Essential FHA Loan Programs for Real Estate Investors

Real estate investors often overlook FHA Loan Programs when evaluating financing options for their portfolios. While these government-backed mortgages might seem designed primarily for homebuyers, they can offer strategic advantages for certain investment scenarios. With updated loan limits for 2026 reaching $1,249,125 for single-unit properties in high-cost areas, FHA programs present opportunities that savvy investors shouldn't ignore.

Understanding how FHA Loan Programs work within an investment context requires looking beyond traditional assumptions. These loans can serve as stepping stones for new investors or complement existing financing strategies for experienced portfolio builders. The key lies in knowing when and how to leverage their unique benefits while navigating their specific requirements and limitations.

Updated FHA Loan Limits and Investment Opportunities

The updated FHA loan limits for 2026 create significant opportunities for real estate investors, particularly in high-cost markets. With the maximum amount for a one-unit property set at $1,249,125, investors can potentially finance larger properties using FHA loans than previously possible.

- High-cost area advantages: The increased limits allow investors to acquire higher-value properties in competitive markets where appreciation potential may be greater

- Strategic market entry: Investors can use these limits to establish footholds in previously inaccessible premium markets

- Portfolio expansion opportunities: The higher limits facilitate growth into markets with better cash flow potential and long-term appreciation prospects

- Refinancing possibilities: Existing property owners can leverage appreciation by refinancing into FHA programs where beneficial

These limit increases respond directly to rising home prices and help maintain accessibility in the lending market. For investors, this represents government support for continued real estate investment activity, even in challenging market conditions.

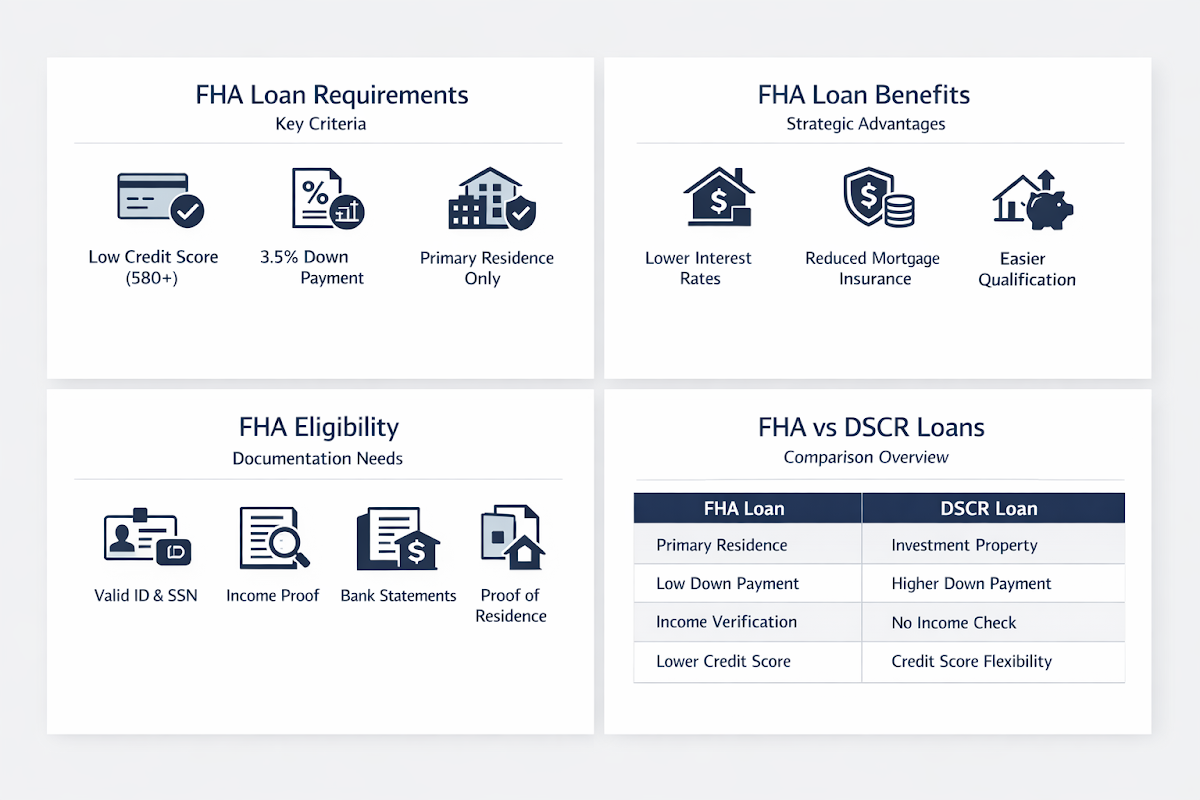

FHA Loan Requirements for Investment Properties

Understanding FHA loan requirements is crucial for investors who want to utilize these programs effectively. The FHA floor typically starts at $541,287, and meeting the program's specific criteria can unlock access to favorable financing terms.

