Buying a home when your credit score isn't perfect can feel like an uphill battle. Many first-time homebuyers and those who've faced financial setbacks worry that a low credit score puts homeownership out of reach. The good news is that it doesn't have to. The Federal Housing Administration (FHA) offers a mortgage program specifically designed to help borrowers with less-than-perfect credit get into a home. Understanding the requirements for FHA loan with low credit score is the first step toward making that goal a reality. In this guide, we'll walk you through everything you need to know — from minimum credit thresholds to down payment rules and debt-to-income guidelines — so you can approach the process with confidence.

What Makes FHA Loans Different from Conventional Mortgages

FHA loans are backed by the federal government through the Federal Housing Administration, which means lenders take on less risk when they approve borrowers with lower credit scores or smaller down payments. This government guarantee is what allows FHA-approved lenders to offer more flexible qualification standards compared to conventional loan programs.

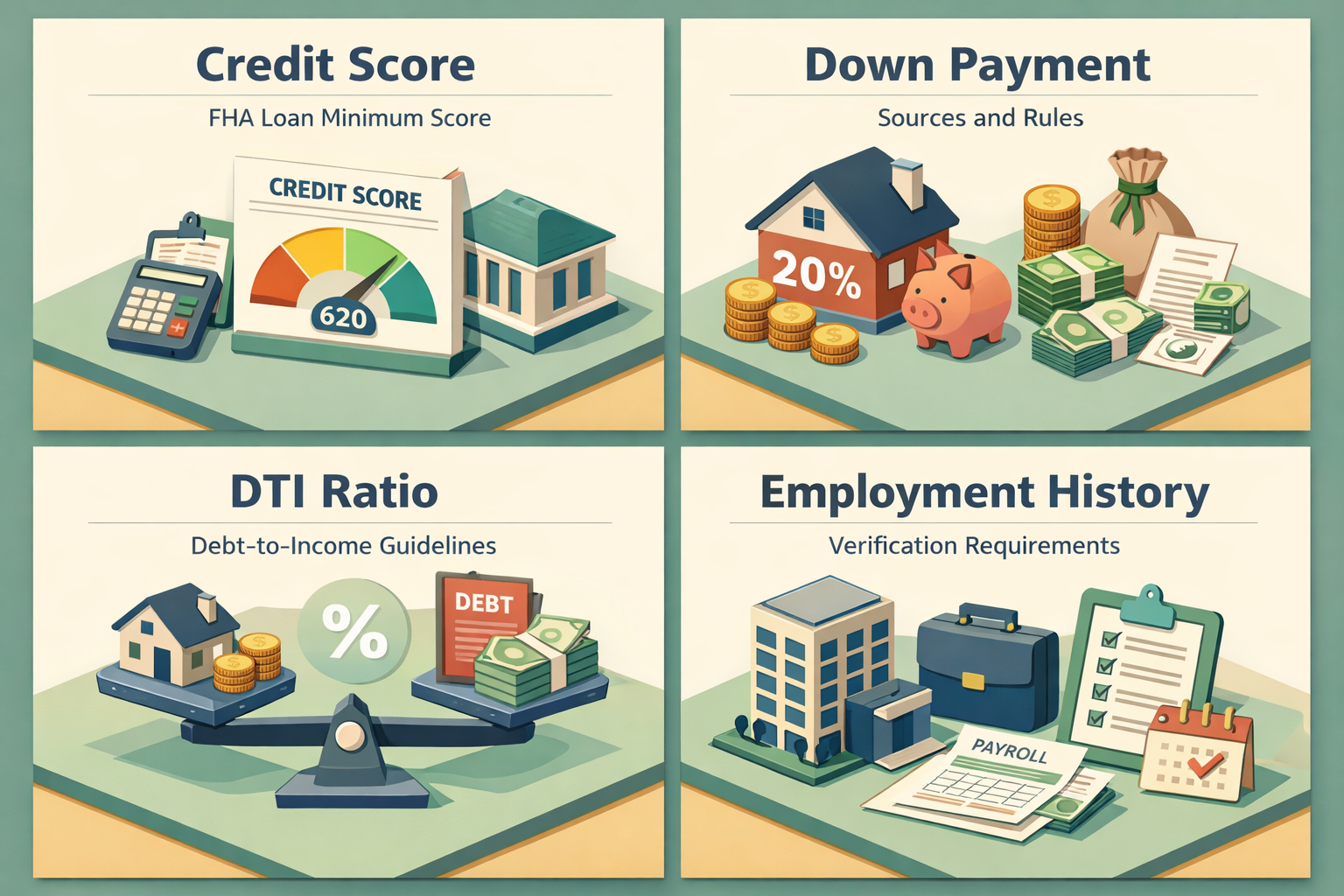

With a conventional mortgage, lenders typically require a credit score of at least 620, and borrowers with scores below 700 may face higher interest rates or stricter terms. FHA loans, by contrast, set a lower FHA loan minimum credit score threshold, making them a more accessible path for buyers who are still rebuilding their financial profile.

Another key difference is the mortgage insurance structure. FHA loans require both an upfront mortgage insurance premium (MIP) and an annual MIP paid monthly, regardless of your down payment amount. Conventional loans only require private mortgage insurance (PMI) when the down payment is below 20%, and PMI can be removed once you build enough equity. It's worth factoring these costs into your overall budget when comparing loan options.

Understanding the FHA Loan Minimum Credit Score Requirements

The FHA program sets official credit score guidelines that determine both your eligibility and the down payment you'll need to bring to the table. Here's how the thresholds generally break down:

- 580 or higher: Borrowers getting an FHA loan with a 580 credit score are typically eligible for the program's lowest down payment option of 3.5% of the purchase price.

