Business Loan for Payroll Taxes: Strategic Financing for Real Estate Investors

Real estate investment businesses often face unique cash flow challenges, particularly when managing payroll obligations across multiple properties and renovation projects. A business loan for payroll taxes might provide the temporary financial bridge needed to maintain operations while preserving capital for investment opportunities. Understanding payroll tax financing options becomes crucial when your rental income is tied up in property improvements or when seasonal fluctuations impact your cash flow.

For investors managing fix and flip projects, rental portfolios, or construction crews, payroll tax obligations don't pause for market conditions or project delays. This comprehensive guide explores how paying payroll taxes with a loan could fit into your investment strategy, along with the tax implications of business loans and practical approaches to managing payroll tax debt without compromising your real estate ventures.

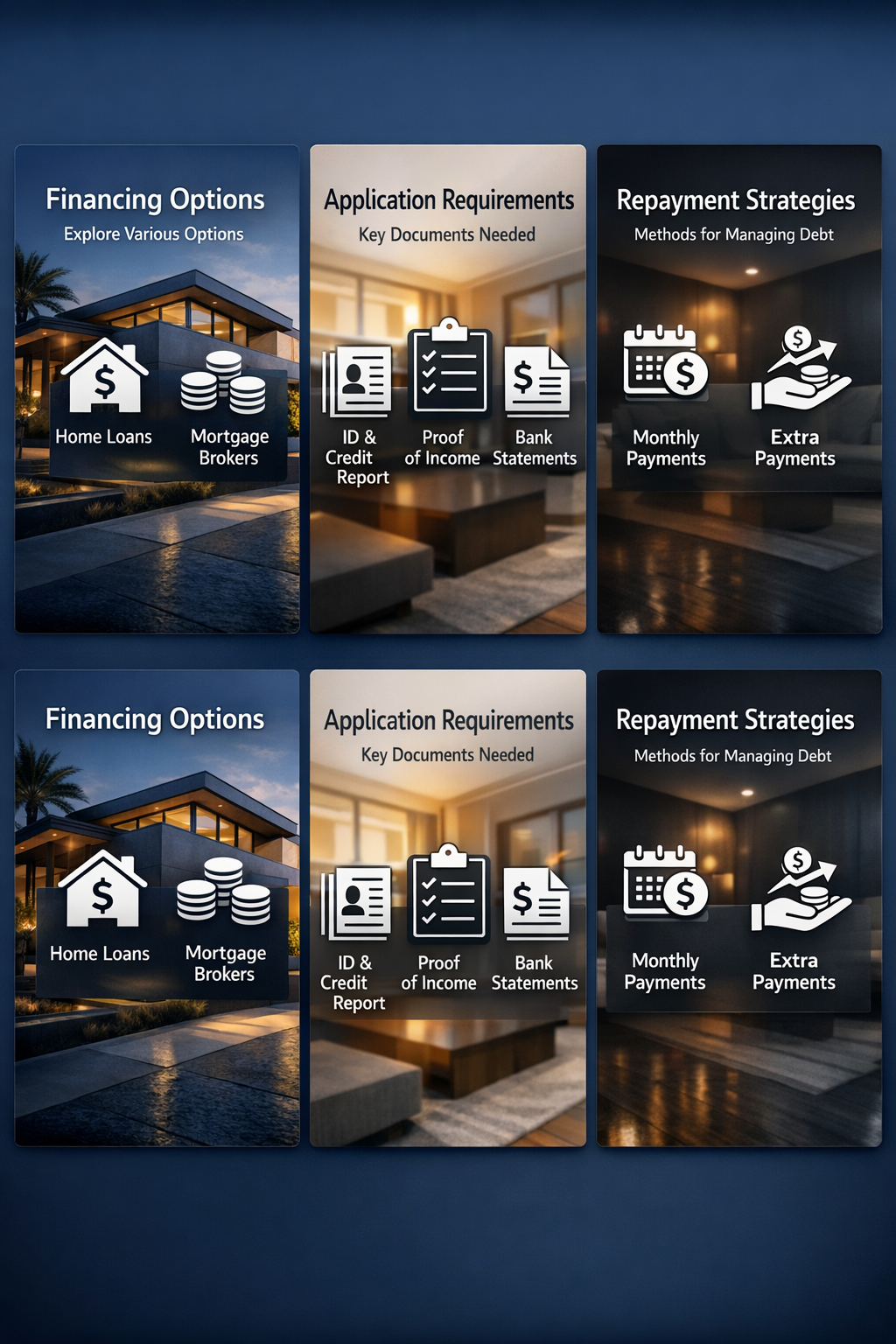

Essential Payroll Tax Financing Options

Essential payroll tax financing options for real estate investors typically involve several strategic approaches that might help maintain business operations during cash flow gaps. These financing solutions could provide the flexibility needed when rental income or project revenues are temporarily delayed.

