Smart Refinance Strategies for Lower Payments

Real estate investors are finding themselves in a unique position as mortgage rates have dropped to approximately 6% in early 2026. This mortgage refinance for lower payments opportunity could significantly impact your investment portfolio's cash flow and overall returns. With refinancing markets opening up for nearly 5 million property owners, understanding the right strategies becomes crucial for maximizing your investment potential.

The recent rate decline has created conditions that might benefit investors looking to reduce their monthly obligations on rental properties and fix-and-flip projects. However, refinancing decisions require careful evaluation of your specific investment goals and current loan terms.

Essential Pre-Refinance Checklist for Investment Properties

Before diving into a mortgage refinance for lower payments, smart investors typically review these critical factors to ensure they're making the right financial decision.

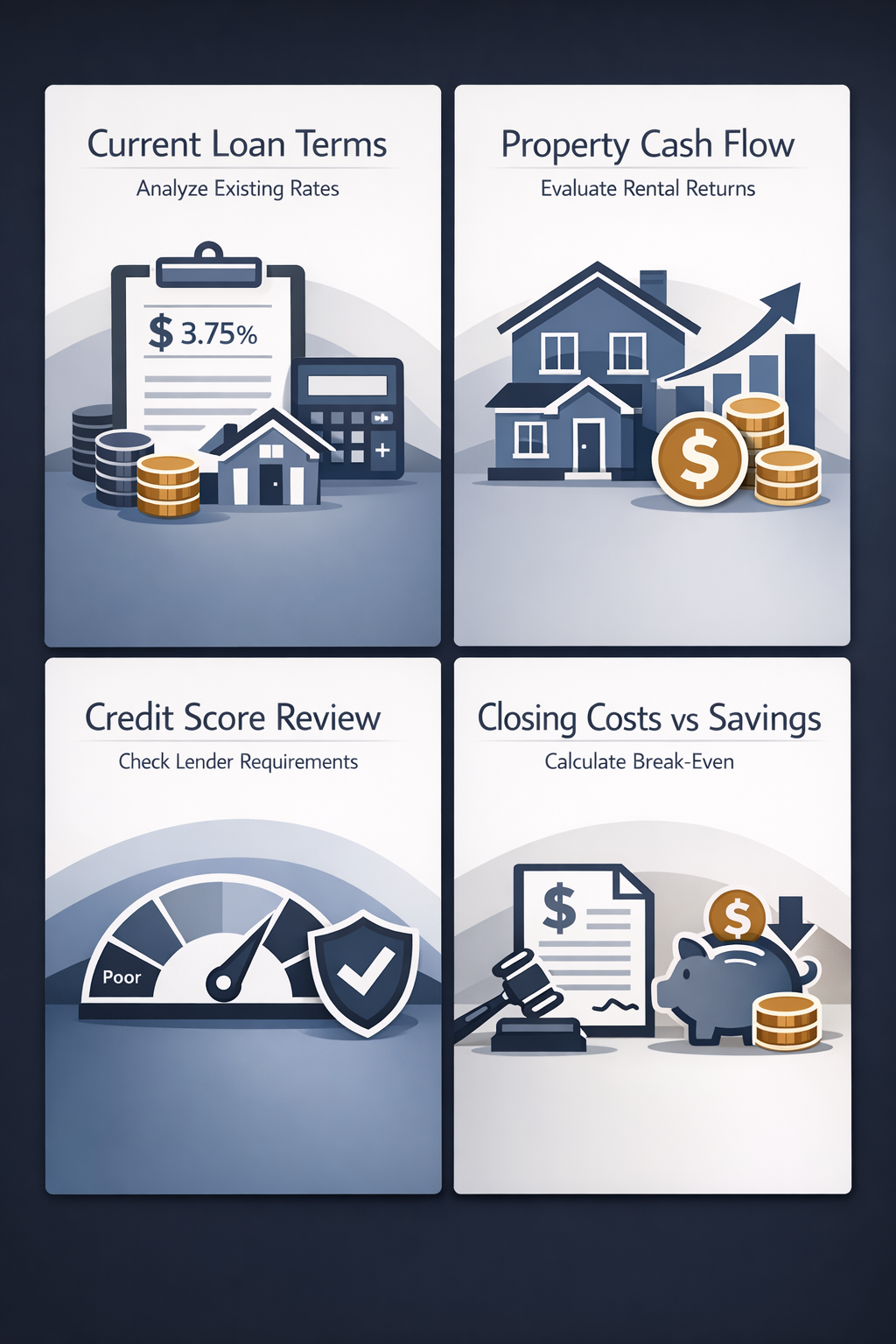

- Current loan terms analysis: Compare your existing interest rate, remaining loan balance, and monthly payment against current market offerings to determine potential savings

- Property cash flow evaluation: Calculate how reduced monthly payments could improve your rental property's cash-on-cash return and overall profitability

- Credit score and debt-to-income review: Ensure your financial profile meets lender requirements for the most favorable refinancing terms available

- Closing costs vs. savings calculation: Factor in refinancing fees against long-term monthly payment reductions to determine break-even timeline

Market Conditions Favoring Lower Payment Refinancing

The current refinancing landscape presents several advantages for real estate investors seeking to reduce their monthly payment obligations on investment properties.

