If you're receiving alimony payments after a divorce, you may be wondering whether that income can help you qualify for a home loan. The good news is that it often can — but the process requires some preparation. Understanding how to calculate mortgage affordability with alimony income is an important step for anyone navigating homeownership after a major life change. Lenders have specific rules around how alimony is treated, and knowing those rules ahead of time can give you a significant advantage when you're ready to apply.

What Alimony Income Means for Mortgage Lenders

Alimony, sometimes called spousal support or maintenance, is a court-ordered payment made from one former spouse to another. From a lender's perspective, it's considered a form of non-employment income — similar in some ways to child support, pension payments, or rental income. However, not every lender treats it identically, and the rules can vary depending on the loan program you're applying for.

Most conventional lenders, as well as those offering FHA and VA loans, will count alimony income as qualifying income — but only under certain conditions. The income typically needs to be stable, consistent, and expected to continue for a defined period after the mortgage closes. Lenders want confidence that the income won't disappear shortly after you take on a new monthly mortgage obligation.

It's also worth noting that alimony income is treated differently from child support in some underwriting guidelines, so it's important to be clear about which type of payment you're receiving when speaking with a loan officer.

Key Requirements Lenders Look For Before Counting Alimony

Before a lender will include your alimony payments in the income calculation, you'll typically need to meet a few standard requirements. While guidelines can vary between loan programs and individual lenders, the following conditions are commonly expected:

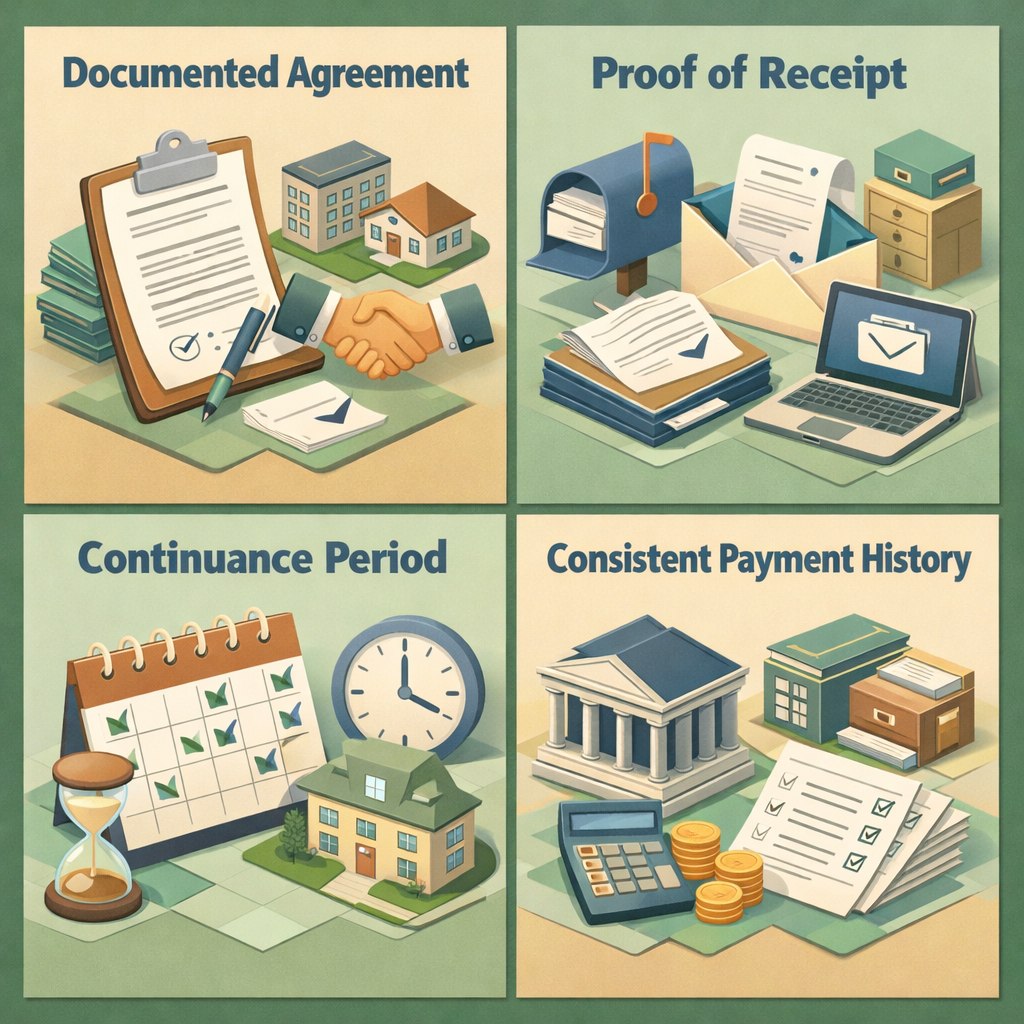

- Documented agreement: You'll need a copy of your divorce decree, separation agreement, or court order that clearly outlines the alimony amount and payment schedule.

- Proof of receipt: Lenders usually want to see that payments have been received consistently — often for a period of six to twelve months — through bank statements or similar financial records.

- Continuance period: Many lenders require that the alimony payments are expected to continue for at least three years from the date of the mortgage application. This is a common benchmark under conventional lending guidelines.

- Consistent payment history: A track record of on-time, full payments from the paying spouse helps demonstrate reliability. Any gaps or partial payments could raise concerns during underwriting.

If you can satisfy these conditions, your alimony income may be counted alongside wages, self-employment earnings, or other qualifying income sources when a lender evaluates your application.

How to Calculate Mortgage Affordability With Alimony Income Step by Step

Knowing how to calculate mortgage affordability with alimony income starts with understanding how lenders measure your overall financial picture. The central metric is your debt-to-income ratio, or DTI. This ratio compares your total monthly debt obligations to your gross monthly income — and it plays a major role in determining how much home you can afford.

Step 1: Add Up Your Monthly Income

Start by tallying all qualifying income sources. This might include wages from employment, freelance or self-employment income, investment income, and your monthly alimony payments. For alimony, use the amount stated in your court order or separation agreement — not an informal arrangement.

Step 2: Calculate Your Monthly Debt Obligations

Next, list your current monthly debt payments. These typically include credit card minimums, auto loans, student loans, personal loans, and any other recurring debt obligations. Don't include everyday expenses like groceries or utilities — lenders focus on installment and revolving debt.

Step 3: Compute Your Debt-to-Income Ratio

Divide your total monthly debts by your total gross monthly income (including alimony) and multiply by 100 to get your DTI percentage. For example, if your monthly debts total $1,200 and your gross monthly income — including alimony — is $5,000, your DTI would be 24%. Most conventional loan programs prefer a DTI at or below 43%, though some programs may allow higher ratios with strong compensating factors.

Step 4: Estimate Your Maximum Mortgage Payment

Subtract your existing monthly debts from the maximum allowable monthly debt load (based on your lender's DTI threshold and your gross income). The result gives you a rough ceiling for what your monthly mortgage payment could be. From there, you can use a mortgage affordability calculator to estimate the loan amount that fits within that payment range at current interest rates.

Documentation You'll Need to Support Your Alimony Income

When applying for a mortgage, documentation is everything. Lenders need a clear paper trail to verify that your alimony income is real, reliable, and legally enforceable. Being organized before you apply can speed up the underwriting process considerably.

Here's what you'll typically be asked to provide:

- Divorce decree or legal separation agreement: This document should specify the monthly alimony amount, payment schedule, and duration.

- Bank statements: Typically covering the past 12 months, showing consistent deposits that match the agreed-upon alimony amount.

- Award letter or court order: In some cases, lenders may request additional legal documentation to confirm the court-ordered nature of the payments.

- Tax returns: Your most recent one to two years of federal tax returns may be required, especially if alimony represents a significant portion of your total income.

