Not every homebuyer fits neatly into a traditional lending box. If you're self-employed, a freelancer, a real estate investor, or someone with income that's hard to document on a standard tax return, you've likely run into roadblocks when applying for a conventional mortgage. That's where a no income verification mortgage may offer a viable path forward. These alternative home loan programs are designed to help borrowers whose financial profiles don't align with the rigid documentation requirements of traditional lenders. In this guide, we'll walk you through how these loans work, who they're best suited for, the potential risks involved, and smart strategies for improving your approval odds.

What Is a No Income Verification Mortgage?

A no income verification mortgage is a type of home loan that does not require borrowers to submit traditional proof of income, such as W-2 forms, pay stubs, or federal tax returns. Instead, lenders may assess a borrower's ability to repay using alternative documentation or financial indicators.

These loans emerged in various forms over the decades and are sometimes referred to as alternative documentation loans, stated income loans, or non-QM (non-qualified mortgage) loans. It's worth noting that the original wave of "no-doc" loans that contributed to the 2008 financial crisis has largely been replaced with more responsible alternatives that still reduce documentation requirements while applying some level of financial scrutiny.

Today's versions are more structured. Lenders offering these products typically rely on factors such as:

- Bank statements (often 12 to 24 months of personal or business accounts)

- Asset depletion calculations

- Investment portfolio statements

- Debt service coverage ratios (DSCR) for real estate investors

- Proof of liquid reserves

The goal is to paint an accurate picture of a borrower's financial health without requiring the paperwork that salaried employees typically provide.

Who Typically Benefits From This Type of Home Loan?

No income verification mortgages are not for everyone, but they can be a strong fit for certain borrower profiles. Understanding whether you fall into one of these categories could save you considerable time and frustration during the mortgage process.

Self-Employed Borrowers and Freelancers

Self-employed individuals often report lower taxable income due to legitimate business deductions. While this is smart tax planning, it can make qualifying for a conventional mortgage very difficult. A bank statement loan, which is a common form of alternative income documentation, may allow lenders to assess your actual cash flow rather than just your adjusted gross income on a tax return.

Real Estate Investors

Investors who own multiple rental properties may have complex income streams that don't translate well to standard underwriting. For this group, DSCR loans — which evaluate whether the rental income from a property covers its mortgage payments — can be especially useful. These loans typically focus on the property's performance rather than the borrower's personal income.

Retirees and High-Net-Worth Individuals

Someone who is retired may have significant assets but limited reportable income. Asset depletion loans allow lenders to calculate a hypothetical monthly income based on a borrower's total liquid assets, which could make qualifying more achievable for this group.

Foreign Nationals and Non-Residents

Borrowers without U.S. tax history may also find no income verification mortgage products more accessible than conventional financing, as these programs sometimes accommodate international income documentation.

How Lenders Evaluate Risk Without Traditional Income Documents

Even without pay stubs or tax returns, lenders still need to assess credit risk carefully. Alternative mortgage lenders typically compensate for reduced documentation by tightening other qualification criteria. Here's what they commonly look at:

Credit Score Requirements

Most non-QM lenders require a minimum credit score, often in the range of 620 to 680 or higher depending on the program and loan amount. A stronger credit score may also help you secure more favorable interest rate terms. Borrowers with excellent credit histories tend to have more options available to them in the alternative lending space.

Down Payment and Loan-to-Value Ratio

Expect higher down payment requirements compared to conventional loans. Many no income verification mortgage programs require a minimum of 20% to 30% down, which reduces the lender's exposure. A lower loan-to-value (LTV) ratio gives the lender more collateral protection if a borrower defaults.

Cash Reserves

Lenders may want to see substantial liquid reserves — sometimes six to twelve months' worth of mortgage payments held in accessible accounts. This demonstrates financial stability even in the absence of a predictable paycheck.

Property Type and Condition

The type of property being financed can also influence approval. Single-family homes in stable markets may be viewed more favorably than multi-unit or non-warrantable properties. Lenders want assurance that the underlying asset holds its value over time.