- 500 to 579: Borrowers in this range may still qualify for an FHA loan, but the FHA requires a minimum down payment of 10% to offset the added risk.

- Below 500: The FHA does not insure loans for borrowers with scores under 500, meaning most lenders will not approve an application at this level.

It's important to note that these are the FHA's official guidelines, but individual lenders are permitted to set their own overlay requirements — meaning a lender might require a 620 minimum score even though the FHA allows 580. Shopping around with multiple FHA-approved lenders is often a smart move when qualifying for FHA with bad credit, since different institutions apply different standards.

The Full Checklist: Requirements for FHA Loan with Low Credit Score

Credit score is just one piece of the puzzle. Meeting the requirements for FHA loan with low credit score means satisfying several additional criteria that lenders and the FHA will review during the underwriting process. Here's a closer look at what's typically expected:

Debt-to-Income Ratio (DTI)

Your debt-to-income ratio measures how much of your gross monthly income goes toward debt payments. FHA guidelines generally allow a front-end DTI (housing costs only) of up to 31% and a back-end DTI (all monthly debts) of up to 43%. However, lenders may approve borrowers with higher DTI ratios if there are strong compensating factors, such as significant cash reserves or a long history of on-time payments.

Employment and Income Verification

Lenders want to see a stable employment history, typically covering at least two years. You'll need to provide recent pay stubs, W-2 forms, and possibly tax returns. Self-employed borrowers may need to supply two years of tax returns and profit-and-loss statements to verify consistent income.

Property Eligibility

The home you're purchasing must meet FHA minimum property standards and be appraised by an FHA-approved appraiser. The property must be your primary residence — FHA loans are not available for investment properties or vacation homes.

FHA Loan Limits

FHA loan limits vary by county and are updated annually. Your loan amount cannot exceed the limit set for the area where you're buying. In higher-cost markets, these limits are significantly higher than in more affordable regions, so it's worth checking the current limits for your target location.

Down Payment Sources and Gift Fund Rules

One of the most borrower-friendly aspects of FHA financing is the flexibility around where your down payment money can come from. Unlike some loan programs that require funds to come exclusively from your own savings, FHA guidelines allow down payment gifts from:

- Family members

- Close friends with a clearly defined relationship

- Employers or labor unions

- Charitable organizations

- Government agencies offering down payment assistance programs

If you're receiving a gift, the donor will typically need to provide a signed gift letter confirming the funds are a gift and not a loan that must be repaid. Your lender will also likely require documentation showing the transfer of funds from the donor's account to yours.

For borrowers getting an FHA loan with a 580 credit score, combining the 3.5% minimum down payment with a down payment assistance program can significantly reduce the upfront cash needed. Many state and local housing finance agencies offer grants or second mortgage programs designed to help buyers cover this cost, so it's worth researching what's available in your area.

How Lenders Evaluate FHA Loan Approval with Low Score

When a borrower applies for FHA loan approval with a low score, lenders look beyond the credit number itself. They're trying to understand the full picture of your financial behavior and stability. Here are some of the factors that can work in your favor:

Recent Payment History

Lenders pay close attention to your most recent 12 to 24 months of payment history. If your credit score is low due to older issues — such as a medical debt or a financial hardship several years ago — but you've consistently paid on time recently, that positive trend may strengthen your application.

Credit Explanations and Documentation

If negative items appear on your credit report, providing a written explanation can help. For example, if a period of late payments was caused by a job loss, medical emergency, or other documented hardship, many underwriters will consider the context when making their decision.

Cash Reserves

Having additional savings beyond your down payment and closing costs signals to lenders that you have a financial cushion. Even one to three months of mortgage payments held in reserve can serve as a compensating factor that may improve your chances of FHA loan approval with a low score.

Lower Loan-to-Value Ratio

If you're able to put down more than the minimum required — say 10% instead of 3.5% — you reduce the lender's risk and may improve your overall application profile, even with a lower credit score.

Practical Steps to Improve Your Chances Before Applying

If your credit score is currently below the 580 threshold — or if you want to put your best foot forward before submitting an application — there are practical strategies that may help you qualify more comfortably.

- Check your credit reports: Request free copies of your credit reports from all three bureaus and review them carefully for errors. Disputing inaccurate negative items could raise your score meaningfully.

- Pay down revolving balances: Reducing your credit card balances relative to your credit limits can improve your credit utilization ratio, which is one of the most influential factors in your score.

- Avoid new credit applications: Each hard inquiry can temporarily lower your score. Try to avoid applying for new credit cards or loans in the months leading up to your mortgage application.

- Bring delinquent accounts current: If you have past-due accounts, bringing them current and maintaining on-time payments going forward may help over time.

- Work with a HUD-approved housing counselor: Free or low-cost counseling is available through HUD-approved agencies. A counselor can help you develop a personalized plan for improving your credit and preparing for homeownership.

Even small improvements in your credit score can make a difference. Moving from a 575 to a 580, for instance, could open the door to the lower 3.5% down payment option and potentially better loan terms.

●Conclusion

Navigating the path to homeownership with a low credit score is challenging, but it's far from impossible. The FHA program exists precisely to give buyers in this situation a realistic shot at owning a home. By understanding the requirements for FHA loan with low credit score — including the 580 credit score threshold for the 3.5% down payment option, debt-to-income guidelines, stable income requirements, and property standards — you can take targeted steps to strengthen your application. Whether you're ready to apply now or working toward improving your credit over the next several months, the important thing is to start informed. At LoanWise, we're here to help you explore your options and connect with lenders who can work with your unique financial situation. Reach out today to take the first step toward your new home.