It's a smart idea to gather these materials early in the homebuying process. If any documentation is missing or inconsistent, it could delay your application or reduce the amount of income your lender is willing to count.

How Loan Programs Differ in Their Treatment of Spousal Support Income

Not all mortgage programs handle alimony income in exactly the same way. Here's a general overview of how common loan types may approach it:

Conventional Loans

Conventional loans underwritten to Fannie Mae or Freddie Mac guidelines typically allow alimony income if it's documented, consistent, and expected to continue for at least three years. These loans often provide flexibility for borrowers with strong credit profiles.

FHA Loans

FHA loans, backed by the Federal Housing Administration, also generally permit alimony income to be counted toward qualification. Borrowers who may have lower credit scores or smaller down payments often consider FHA loans as a pathway to homeownership, and alimony income can meaningfully increase their qualifying power.

VA Loans

For veterans and active-duty service members, VA loans offer competitive terms and may also recognize alimony as qualifying income, subject to similar documentation requirements. VA loans use a residual income method in addition to DTI, so the full picture of your finances matters.

USDA Loans

USDA loans, designed for rural and some suburban homebuyers, may also count alimony toward income eligibility, though lenders will apply their own documentation standards. Income limits apply under this program, so borrowers should confirm that their total qualifying income — including alimony — falls within the acceptable range for their area.

Strategies to Strengthen Your Mortgage Application as an Alimony Recipient

Even with qualifying alimony income, there are additional steps you can take to improve your overall mortgage profile. A stronger application could lead to better loan terms, lower interest rates, or access to a larger loan amount.

- Build or maintain strong credit: Your credit score remains one of the most influential factors in mortgage approval. Paying bills on time, keeping credit card balances low, and avoiding new debt before applying can all help.

- Save for a larger down payment: A higher down payment reduces your loan-to-value ratio, which may lower your interest rate and eliminate the need for private mortgage insurance on conventional loans.

- Reduce existing debt: Paying down credit cards or auto loans before applying can improve your DTI ratio, which makes more room for a larger mortgage payment.

- Establish a financial paper trail early: If you've recently started receiving alimony, begin depositing payments into a bank account immediately and consistently. The longer and cleaner your payment history, the stronger your documentation will be.

- Work with an experienced loan officer: Not all lenders have the same familiarity with non-traditional income sources. A loan officer who regularly works with divorced or newly single borrowers may be better equipped to navigate your specific situation.

Common Pitfalls to Avoid When Using Alimony Income for a Home Loan

Understanding alimony income mortgage affordability also means being aware of the mistakes that could derail your application. Here are a few common issues to watch out for:

- Cash payments with no documentation: If alimony is paid in cash without a clear bank record, lenders may not be able to count it. Always ensure payments are traceable through your bank account.

- Informal agreements: A verbal or handshake arrangement — even between amicable ex-spouses — won't satisfy underwriting requirements. You need a court order or formal legal document.

- Overestimating future payments: If your alimony is set to decrease or expire within three years, a lender may not count the full amount or may exclude it altogether. Be transparent about the terms.

- Failing to disclose alimony obligations: If you're the one paying alimony rather than receiving it, that obligation will typically be counted as a monthly debt in your DTI calculation. Failing to disclose it could be considered misrepresentation on a mortgage application.

- Applying before your payment history is established: If you've only received a few months of payments, it may be worth waiting until you have a longer, more consistent track record before applying.

Avoiding these pitfalls can make the difference between a smooth closing and an unexpected denial.

●Conclusion

Navigating homeownership after a divorce or separation can feel overwhelming, but understanding how to calculate mortgage affordability with alimony income puts you in a much stronger position. By knowing what lenders look for, gathering the right documentation, and applying smart financial strategies, you may be able to qualify for a mortgage that supports the next chapter of your life. Every borrower's situation is unique, so consider speaking with a qualified loan officer at LoanWise who can help you evaluate your income, DTI, and loan options in detail. With the right guidance, homeownership may be closer than you think.