Shipping container homes have captured the imagination of homebuyers across the country. They're modern, sustainable, and often more affordable to build than traditional houses. But when it comes to financing, many prospective owners hit a wall. If you're wondering how to get a mortgage for a house built with shipping containers, you're not alone. Lenders tend to treat these properties differently, and navigating the process requires some preparation. The good news is that financing options do exist — you just need to know where to look and what to expect.

Why Shipping Container Homes Are Harder to Finance

Before diving into solutions, it helps to understand the challenge. Most mortgage lenders rely on standardized appraisal guidelines and property classifications. A shipping container home doesn't always fit neatly into those boxes — literally or figuratively.

Traditional lenders, including banks and credit unions, typically require that a home meet certain building codes, be permanently affixed to a foundation, and qualify as real property rather than personal property. Shipping container homes may or may not meet these requirements depending on how they're constructed, where they're located, and how local municipalities classify them.

Appraisers may also struggle to find comparable sales — often called comps — in the area, which makes it harder to establish a fair market value. Without a solid appraisal, many loan programs simply won't approve the financing. That said, this landscape is slowly evolving as container homes become more mainstream and lenders grow more familiar with them.

Understanding How Lenders Classify Your Container Home

One of the most important factors in securing financing is how your home is legally classified. There are two main categories lenders consider: real property and personal property. This distinction matters enormously for your loan options.

