When shopping for a home loan, you'll likely come across two broad categories: conforming and non-conforming mortgages. Most borrowers are familiar with conforming loans — those that meet the guidelines set by Fannie Mae and Freddie Mac. But a non-conforming mortgage follows a different set of rules, and for many homebuyers, it could actually be the better fit. Whether you're purchasing a high-value property, carrying a unique financial profile, or simply don't check every traditional lending box, understanding non-conforming loans is well worth your time. This guide breaks down exactly what these loans are, how they differ from conforming products, who they serve, and what to consider before applying.

Understanding the Conforming Loan Baseline

To understand what makes a mortgage "non-conforming," it helps to first understand the standard it's measured against. Conforming loans are home loans that meet the purchasing guidelines established by Fannie Mae and Freddie Mac, two government-sponsored enterprises (GSEs) that play a central role in the U.S. secondary mortgage market. These guidelines include limits on loan size, borrower credit scores, debt-to-income ratios, and documentation requirements.

Each year, the Federal Housing Finance Agency (FHFA) sets a baseline conforming loan limit that determines the maximum loan amount a conforming mortgage can carry. In most parts of the country, this limit applies uniformly, though higher-cost areas may receive elevated limits. When a loan exceeds this threshold — or fails to meet other GSE criteria — it becomes a non-conforming mortgage.

Lenders who issue conforming loans can sell them to Fannie Mae or Freddie Mac, which provides liquidity and reduces lender risk. Non-conforming loans, by contrast, are typically held in the lender's own portfolio or sold to private investors. This distinction has real implications for interest rates, qualification standards, and the overall borrowing experience.

What Makes a Mortgage Non-Conforming

A mortgage can fall outside conforming guidelines for several reasons. The most common is loan size. Jumbo loans — mortgages that exceed the FHFA's annual conforming loan limit — are perhaps the most widely recognized type of non-conforming mortgage. These loans are frequently used by buyers in competitive, high-cost real estate markets where home prices regularly surpass the conforming cap.

Beyond loan size, a mortgage may be considered non-conforming for reasons that include:

- Credit profile: Borrowers with lower credit scores or past credit events such as bankruptcy or foreclosure may not meet GSE requirements, pushing them toward non-conforming products.

- Debt-to-income ratio: If a borrower's monthly debt obligations are relatively high compared to their income, they may exceed conforming DTI thresholds.

- Non-traditional income documentation: Self-employed borrowers, freelancers, and investors who can't provide standard W-2s or tax returns may need alternative documentation loans — a common non-conforming category sometimes called Non-QM (non-qualified mortgage) loans.

- Property type: Certain property types — such as multi-unit investment properties, rural land, or unique structures — may not qualify under conforming guidelines.

- Down payment size: Some non-conforming programs serve borrowers who cannot meet the down payment minimums required for conventional conforming loans.

It's important to note that being "non-conforming" doesn't inherently mean a loan is risky or predatory. It simply means the loan operates outside the GSE framework, which opens the door to greater flexibility in underwriting.

Jumbo Loans: The Most Common Non-Conforming Option

When most mortgage professionals refer to a non-conforming mortgage, they're often talking about jumbo loans. These are loans that exceed the conforming limit set by the FHFA — a number that's adjusted annually to reflect changes in average home prices across the U.S. In high-cost counties, a higher limit may apply, but even that elevated cap has a ceiling, and loans above it are jumbo by definition.

Jumbo mortgages are widely used in metropolitan areas where median home prices are well above national averages. Because these loans can't be purchased by Fannie Mae or Freddie Mac, lenders take on more risk and typically compensate by applying stricter qualification standards. Borrowers seeking jumbo financing might encounter requirements such as:

- Higher minimum credit scores — often in the 700s or above

- Lower debt-to-income ratios than conforming standards allow

- Larger cash reserves after closing

- More thorough income and asset documentation

- In some cases, larger down payment requirements

Interest rates on jumbo loans may be slightly higher than conforming rates, though this can vary based on market conditions, the lender's portfolio strategy, and the borrower's overall financial strength. In some market environments, well-qualified jumbo borrowers have actually secured rates that are competitive with — or even lower than — conforming options. Rate comparisons are always worth doing when you're in this loan category.

