If you've built up equity in your home, you may be sitting on a powerful financial resource. A home equity line of credit, commonly known as a HELOC, lets homeowners borrow against that equity in a flexible, revolving way — much like a credit card secured by your property. But before you can access those funds, you'll need to meet specific lender criteria. Understanding the requirements for a HELOC on primary residence is the first step toward making a smart, informed borrowing decision. Whether you're planning a major renovation, consolidating debt, or preparing for unexpected expenses, this guide breaks down everything you need to know.

What Is a HELOC and How Does It Work for Primary Residences?

A HELOC is a secured line of credit that uses your home as collateral. Unlike a traditional loan where you receive a lump sum upfront, a HELOC gives you access to a credit limit you can draw from as needed during a set draw period — typically around 10 years. After that, you enter a repayment period where you pay back both principal and interest.

Because your primary residence serves as collateral, lenders view HELOCs on owner-occupied homes as relatively lower risk compared to investment properties or second homes. This often means more favorable interest rates and higher borrowing limits for primary residence applicants. However, it also means that failing to repay could put your home at risk — so it's essential to borrow responsibly.

HELOCs are particularly popular among homeowners who want financial flexibility. You only pay interest on the amount you actually draw, not the full credit line. This makes them a cost-effective option for ongoing projects or expenses that don't have a fixed price tag upfront.

Core Equity and Loan-to-Value Standards You Must Understand

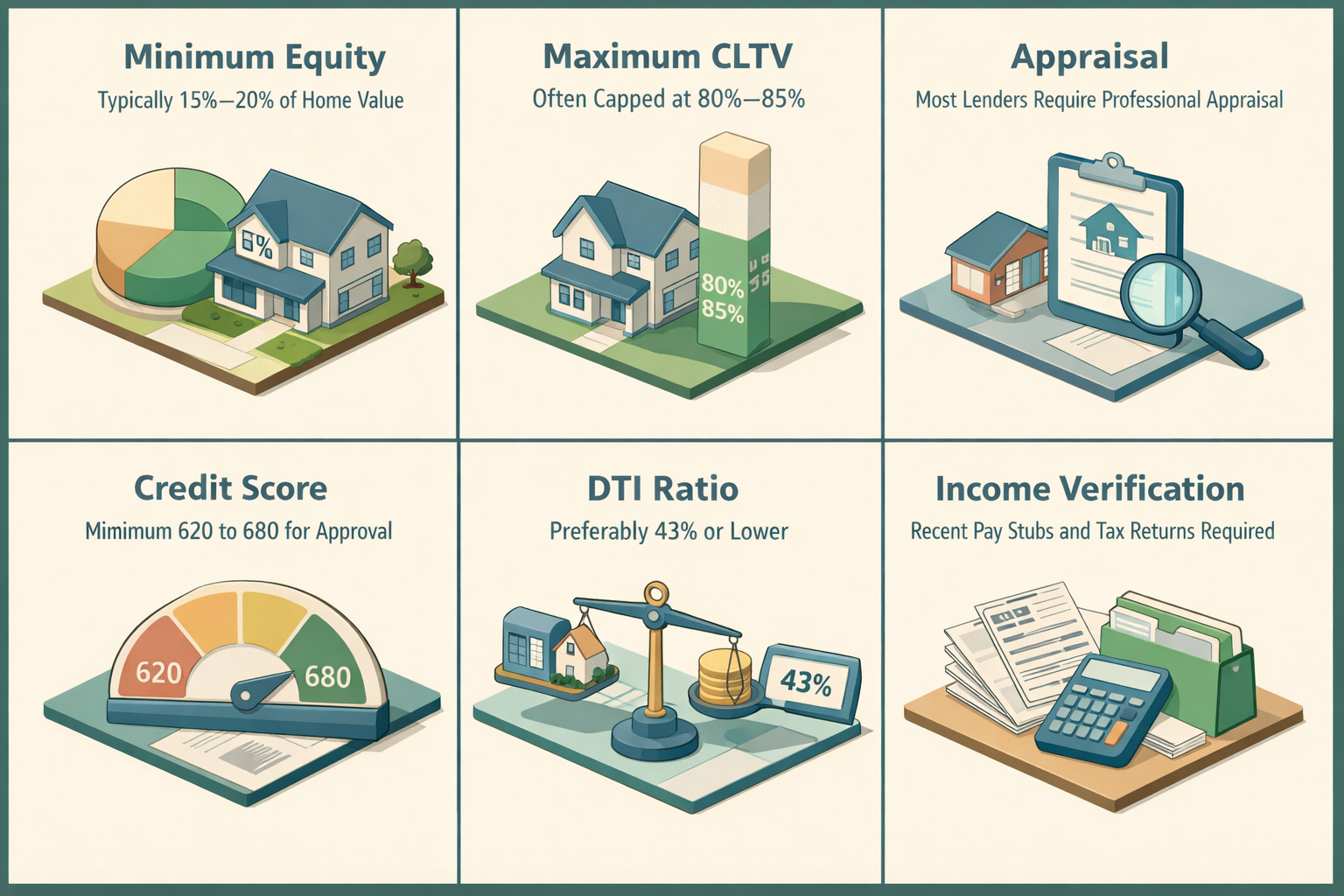

One of the most fundamental home equity line of credit requirements is having sufficient equity in your property. Equity is the difference between your home's current market value and what you still owe on your mortgage. Most lenders typically require that you maintain at least 15% to 20% equity in your home after the HELOC is factored in.

Lenders measure this using a metric called the combined loan-to-value ratio (CLTV). This calculation adds your existing mortgage balance to the HELOC amount you're requesting, then divides the total by your home's appraised value. Most lenders cap the CLTV at around 80% to 85%, though some may allow slightly higher ratios depending on your overall financial profile.