- Rate environment improvement: Mortgage rates falling to around 6% create opportunities for investors with higher-rate loans to potentially secure meaningful payment reductions

- Increased lender competition: More refinance-eligible borrowers in the market may lead to competitive loan terms and reduced fees from financial institutions

- Affordability peaks reached: Current market conditions suggest optimal timing for investors to lock in lower rates before potential future increases

- Expanded refinancing pool: With nearly 5 million homeowners becoming refinance-eligible, lenders might offer more attractive terms to capture market share

DSCR Loan Refinancing Benefits for Rental Properties

DSCR loan refinancing could offer unique advantages for investors focused on rental property cash flow optimization and portfolio expansion strategies.

- Income-based qualification: DSCR loans typically qualify borrowers based on property cash flow rather than personal income, making refinancing more accessible for portfolio investors

- Streamlined approval process: These loan products might reduce documentation requirements compared to traditional refinancing options for investment properties

- Portfolio scalability: Lower monthly payments through DSCR refinancing could free up capital for additional property acquisitions or improvements

- Cash flow optimization: Reduced debt service payments directly improve your property's debt service coverage ratio and overall investment performance

Step-by-Step Lower Payment Refinancing Process

Following a systematic approach to refinancing to lower monthly mortgage payment helps ensure you secure the best possible terms for your investment properties.

- Market research and lender comparison: Contact multiple mortgage lenders to compare rates, terms, and fees specific to investment property refinancing products

- Financial documentation preparation: Gather rental income statements, property tax records, insurance information, and current loan details for streamlined application processing

- Property valuation and analysis: Obtain current market valuations to understand your loan-to-value ratio and potential refinancing options available

- Application submission and rate lock: Submit applications with your top lender choices and consider locking favorable rates to protect against market fluctuations

- Closing coordination and fund management: Coordinate closing timeline with your investment schedule and prepare for temporary cash flow adjustments during the transition period

Calculating Refinancing Savings and Break-Even Points

Understanding the financial impact of your mortgage refinance for lower payments requires careful analysis of both immediate costs and long-term benefits to your investment strategy.

- Monthly payment reduction calculation: Subtract your new projected monthly payment from current payment to determine immediate cash flow improvement for your rental properties

- Total closing cost assessment: Add all refinancing fees, appraisal costs, and lender charges to establish your upfront investment in the refinancing process

- Break-even timeline analysis: Divide total closing costs by monthly payment savings to determine how many months until refinancing pays for itself

- Long-term savings projection: Calculate total interest savings over the remaining loan term to understand the full financial benefit of your refinancing decision

- Return on investment evaluation: Compare refinancing costs against improved cash flow and interest savings to ensure the decision aligns with your investment goals

Alternative Refinancing Strategies for Investment Properties

Beyond traditional refinancing for lower monthly payments, several specialized strategies might better serve specific investment objectives and portfolio management goals.

- Cash-out refinancing for portfolio expansion: Extract equity from performing properties to fund new acquisitions, though this typically increases monthly payments while providing capital for growth

- Term extension for payment reduction: Extending loan terms from 15 to 30 years could significantly reduce monthly obligations, improving short-term cash flow at the cost of higher total interest

- Bridge loan refinancing for fix-and-flip projects: Replace short-term bridge financing with conventional loans once renovations complete, potentially securing lower rates and extended terms

- Portfolio consolidation refinancing: Combine multiple property loans into a single financing package, which might offer better terms and simplified payment management

Maximizing Your Refinancing Success

The benefits of refinancing for lower payments extend beyond simple monthly payment reduction when approached strategically. Current market conditions with rates around 6% might present a limited-time opportunity for real estate investors to optimize their portfolio financing. Success in refinancing typically depends on thorough preparation, careful lender selection, and alignment with your broader investment strategy. Consider working with mortgage professionals who understand investment property financing to ensure you're capturing all available benefits while avoiding potential pitfalls that could impact your portfolio's performance.

●Conclusion

With mortgage rates dropping to approximately 6% and refinancing opportunities expanding, real estate investors have a potentially valuable window to reduce their monthly payment obligations. The key to successful mortgage refinance for lower payments lies in careful analysis of your current loan terms, market conditions, and investment objectives. Whether you're managing rental properties or planning fix-and-flip projects, lower monthly payments could improve cash flow and create opportunities for portfolio expansion. Consider consulting with investment-focused mortgage professionals to explore how current refinancing options might benefit your specific situation and long-term investment goals.