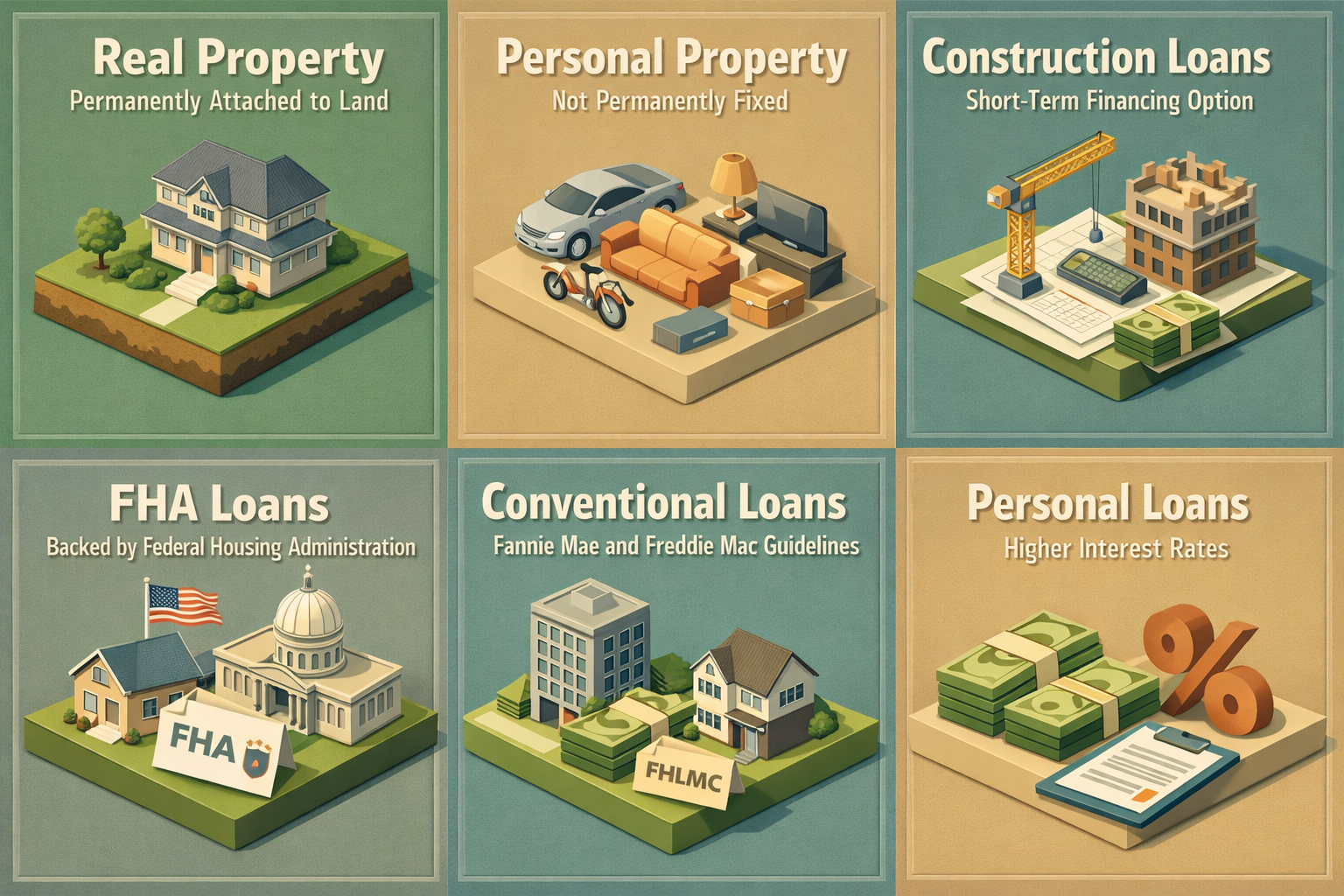

- Real property: The home is permanently attached to land you own. This classification opens the door to traditional mortgage products and generally offers lower interest rates and longer repayment terms.

- Personal property: The home is not permanently fixed to owned land — it may be placed on leased land or remain movable. Financing in this category is typically more limited, often requiring a personal loan or chattel loan with higher rates.

To maximize your financing options, many lenders and housing experts suggest ensuring your container home is built on a permanent foundation and that you hold title to the land. Additionally, making sure the structure complies with local building codes and is classified as a single-family dwelling can significantly improve your chances of qualifying for a conventional or government-backed mortgage.

Shipping Container Home Financing Options Worth Exploring

When it comes to shipping container home financing options, there isn't a one-size-fits-all solution. However, several pathways may be available depending on your situation, the property's classification, and your financial profile.

Construction Loans

If your container home hasn't been built yet, a construction loan is often the most natural starting point. These short-term loans cover the cost of building the home and typically convert into a traditional mortgage once construction is complete — a process known as a construction-to-permanent loan. You'll generally need detailed construction plans, a licensed builder, and a solid credit profile to qualify. Some lenders may be hesitant with non-traditional builds, so it's important to work with a lender who has experience financing alternative housing types.

FHA Loans

FHA loans, backed by the Federal Housing Administration, could potentially be used for container homes — but only if the property meets HUD's minimum property standards and is classified as a traditional dwelling. The home must be on a permanent foundation, titled as real estate, and pass an FHA appraisal. Because these requirements are strict, not every container home will qualify, but those that are built to conventional housing standards may have a reasonable chance.

Conventional Loans

Conventional mortgages follow Fannie Mae and Freddie Mac guidelines. These programs can be used for container homes if the property meets their standard requirements for structural integrity, habitability, and appraised value. Again, permanent foundation placement and proper local permitting are typically essential. Finding a lender familiar with alternative construction types is key to making a conventional loan work for a container home.

Personal Loans

For smaller container home projects or situations where the home doesn't qualify as real property, a personal loan may serve as a viable option. These loans don't require the property to serve as collateral, which removes some of the classification hurdles. The tradeoff is that personal loans often come with higher interest rates and shorter repayment periods, which can make monthly payments less manageable on larger builds.

Portfolio Loans

Some community banks and credit unions offer portfolio loans — mortgages they keep in-house rather than selling to the secondary market. Because these lenders set their own guidelines, they may be more flexible about financing non-traditional properties like container homes. If you've been turned down elsewhere, a local lender offering portfolio products could be worth exploring.

Key Steps to Prepare Before You Apply for Financing

Knowing how to get a mortgage for a house built with shipping containers isn't just about understanding loan types — it's also about preparing your application strategically. Here's what you can do to put your best foot forward.