Non-QM Loans and Alternative Documentation Pathways

Another significant branch of the non-conforming mortgage world is the non-qualified mortgage, or Non-QM loan. These products were designed to serve creditworthy borrowers who simply don't fit into the income documentation framework required by the Consumer Financial Protection Bureau's "Qualified Mortgage" (QM) rule.

Non-QM loans are particularly common among:

- Self-employed individuals who report lower taxable income due to business deductions, making standard tax return documentation less effective at reflecting their true earning power

- Real estate investors who need to qualify based on rental income or asset depletion rather than traditional employment income

- Foreign nationals purchasing U.S. property without a domestic credit history

- Recent retirees with substantial assets but limited monthly income from employment

Common Non-QM documentation alternatives include bank statement loans (using 12 to 24 months of bank deposits as income evidence), asset depletion loans (spreading total liquid assets over a loan term to calculate qualifying income), and debt service coverage ratio (DSCR) loans used by real estate investors to qualify based on a property's rental income rather than personal income.

While Non-QM products offer meaningful flexibility, they do tend to carry higher interest rates than conforming or QM loans, reflecting the added complexity and risk lenders take on. Borrowers considering these options should carefully weigh the cost against the benefit of accessing financing that might otherwise be unavailable to them.

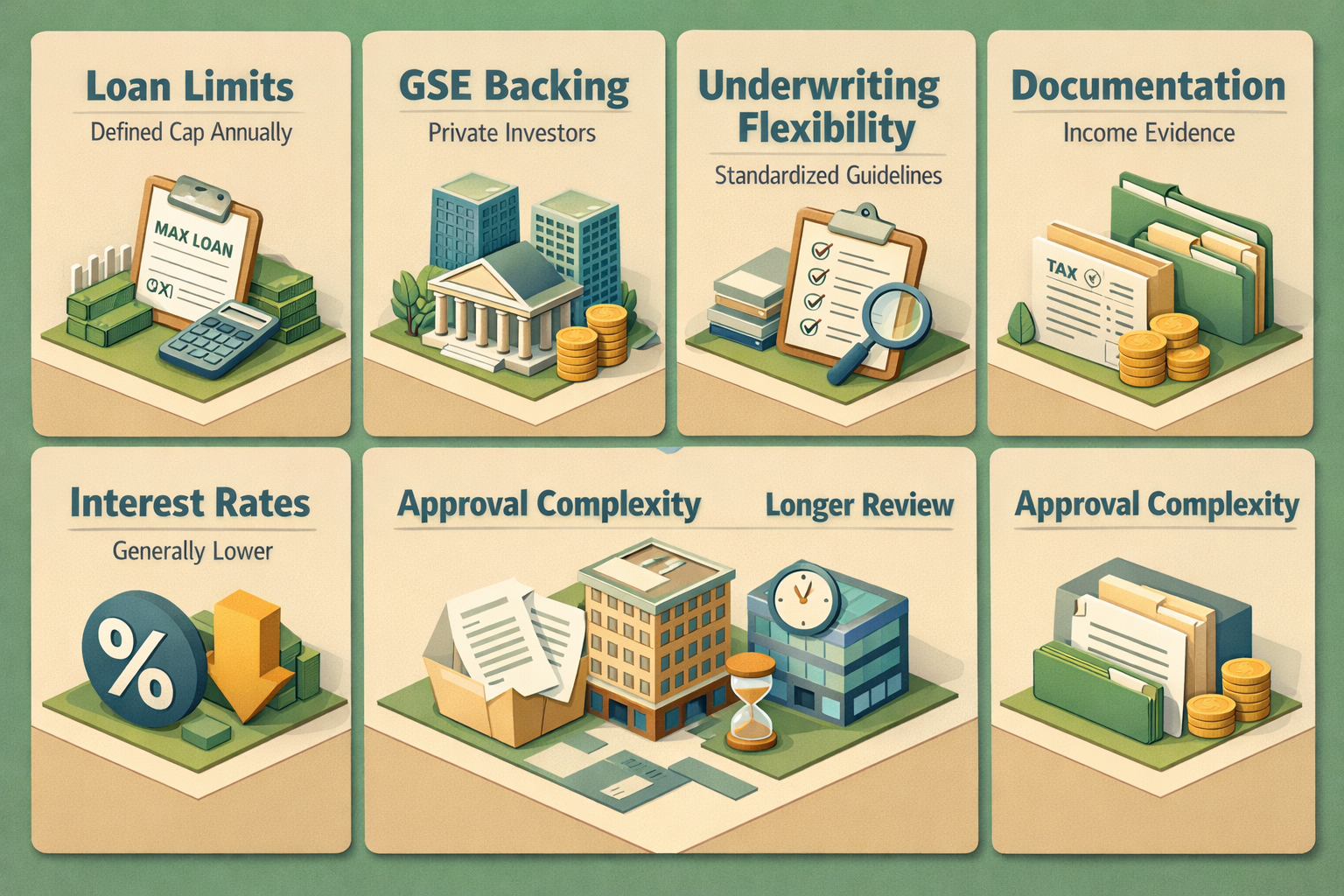

Comparing Non-Conforming and Conforming Loan Features

Understanding the practical differences between conforming and non-conforming mortgages can help you decide which direction fits your situation. Here's a side-by-side look at some key distinctions:

- Loan limits: Conforming loans have a defined cap set annually by the FHFA. Non-conforming loans have no such upper boundary, which is why they serve high-value property purchases effectively.

- GSE backing: Conforming loans can be sold to Fannie Mae or Freddie Mac. Non-conforming loans remain with private investors or the originating lender's portfolio.

- Underwriting flexibility: Conforming loans follow standardized guidelines. Non-conforming lenders can apply more discretion, which may benefit borrowers with unusual financial circumstances.

- Documentation: Conforming loans typically require standard W-2 or tax return income documentation. Non-conforming products may accept bank statements, 1099s, asset statements, or property cash flow analysis.

