An adjustable-rate mortgage, or ARM, can be an attractive option for homebuyers and homeowners who want a lower initial interest rate. But because the rate can change over time, figuring out what you can truly afford takes a bit more thought than with a fixed-rate loan. Knowing how to calculate affordability for ARM mortgage financing is one of the most important steps you can take before signing on the dotted line. This guide walks you through the key concepts, the numbers that matter, and the tools that can help you make a confident, informed decision.

What Makes an ARM Different From a Fixed-Rate Mortgage

Before diving into the math, it helps to understand what sets an ARM apart. With a fixed-rate mortgage, your interest rate stays the same for the entire loan term. Your monthly principal and interest payment never changes, which makes budgeting straightforward.

An ARM, on the other hand, starts with a fixed introductory period — commonly three, five, seven, or ten years — during which your rate stays locked. After that initial period ends, the rate adjusts periodically based on a financial index plus a margin set by your lender. Common indexes used today include the Secured Overnight Financing Rate (SOFR) and the Constant Maturity Treasury (CMT) index.

ARM loans are often described using a shorthand like 5/1 ARM or 7/6 ARM. The first number tells you how long your initial fixed period lasts. The second number tells you how often the rate adjusts after that — every one year or every six months, respectively.

This built-in variability is precisely why affordability planning for an ARM requires a broader lens. You're not just asking what your payment is today — you're asking what it could become, and whether you'd still be comfortable if it rose.