For example, if your home is appraised at $400,000 and you owe $250,000 on your mortgage, you have $150,000 in equity. With an 85% CLTV cap, your total borrowing limit across both loans could be up to $340,000 — meaning you might qualify for a HELOC of up to $90,000. Keep in mind that your actual credit limit may vary based on other qualifying factors.

- Minimum equity required: Typically 15%–20% of home value

- Maximum CLTV: Often capped at 80%–85%

- Appraisal: Most lenders will require a professional home appraisal to confirm current value

Credit Score for HELOC Approval: What Lenders Are Looking For

Your credit score for a HELOC plays a significant role in whether you qualify and what interest rate you'll receive. Most lenders typically look for a minimum credit score in the range of 620 to 680, though borrowers with scores of 700 or higher may access better rates and more generous terms.

A strong credit history signals to lenders that you're a reliable borrower. They'll review not just your score, but also your overall credit report — including payment history, outstanding balances, length of credit history, and any derogatory marks such as late payments, collections, or bankruptcies. Even if your score meets the minimum threshold, negative items on your report could result in a higher interest rate or a reduced credit line.

If your credit score for HELOC is on the lower end, it may be worth spending a few months improving it before applying. Paying down revolving balances, avoiding new hard inquiries, and resolving any errors on your credit report can all contribute to a meaningful score increase over time.

Income Verification and Debt-to-Income Ratio Requirements

Lenders want to be confident that you can repay what you borrow. That's why income verification is a standard part of the HELOC application process. You'll generally need to provide recent pay stubs, W-2 forms, and possibly federal tax returns — especially if you're self-employed or have variable income sources.

Alongside your income, lenders calculate your debt-to-income ratio (DTI). This compares your total monthly debt obligations — including your existing mortgage, car payments, student loans, credit cards, and the projected HELOC payment — to your gross monthly income. Most lenders prefer a DTI of 43% or lower, though some may accept slightly higher ratios for borrowers with strong compensating factors like excellent credit or substantial home equity.

Self-employed homeowners and those with non-traditional income may face additional documentation requirements. Bank statements, profit-and-loss statements, and 1099 forms might all be requested to verify consistent earning capacity. Being organized and prepared with these documents can help streamline the approval process significantly.

How the Requirements for a HELOC on Primary Residence Differ from Other Properties

It's worth noting that the requirements for a HELOC on primary residence are generally more flexible and borrower-friendly than those applied to investment properties or vacation homes. Lenders tend to offer lower interest rates, higher CLTV allowances, and less restrictive credit thresholds for owner-occupied homes — because borrowers are statistically more motivated to protect the home they live in.

For investment properties, lenders often require a lower CLTV, a higher credit score, and may charge a risk premium on the interest rate. Some lenders don't offer HELOCs on non-owner-occupied properties at all. If you own rental properties and are hoping to tap into their equity, your options may be more limited or more costly than a primary residence HELOC.

This distinction makes primary residence HELOCs one of the most accessible and cost-effective equity-based financing tools available to homeowners. If you qualify, it's often a smarter starting point than exploring equity options on secondary properties.

Using HELOC Funds for Home Improvements and Other Smart Purposes

One of the most popular reasons homeowners pursue a HELOC is for renovations. Using a HELOC for home improvements can be financially strategic — not only does it fund the upgrades, but certain renovations may increase your home's value, potentially building even more equity over time. Kitchen remodels, bathroom upgrades, roof replacements, and energy-efficient improvements are all common uses.

Beyond renovations, HELOCs can be used for a variety of purposes, including:

- Debt consolidation: Paying off high-interest credit card balances with a lower-rate HELOC

- Education expenses: Funding tuition or training costs for yourself or a family member

- Emergency fund backup: Keeping a HELOC open as a financial safety net for unexpected expenses

- Major purchases: Financing large, planned expenses like medical costs or a vehicle

It's important to use HELOC funds thoughtfully. Because your home is on the line, borrowing for depreciating assets or discretionary spending carries real financial risk. The best HELOC strategies typically involve uses that either improve your financial position or preserve your home's value.

HELOC vs Home Equity Loan: Choosing the Right Fit for Your Needs

When comparing a HELOC vs home equity loan, the key difference comes down to how funds are accessed and repaid. A home equity loan delivers a lump sum at a fixed interest rate with predictable monthly payments — ideal for borrowers who know exactly how much they need. A HELOC, by contrast, functions as a revolving credit line with a variable interest rate, offering flexibility for ongoing or uncertain expenses.

Here's a quick comparison to help you decide:

- HELOC: Variable rate, draw as needed, interest-only payments during draw period, flexible for ongoing projects

- Home Equity Loan: Fixed rate, lump sum disbursement, predictable payments, better for one-time large expenses

If you're tackling a multi-phase home renovation or want a financial safety net, a HELOC may offer more versatility. If you're funding a single major expense and want payment certainty, a home equity loan might be the better choice. In some cases, homeowners may even consider both products depending on their specific financial goals.

Both options typically share similar qualifying criteria — equity thresholds, credit score minimums, and income verification — so understanding one helps you evaluate the other with confidence.

●Conclusion

Tapping into your home's equity can be one of the most practical financial moves a homeowner makes — provided you go in well-prepared. Understanding the requirements for a HELOC on primary residence puts you in a much stronger position to shop for competitive terms, present a solid application, and use the funds in a way that genuinely improves your financial life. From maintaining adequate equity and a healthy credit score to keeping your debt load manageable, each qualification factor is within your control with the right planning. If you're ready to explore your options, consider connecting with a knowledgeable mortgage professional who can help you evaluate whether a HELOC aligns with your current goals and long-term financial strategy.