- Interest rates: Conforming rates are generally lower, but the gap isn't always dramatic, and it shifts with market conditions.

- Approval complexity: Non-conforming approvals may take longer and require more documentation review, particularly for Non-QM products.

Neither loan type is universally better. The right choice depends on your financial profile, the property you're purchasing, and your long-term goals as a homeowner or investor.

Who Should Consider a Non-Conforming Mortgage

A non-conforming mortgage may be worth exploring if you find yourself in one of the following situations:

- You're purchasing a home that exceeds the conforming loan limit in your area and need a jumbo mortgage to cover the purchase price.

- You're self-employed or run your own business and your tax returns don't fully capture your actual earning capacity.

- You're a real estate investor looking to qualify based on a property's rental income rather than your personal salary.

- You're a foreign national buying U.S. property without an established domestic credit file.

- You've had past credit challenges — such as a bankruptcy or late payment history — and don't yet qualify for conforming guidelines but have demonstrated recent financial stability.

- You're recently retired with strong assets but limited verifiable monthly income from employment sources.

In each of these cases, conforming loan programs may simply not be structured to accommodate your circumstances. Non-conforming lenders, however, are often better equipped to evaluate your full financial picture rather than relying solely on standardized metrics. That said, it's wise to work with an experienced mortgage professional who can help you compare all available options and understand the true cost of each path forward.

●Conclusion

A non-conforming mortgage isn't a fallback option — for the right borrower, it can be the most sensible and strategic financing path available. Whether you're navigating the jumbo loan landscape, operating as a self-employed professional, or investing in income-producing real estate, non-conforming products exist precisely because real financial lives don't always fit neatly into standardized boxes. The key is understanding what these loans offer, what they cost, and whether the flexibility they provide is worth the trade-offs involved. If you're exploring your mortgage options and think a non-conforming loan might be the right fit, connecting with a knowledgeable lending advisor can help you weigh your choices and move forward with confidence.