Key Numbers You Need Before Using an ARM Mortgage Affordability Calculator

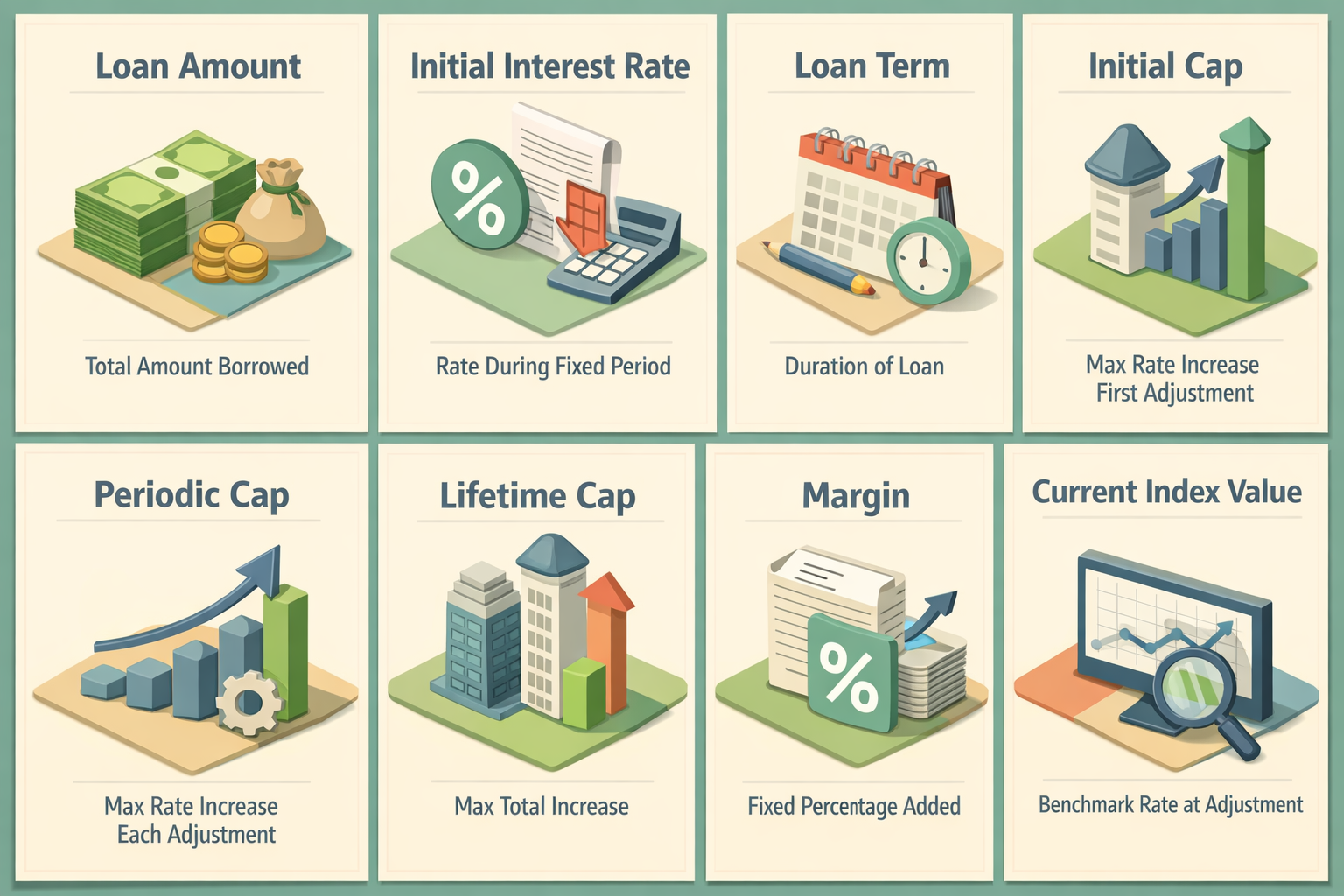

Whether you're using an online ARM mortgage affordability calculator or working through the numbers manually, you'll need to gather a few essential inputs first. Having these ready makes the process much smoother.

- Loan amount: The total amount you plan to borrow, which is the home purchase price minus your down payment.

- Initial interest rate: The rate that applies during the fixed introductory period. This is typically lower than a comparable fixed-rate mortgage.

- Loan term: Most ARMs are structured over a 30-year term, though 15-year and 20-year options may be available.

- Initial cap: The maximum amount the rate can increase at the first adjustment. This is often 2% or 5%, depending on the loan program.

- Periodic cap: The maximum amount the rate can increase at each subsequent adjustment, commonly 1% or 2%.

- Lifetime cap: The maximum total increase over the life of the loan, typically 5% above the starting rate.

- Margin: A fixed percentage your lender adds to the index at each adjustment to determine your new rate.

- Current index value: The benchmark rate your ARM is tied to at the time of adjustment.

Once you have these numbers, an ARM affordability calculator can model both your initial payment and potential future payments under different rate scenarios. This gives you a much clearer picture of your true exposure.

How to Calculate Affordability for ARM Mortgage Step by Step

Understanding how to calculate affordability for ARM mortgage loans involves two stages: calculating your initial payment and then stress-testing future payments based on rate caps.

Step 1: Calculate Your Initial Monthly Payment

Your initial payment is calculated like any standard mortgage. You use the standard amortization formula with your loan amount, initial interest rate, and loan term. For example, if you borrow $350,000 at a 6.0% initial rate on a 30-year ARM, your starting principal and interest payment would be approximately $2,098 per month.

Step 2: Model the Worst-Case Adjusted Payment

This is where ARM affordability planning differs from fixed-rate planning. You'll want to calculate affordability for what your payment could look like if the rate rises to its maximum allowed level. Using the same example, if your initial cap is 2% and your lifetime cap is 5%, your rate could potentially reach 11.0% after all adjustments. At that level on a remaining loan balance, your payment could rise significantly — sometimes by several hundred dollars per month.

Step 3: Apply the Debt-to-Income Rule

Lenders typically want your total monthly debt obligations — including your mortgage payment — to stay within a certain percentage of your gross monthly income. This ratio is called the debt-to-income (DTI) ratio. Most conventional lenders prefer a DTI at or below 43%, though some may allow slightly higher ratios with compensating factors like strong credit or large reserves. When calculating affordability, it's wise to apply the DTI test not just to your initial payment, but also to your worst-case adjusted payment.

Step 4: Factor In Taxes, Insurance, and HOA Fees

Your total housing cost includes more than principal and interest. Property taxes, homeowners insurance, and any HOA dues all count toward your monthly obligation. Make sure your affordability calculation includes all of these costs so you're not surprised later.

Understanding ARM Payment Changes Over Time

Understanding ARM payment changes is essential for long-term financial planning. Many borrowers focus entirely on the initial rate — which is often appealingly low — without fully grasping how much payments could shift after the fixed period ends.

