Mortgage for Foreign Nationals: Your Complete Investment Guide

International real estate investors face unique challenges when seeking financing for U.S. properties. A mortgage for foreign nationals operates differently from traditional lending products, requiring specialized knowledge of documentation, down payment requirements, and alternative financing options like DSCR loans. Understanding these requirements can unlock significant investment opportunities in the American real estate market for non-resident investors.

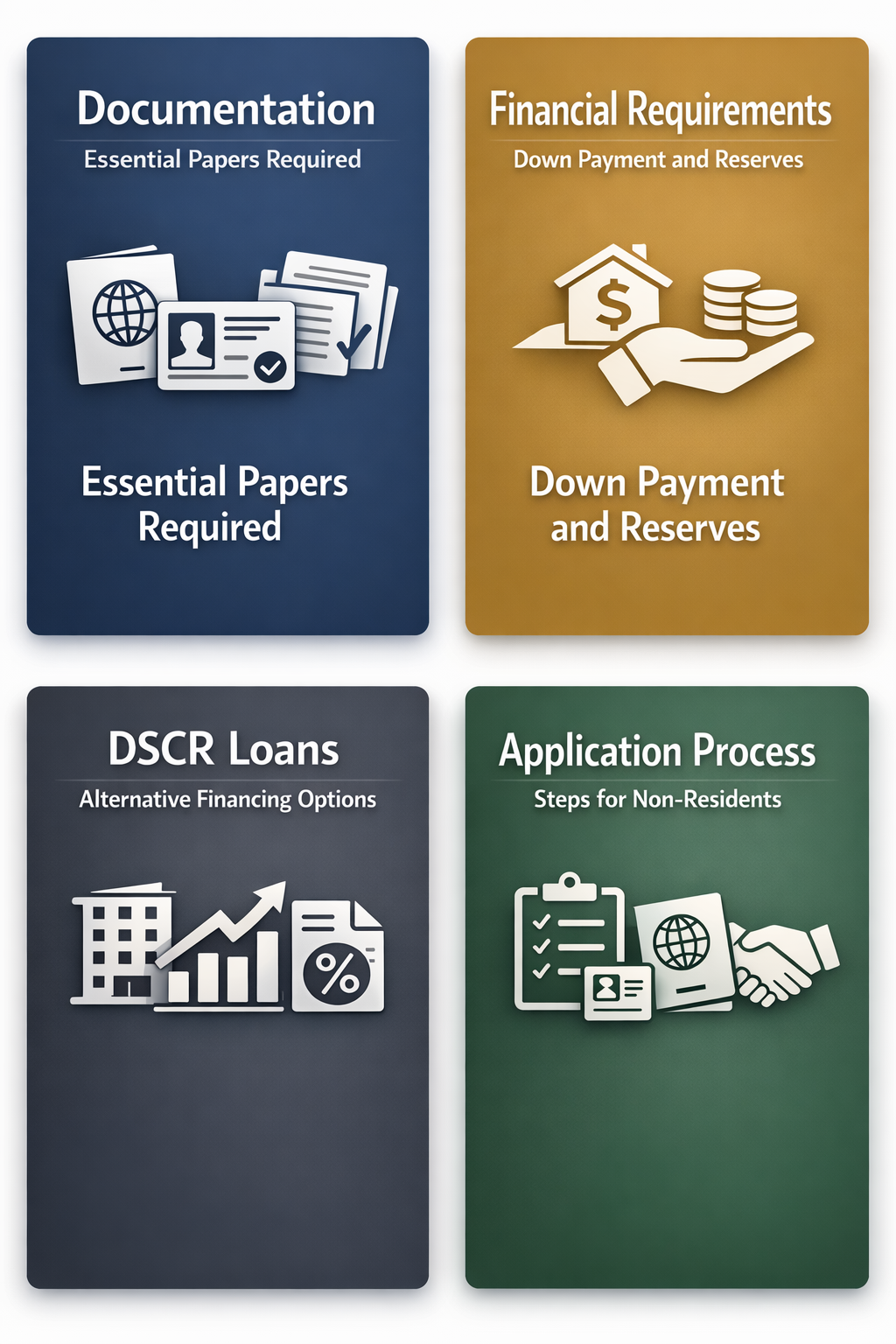

Essential Documentation Requirements for Foreign National Mortgages

Essential documentation requirements for foreign national mortgages typically involve more comprehensive paperwork than traditional domestic loans. International investors must prepare specific documents that prove their identity, income, and investment intentions to secure U.S. real estate financing.

- Valid passport and visa documentation serve as primary identification for foreign nationals applying for U.S. mortgages

- Proof of income from home country including tax returns, employment letters, and bank statements translated into English

- Credit reports from home country may be required, though some lenders offer alternative credit evaluation methods

- Investment property documentation detailing the intended use and rental income potential of the target property

Down Payment and Financial Requirements for International Investors

Down payment and financial requirements for international investors typically demand higher initial investments compared to domestic buyers. Foreign nationals often face stricter financial criteria due to perceived lending risks associated with non-resident borrowers.

- Down payment ranges from 20% to 25% for most foreign national mortgage programs, significantly higher than domestic investor requirements

- Cash reserves equivalent to 2-6 months of mortgage payments may be required to demonstrate financial stability

- Debt-to-income ratios might be calculated differently, often requiring lower ratios than domestic borrowers

- Currency exchange documentation showing the source and conversion of foreign funds for the transaction

DSCR Loans: Alternative Financing for Foreign Real Estate Investors

DSCR loans alternative financing for foreign real estate investors offers a pathway to U.S. property ownership without traditional income documentation. These debt service coverage ratio loans focus on rental income potential rather than personal income verification, making them particularly attractive for international investors.

- Income qualification based on property cash flow rather than personal employment history or tax returns

- No employment verification required from foreign countries, simplifying the application process significantly

- Property rental income projections serve as the primary qualification metric for loan approval

- Faster approval processes compared to traditional foreign national mortgage programs due to reduced documentation requirements

Step-by-Step Application Process for Non-Resident Investors

Step-by-step application process for non-resident investors requires careful planning and timing to navigate U.S. mortgage systems effectively. International investors benefit from understanding each phase of the application timeline and preparing accordingly.

- Pre-qualification phase involves initial document review and financial assessment to determine borrowing capacity and loan program eligibility

- Property identification and contract negotiation requires coordination with real estate professionals familiar with foreign buyer transactions

- Formal application submission includes comprehensive documentation package and property appraisal scheduling

- Underwriting and approval process typically takes 30-45 days, during which lenders verify all submitted documentation

- Closing preparation and fund transfer involves international wire transfers and final document execution with legal representation

Specialized Mortgage Programs Available to Foreign Nationals

Specialized mortgage programs available to foreign nationals cater to different investment strategies and financial situations. These targeted lending products recognize the unique circumstances of international investors and provide tailored financing solutions.

- Foreign national conventional programs offer traditional mortgage structures with modified qualification criteria for non-resident borrowers

- Portfolio lending products provide more flexible underwriting guidelines through lenders who retain loans in-house rather than selling to government agencies

- Bridge financing options enable quick property acquisitions while foreign nationals arrange permanent financing or currency transfers

- Commercial investment loans target larger multifamily properties and commercial real estate investments for sophisticated international investors

●Conclusion

Securing a mortgage for foreign nationals requires careful preparation, higher down payments, and often alternative financing approaches like DSCR loans. International investors who understand these requirements and work with experienced lenders can successfully access the U.S. real estate market. The key lies in proper documentation, adequate capital reserves, and choosing the right loan program that matches your investment strategy and financial profile.