Home Equity Loan Calculator: Your Investment Capital Blueprint

Real estate investors often find themselves sitting on substantial equity in their properties, yet many struggle to effectively calculate and leverage this wealth for their next investment opportunity. A home equity loan calculator becomes an essential tool in your investment arsenal, helping you determine exactly how much capital you can access and at what cost.

Whether you're planning your next fix and flip project or expanding your rental property portfolio, understanding how to calculate home equity loan payments and borrowing capacity can make the difference between missing opportunities and maximizing returns. The key lies not just in knowing your numbers, but in understanding how different loan structures impact your overall investment strategy.

Smart Approaches When Using Home Equity Calculations

Smart approaches when using home equity calculations can significantly impact your investment success and financial planning accuracy. Professional investors typically follow specific best practices when evaluating their equity positions and potential borrowing capacity.

- Calculate based on recent property valuations: Use current market values rather than purchase prices, as property appreciation might have increased your available equity substantially over time.

- Factor in all associated costs: Include closing costs, appraisal fees, and ongoing interest expenses when determining the true cost of accessing your equity capital.

- Consider multiple loan structures: Compare traditional home equity loans against HELOCs to determine which option aligns better with your investment timeline and cash flow needs.

- Account for debt-to-income ratios: Ensure your calculations include existing mortgage payments and rental income when determining qualification parameters for additional financing.

Common Mistakes That Hurt Your Investment Calculations

Common mistakes that hurt your investment calculations often stem from oversimplified assumptions or overlooking key variables that impact your actual borrowing costs and capacity. These errors can lead to unrealistic expectations and poor investment decisions.

- Ignoring variable rate risks: Failing to account for potential rate increases on variable-rate products can dramatically underestimate long-term borrowing costs and impact cash flow projections.

- Overestimating available equity: Using inflated property values or forgetting about existing liens and mortgages can result in disappointment when applying for actual financing.

- Neglecting tax implications: Not considering the tax deductibility differences between home equity loans and other financing options can misrepresent the true cost of capital.

- Skipping stress testing scenarios: Failing to model different interest rate environments or vacancy periods can leave investors vulnerable to cash flow shortfalls.