Here's how the adjustment process typically works. At each adjustment date, your lender calculates a new rate by adding the current index value to your margin. For example, if the index is at 4.5% and your margin is 2.75%, your new rate would be 7.25% — subject to the cap limits in your loan agreement.

If that new rate is higher than your initial rate, your payment goes up. If the index has fallen, your rate — and payment — may actually decrease. ARMs can move in both directions, which is one reason they can be appealing in a declining rate environment.

It's also worth knowing that when your rate adjusts, your remaining loan balance and remaining term are used to recalculate the payment. This means the impact of a rate increase may be somewhat softened if you've already paid down a meaningful portion of the principal. Still, the safest approach is to plan as though rates will rise to their cap and confirm that your budget can handle that outcome.

Factors Affecting ARM Loan Qualification That Borrowers Often Overlook

Several factors affecting ARM loan qualification go beyond just your income and credit score. Understanding these can help you prepare a stronger application and avoid unexpected surprises during underwriting.

- Credit score requirements: ARMs, like other mortgage products, typically require a minimum credit score. Conventional ARMs often require a score of at least 620, while jumbo ARMs may require 700 or higher. A stronger credit score can also help you secure a lower initial rate and margin.

- Qualifying rate: Some lenders qualify borrowers at a rate higher than the initial note rate — often the fully indexed rate or the initial rate plus a certain percentage. This is a protective measure to ensure you could handle future payment increases.

- Reserves: Lenders may want to see that you have several months of mortgage payments in reserve after closing. This is especially true for jumbo ARMs or investment property loans.

- Loan-to-value ratio (LTV): A lower LTV — meaning a larger down payment — may improve your qualification odds and potentially your rate. Some ARM programs limit availability to borrowers with LTVs below a certain threshold.

- Property type: Investment properties and second homes often face stricter ARM qualification requirements than primary residences.

- Employment and income stability: Since ARM payments can rise, lenders may scrutinize income stability more carefully than with fixed-rate loans. Self-employed borrowers may need to provide additional documentation.

Being aware of these factors ahead of time gives you a chance to address potential concerns before submitting your application.

How Much ARM Loan Can I Get? Practical Ways to Estimate Your Borrowing Power

One of the most common questions from homebuyers is: how much ARM loan can I get? The answer depends on a combination of your income, debts, credit profile, and the specific ARM program you're applying for.

A general starting point is the 28/36 rule, which suggests that your housing costs should not exceed 28% of your gross monthly income, and your total debt obligations should not exceed 36%. While many lenders today allow DTI ratios up to 43% or slightly higher, staying closer to these traditional thresholds may give you more financial breathing room — especially if your ARM rate adjusts upward later.

Here's a simplified example. If your gross monthly income is $8,000, the 28% front-end limit suggests a maximum housing payment of about $2,240. Using the initial rate of a 5/1 ARM, you could back-calculate the loan amount that produces that payment at your quoted rate and term.

However, a prudent approach is to also run the same calculation at the worst-case adjusted rate. If your budget can support the payment at that higher rate while still meeting the DTI requirement, you're in a much stronger position. If it can't, you may want to consider a lower loan amount or a longer fixed period to give yourself more time before adjustments begin.

Using an online ARM mortgage affordability calculator is one of the most practical ways to run these scenarios quickly. Many lenders and financial websites offer free tools that let you input your rate caps, index, and margin to project payment ranges over time.

●Conclusion

An adjustable-rate mortgage can offer real advantages — especially for buyers who expect to sell or refinance before the fixed period ends, or those entering the market when initial ARM rates are meaningfully lower than fixed-rate alternatives. But the key to using one wisely is preparation. Knowing how to calculate affordability for ARM mortgage financing means looking beyond the first monthly payment and stress-testing your budget against the full range of possible outcomes. Gather your loan details, use a reliable ARM mortgage affordability calculator, check your DTI at both initial and adjusted rates, and review all the qualification factors that may apply to your situation. When you approach an ARM with this level of clarity, you're not just shopping for a rate — you're making a thoughtful, well-informed financial decision. Ready to explore your options? Connect with a LoanWise mortgage specialist to run the numbers together and find the loan structure that fits your goals.