- Review your credit score: Most mortgage programs have minimum credit score requirements. A stronger credit profile generally leads to better loan terms and higher approval odds. Before applying, check your credit report for errors and address any outstanding issues.

- Secure proper permits and plans: Work with a licensed contractor or architect and obtain all necessary building permits from your local municipality. Having documented, code-compliant construction plans demonstrates to lenders that the project meets minimum standards.

- Choose the right land: Owning the land where your container home will sit — rather than leasing it — significantly improves your financing prospects. If possible, purchase the land before or alongside the home construction.

- Get a professional appraisal: Consider hiring an independent appraiser who has experience valuing alternative or non-traditional homes. Their valuation can help support your loan application and give lenders more confidence in the property's worth.

- Save for a larger down payment: Because container homes carry more perceived risk for lenders, you may be asked to put down a larger down payment than you would on a conventional home. Having extra reserves ready can also strengthen your application.

Working with the Right Lender Makes All the Difference

Not every lender is equipped or willing to finance a shipping container home. Choosing the wrong one can lead to wasted time and unnecessary frustration. Instead, look for lenders with experience in alternative construction financing, specialty residential lending, or rural and non-traditional property types.

Mortgage brokers can be particularly useful in this situation. Because brokers work with multiple lenders, they may have access to niche programs or portfolio lenders who are open to container home financing. They can also help you compare rates and terms across several options, saving you from having to shop independently.

It's also worth asking lenders directly about their experience with container homes before submitting a full application. Some lenders may be willing to do a preliminary review of your project to let you know whether financing is feasible before you go through the formal underwriting process.

Community banks and credit unions are another group worth approaching. They often take a more relationship-based approach to lending and may be more willing to work through the unique aspects of a container home project — especially if you're an existing customer with a strong financial history.

Zoning Laws and Local Regulations You Need to Know

Financing a shipping container home is only one piece of the puzzle. Before you can get a mortgage lender to say yes, your local government also has to say yes. Zoning laws, building codes, and local ordinances vary widely across states and municipalities, and some areas may not permit container homes at all.

Research the zoning classification of your intended property. Container homes may be allowed in areas zoned for residential construction, but some zones have specific restrictions on what types of structures can be placed there. In rural areas, regulations might be more lenient, while urban and suburban municipalities may require your container home to be virtually indistinguishable from a traditional stick-built house.

Working with a local real estate attorney or an experienced contractor familiar with container home builds in your area can help you navigate these rules. Securing proper permits and meeting all local codes isn't just a legal requirement — it's also one of the most important steps in making your container home lendable and insurable.

Insurance Considerations That Affect Your Loan Approval

Lenders universally require homeowners insurance as a condition of any mortgage. For container homes, obtaining adequate coverage may require some extra legwork. Not all standard homeowners insurance policies cover non-traditional structures, so you may need to seek out specialty insurers who have experience with alternative housing.

When shopping for insurance, look for policies that specifically cover the materials and construction methods used in container homes. Steel structures have different risk profiles than wood-frame houses, and your policy should reflect that. Some insurers may also require a professional inspection before issuing coverage.

Having insurance in place — or at least a commitment letter from an insurer — before you approach lenders can actually strengthen your loan application. It signals to lenders that the property is insurable, which reduces one of their key concerns about alternative property types. If you're working with a mortgage broker or housing consultant, they may be able to point you toward insurers familiar with container home coverage.

●Conclusion

Learning how to get a mortgage for a house built with shipping containers takes patience, preparation, and the right team of professionals. While the path isn't always straightforward, it's absolutely possible with the right approach. From choosing the correct legal classification and loan type to working with experienced lenders and meeting local building codes, each step you take brings you closer to securing your container home. Explore your shipping container home financing options carefully, ask plenty of questions, and don't hesitate to work with a knowledgeable mortgage broker who can help you find the right fit. With the right guidance, your container home dream could become a very real address.