Understanding the Costs and Trade-Offs Involved

No income verification mortgages come with trade-offs that borrowers should weigh carefully before proceeding. The flexibility these loans offer typically comes at a price, and being informed upfront can help you make a smarter financial decision.

Higher Interest Rates

Because lenders take on more perceived risk with reduced documentation, they often charge higher interest rates than those associated with conventional or government-backed loans. The rate difference can vary widely depending on your credit profile, down payment, and the specific lender, but it's common for borrowers to pay a premium for this flexibility.

Additional Fees and Closing Costs

Some non-QM lenders may charge origination fees or other costs that are higher than industry averages. It's important to review the loan estimate carefully and compare offers from multiple lenders before committing.

Limited Lender Options

Not all banks and credit unions offer no income verification mortgage programs. You may need to work with specialty non-QM lenders, mortgage brokers with access to alternative loan products, or private lenders. This smaller pool of options could make shopping around more time-consuming, but it's still worth the effort.

Potential for Higher Monthly Payments

Between higher interest rates and possibly shorter amortization periods on some products, monthly payments could be more substantial than those on a conventional mortgage for the same loan amount. Running the numbers carefully — ideally with the help of a mortgage professional — is strongly recommended before signing any loan agreement.

Common Types of Alternative Documentation Mortgage Programs

The term "no income verification mortgage" is often used as an umbrella for several distinct loan products. Knowing the differences can help you identify which program might align best with your financial situation.

