serve specific business expansion needs, real estate investors often find more suitable financing through specialized investment property loans. These alternative financing options typically offer faster processing and more flexible terms for property acquisitions.

- DSCR loans: Debt Service Coverage Ratio loans focus on property cash flow rather than personal income, making them ideal for seasoned investors

- Fix and flip financing: Short-term loans designed specifically for property renovation projects with quick turnaround expectations

- Bridge loans: Temporary financing solutions that allow investors to acquire properties quickly while arranging permanent financing

- Portfolio lender programs: Specialized lenders who keep loans in-house and offer more flexible underwriting for investment properties

●Conclusion

The SBA loan application process requires significant time and documentation preparation, which may not align with the fast-paced nature of most real estate investment opportunities. While SBA financing might serve specific business expansion needs, investors typically find better success with specialized investment property loans.

DSCR loans, bridge financing, and fix and flip loans often provide more appropriate terms and faster processing for real estate investment activities. These alternatives focus on property performance and investment potential rather than traditional small business criteria, making them more suitable for most real estate investment scenarios.

Before committing to the lengthy SBA loan application timeline, consider consulting with investment property financing specialists who understand the unique needs of real estate investors and can recommend the most efficient funding solutions for your investment strategy.