5 Steps to Estimate Home Equity Loan Borrowing Power

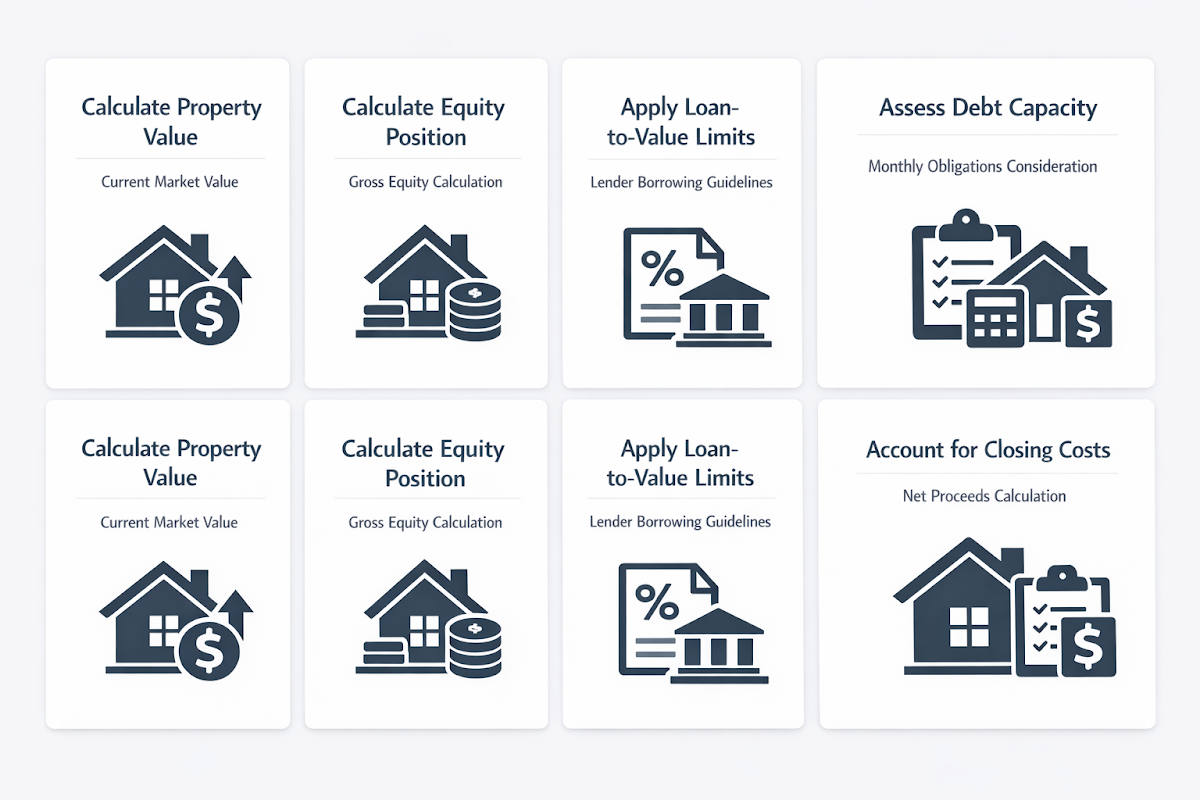

Estimate home equity loan borrowing power by following a systematic approach that considers both your property value and lender requirements. This methodical process helps ensure accurate calculations and realistic expectations for your investment planning.

- Determine current property value: Obtain recent comparable sales data or consider a professional appraisal to establish your property's current market value, as this forms the foundation of your equity calculation.

- Calculate existing equity position: Subtract your remaining mortgage balance from the current property value to determine your gross equity, which represents your ownership stake in the property.

- Apply lender loan-to-value limits: Most lenders typically allow borrowing up to 80-90% of property value minus existing mortgages, though investment properties might face more conservative limits.

- Assess your debt-to-income capacity: Factor in your existing monthly obligations and rental income to determine how much additional debt service you can realistically handle without straining cash flow.

- Account for closing costs and fees: Subtract estimated closing costs, appraisal fees, and other associated expenses from your potential loan amount to determine net proceeds available for investment.

4 Key Factors in Home Equity Loan Interest Rate Calculations

Home equity loan interest rates depend on multiple factors that directly impact your borrowing costs and investment returns. Understanding these variables helps you better prepare for the application process and negotiate favorable terms.

- Credit score and financial history: Higher credit scores typically qualify for lower interest rates, while investment property loans may carry slightly higher rates than owner-occupied properties regardless of credit quality.

- Loan-to-value ratio impact: Lower LTV ratios often result in better interest rates, as lenders view these loans as less risky due to the larger equity cushion protecting their investment.

- Property type and occupancy status: Investment properties and non-owner-occupied homes usually carry higher rates than primary residences, reflecting the increased risk lenders associate with these property types.

- Market conditions and term length: Current interest rate environments and your chosen loan term affect pricing, with longer terms potentially offering rate stability but higher overall interest costs.

3 Ways to Compare HELOC vs Home Equity Loan Options

HELOC vs. home equity loan calculator comparisons reveal significant differences in structure, costs, and flexibility that can impact your investment strategy. Each option serves different investor needs and market scenarios.

- Payment structure and cash flow impact: Home equity loans provide fixed monthly payments that help with budgeting, while HELOCs offer interest-only payments during the draw period, potentially improving short-term cash flow for active investors.

- Interest rate stability and risk exposure: Fixed-rate home equity loans protect against rate increases, whereas variable-rate HELOCs might start lower but carry rate adjustment risks that could affect long-term investment profitability.

- Access flexibility and usage patterns: HELOCs allow multiple draws up to your credit limit, making them ideal for investors pursuing multiple projects, while home equity loans provide lump-sum funding better suited for single large investments.

●Conclusion

Mastering home equity loan calculations empowers real estate investors to make informed decisions about leveraging their property wealth for portfolio growth. The ability to accurately calculate home equity loan payments, compare different loan structures, and estimate borrowing power creates opportunities to capitalize on market conditions and expand investment activities.

Remember that successful investors don't just focus on accessing the maximum amount of equity, but rather on finding the right balance between leverage and risk management. Consider consulting with mortgage professionals who specialize in investment property financing to ensure your calculations align with current market conditions and lender requirements.

Your property equity represents more than just paper wealth - it's potential investment capital waiting to fuel your next successful real estate venture. Use these calculation strategies to unlock that potential while maintaining the financial stability that sustains long-term investment success.