- Owner-occupancy rules: Most FHA loans require the borrower to occupy the property as their primary residence, limiting direct investment applications

- Multi-unit properties: FHA loans can finance up to four-unit properties when the owner occupies one unit, creating house-hacking opportunities

- Credit and income standards: FHA programs often have more flexible credit requirements compared to conventional investment loans

- Down payment benefits: Lower down payment requirements can preserve capital for additional investments or property improvements

While FHA loan requirements may seem restrictive for pure investment purposes, creative investors often find ways to incorporate these programs into their broader strategies, particularly when starting their real estate careers or transitioning between markets.

Strategic Benefits of FHA Programs

FHA loan benefits extend beyond simple financing, offering strategic advantages that complement investment objectives. These government-backed programs provide stability and predictability that can enhance overall portfolio performance.

- Lower barrier to entry: Reduced down payment requirements help new investors enter the market with less initial capital

- Competitive interest rates: FHA loan interest rates are often favorable compared to conventional investment loans

- Assumable loan features: FHA loans can be assumed by qualified buyers, potentially adding value when selling properties

- Portfolio diversification: Including FHA-financed properties can balance higher-risk investment loans with more stable financing

The combination of government backing and investor-friendly terms makes FHA programs valuable tools for building wealth through real estate, particularly when integrated thoughtfully with other financing strategies.

FHA Eligibility and Documentation Requirements

FHA loan eligibility involves specific documentation and qualification standards that investors must understand to leverage these programs effectively. The process typically requires more personal income verification compared to investment-focused loan products.

- Personal income documentation: Unlike DSCR loans that focus on property cash flow, FHA programs require traditional employment and income verification

- Debt-to-income ratios: Borrowers must meet specific DTI requirements that include all existing debt obligations

- Property condition standards: FHA properties must meet specific habitability and safety requirements, potentially requiring repairs before closing

- Primary residence commitment: Borrowers typically must commit to occupying the property as their primary residence for a specified period

These eligibility requirements create both opportunities and constraints for investors, making FHA programs most suitable for specific scenarios rather than general investment purposes.

Comparing FHA Programs with DSCR Loan Options

When evaluating financing options, investors should understand how FHA programs compare with DSCR loan alternatives. Each loan type serves different strategic purposes within a comprehensive investment approach.

- Income verification approach: DSCR loans focus on property cash flow rather than personal income, while FHA programs require traditional employment documentation and personal financial qualification

- Property use flexibility: DSCR loans typically allow for pure investment properties without occupancy requirements, whereas FHA programs generally require owner occupancy

- Down payment structures: FHA programs may offer lower down payment options, while DSCR loans typically require higher initial investments but provide more flexible terms

- Interest rate considerations: FHA loan interest rates might be more competitive for qualified borrowers, while DSCR rates reflect the higher risk of investment lending

Understanding these differences helps investors choose the right financing tool for each situation, potentially using both types of loans within a diversified portfolio strategy.

Market Trends and Future Considerations

The evolving lending landscape presents both opportunities and challenges for investors considering FHA programs alongside other financing options. Recent market developments suggest continued innovation in investment lending products.

- DSCR lending evolution: Product innovations and hybrid loan structures are reshaping rental property financing, potentially offering more competitive alternatives to traditional programs

- Credit market dynamics: Institutional capital infusion into lending markets may create new opportunities while maintaining program accessibility

- Regulatory environment: Government support through programs like FHA continues to demonstrate commitment to housing market stability and investor participation

- Integration strategies: Successful investors increasingly combine multiple loan types, using FHA programs for specific situations while relying on DSCR loans for pure investment plays

Staying informed about these trends helps investors adapt their strategies and capitalize on emerging opportunities while maintaining financing flexibility across changing market conditions.

●Conclusion

FHA Loan Programs represent a valuable component of comprehensive real estate investment financing strategies, particularly when used strategically rather than as primary investment tools. The updated 2026 loan limits create new opportunities in high-cost markets, while the programs' inherent benefits can complement other financing options like DSCR loans.

Success with FHA programs requires understanding their specific requirements, benefits, and limitations within the context of broader investment objectives. While these loans may not suit every investment scenario, they can provide strategic advantages for new investors, multi-unit property acquisitions, and portfolio diversification efforts.

As the lending landscape continues to evolve, investors who maintain awareness of all available financing options, including FHA programs, position themselves to capitalize on opportunities and navigate market changes more effectively. The key lies in matching the right financing tool to each investment opportunity while building a sustainable, profitable real estate portfolio.