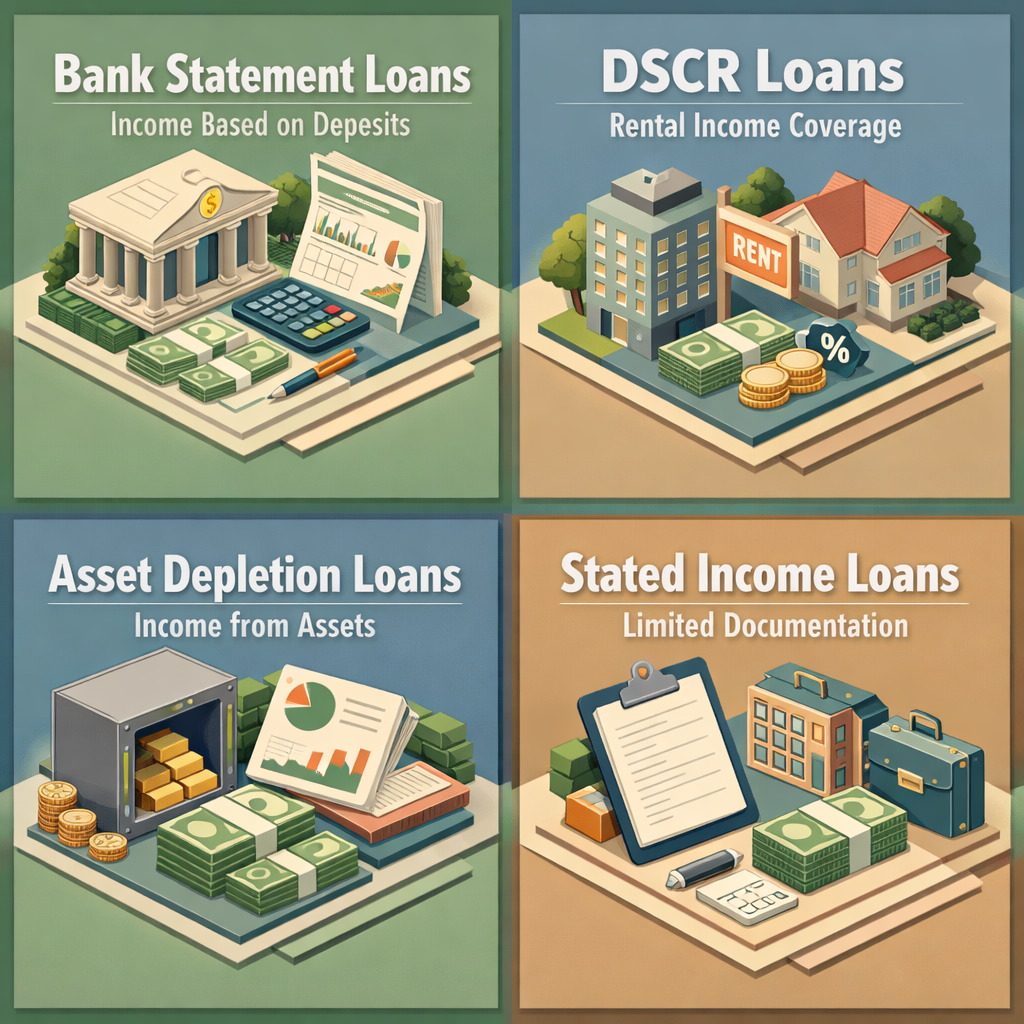

- Bank Statement Loans: Lenders review 12 to 24 months of bank statements to assess income based on deposits. This is one of the most popular options for self-employed borrowers.

- DSCR Loans: Designed for real estate investors, these loans focus on whether the property's rental income covers its debt obligations. Personal income documentation may not be required at all.

- Asset Depletion Loans: Also called asset-based loans, these calculate income by dividing a borrower's total eligible assets by the loan term in months. Useful for retirees and high-net-worth individuals.

- Stated Income Loans: These were far more common before the 2008 housing crisis. Today, they exist in a much more limited and regulated form. Some lenders may still offer variations, but with stronger compensating factors required.

- No-Ratio Loans: In this structure, the borrower's income is not calculated or verified at all — qualification relies almost entirely on assets, credit, and the property itself. These are rare and typically reserved for very high-net-worth borrowers.

Each of these programs has its own eligibility criteria, documentation requirements, and risk profile. Speaking with a licensed mortgage professional who specializes in non-QM lending can help you identify the best path forward.

Tips to Strengthen Your Application for a No Income Verification Mortgage

Even though traditional income documents aren't required, there are still proactive steps you can take to make your application more competitive. Lenders want to feel confident in your ability to repay, so the more evidence you can provide of financial stability, the better your chances of approval — and of securing a more favorable rate.

Build and Maintain a Strong Credit Profile

Your credit score carries significant weight in the non-QM lending world. Pay down existing debts, avoid opening new credit lines close to your application date, and review your credit report for any errors that could be dragging your score down. Even a modest improvement in your credit score could open up better loan terms.

Maximize Your Liquid Reserves

Having six to twelve months — or even more — of mortgage payments sitting in liquid, accessible accounts sends a strong signal to lenders. If you're approaching a home purchase, it may be worth holding off on large withdrawals or investments that would reduce your visible reserves.

Document Everything You Can

Even if traditional income verification isn't required, providing supplementary documentation — such as CPA letters, business licenses, profit and loss statements, or investment account summaries — can help round out your financial picture and build lender confidence.

Work With a Specialist

Not every loan officer is well-versed in non-QM products. Partnering with a mortgage broker or lender who specializes in alternative lending programs can make a meaningful difference in both your approval odds and the quality of the loan terms you receive. To improve your approval chances, working with the right specialist is key.

●Conclusion

A no income verification mortgage can be a practical and legitimate financing solution for borrowers whose income doesn't fit the traditional mold. Whether you're self-employed, a seasoned real estate investor, a retiree with significant assets, or simply someone with a non-traditional income stream, these alternative loan programs may offer the flexibility you need to purchase or refinance a home. That said, it's important to go in with clear expectations — higher rates, larger down payments, and a smaller pool of lenders are common realities of this space. The smartest move you can make is to work with a knowledgeable mortgage professional who can help you compare programs, understand the true cost of each option, and match you with a product that fits your long-term financial goals. At LoanWise, we're here to help you navigate the lending landscape with confidence — no matter how unique your financial story may be.