- Business lines of credit: May offer revolving access to funds for ongoing payroll obligations, allowing you to draw only what's needed for tax payments while maintaining cash reserves for property investments

- Short-term business loans: Could provide lump-sum financing to cover immediate payroll tax liabilities, often with faster approval processes than traditional commercial loans

- Asset-based lending: Might leverage your real estate portfolio as collateral for payroll tax financing, potentially offering better rates due to the secured nature of the loan

- Invoice factoring for contractors: May help if your business involves contracting work, converting pending payments into immediate cash for payroll tax obligations

Critical Loan Application Requirements

Critical loan application requirements for payroll tax financing often vary among lenders, but real estate investors should typically prepare specific documentation that demonstrates both business viability and repayment capacity.

- Financial statements and tax returns: Usually includes the last two years of business and personal tax returns, plus current profit and loss statements from your real estate operations

- Cash flow projections: May require detailed forecasts showing rental income, project completion schedules, and expected revenue streams that support loan repayment

- Property portfolio documentation: Could include property deeds, rental agreements, and current market valuations that demonstrate your business's asset base and income potential

Tax Compliance Documentation Checklist

Tax compliance documentation checklist becomes essential when applying for payroll tax financing, as lenders typically want to understand your current tax situation and compliance history before approving funding.

- Recent payroll tax filings: Should include Forms 941, 940, and state payroll tax returns to demonstrate your filing history and current obligations

- IRS payment agreements or notices: Must disclose any existing payment plans, liens, or correspondence with tax authorities that might affect loan approval

- Payroll processing records: May include recent payroll registers, employee records, and proof of current payroll tax deposits to show ongoing compliance efforts

- Business registration documents: Could require current business licenses, EIN documentation, and state registration certificates that verify your legal business status

Step-by-Step Loan Application Process

The step-by-step loan application process for payroll tax financing typically follows a structured approach that real estate investors should understand to expedite approval and secure favorable terms.

- Initial financial assessment: Begin by calculating your exact payroll tax liability and determining the precise loan amount needed, including any penalties or interest that might accrue during the application process

- Lender research and comparison: Research multiple lenders who specialize in business financing for real estate investors, comparing interest rates, terms, and approval requirements specific to payroll tax loans

- Documentation preparation and submission: Compile all required financial documents, tax records, and business information before submitting applications to avoid delays in the approval process

- Application review and approval: Work closely with lenders during the underwriting process, providing additional information as requested and maintaining open communication about your real estate business operations

Strategic Repayment Planning Methods

Strategic repayment planning methods for payroll tax loans require careful consideration of your real estate investment cash flow cycles and project timelines to ensure sustainable debt management.

- Rental income allocation strategy: Structure loan payments to align with monthly rental collections, potentially setting aside a specific percentage of rental income specifically for loan repayment and future payroll tax obligations

- Project-based repayment scheduling: Time loan repayments with anticipated property sales or refinancing events, particularly useful for fix and flip investors who can predict project completion and sale proceeds

- Seasonal cash flow management: Plan repayment schedules around seasonal variations in your real estate business, such as higher rental demand in certain months or construction season limitations

Managing Ongoing Tax Obligations

Managing ongoing tax obligations while servicing payroll tax debt requires systematic approaches that prevent future cash flow challenges and maintain compliance with federal and state requirements.

- Automated tax reserve systems: Establish separate business accounts that automatically set aside payroll tax funds from each paycheck processed, ensuring future obligations are covered regardless of cash flow variations

- Quarterly payment planning: Implement quarterly review processes that assess your payroll tax liability against available cash reserves, allowing for proactive adjustments to payment schedules or additional financing if needed

- Professional tax advisory services: Engage qualified tax professionals who understand real estate investment businesses to ensure ongoing compliance and strategic planning for future payroll tax obligations

Key Takeaways for Real Estate Investors

A business loan for payroll taxes might serve as a valuable financial tool for real estate investors, but success depends on careful planning and realistic assessment of repayment capacity. The tax implications of business loans used for payroll tax payments could vary depending on your specific situation and business structure, making professional tax advice essential before proceeding with financing.

Managing payroll tax debt through strategic borrowing requires understanding that this approach typically works best as a short-term solution while you address underlying cash flow issues in your real estate business. Consider how loan payments will affect your ability to pursue new investment opportunities and maintain adequate reserves for property maintenance and improvements.

●Conclusion

Navigating payroll tax financing as a real estate investor requires balancing immediate business needs with long-term investment goals. While paying payroll taxes with a loan might provide necessary breathing room during cash flow challenges, sustainable success depends on implementing systems that prevent future tax payment crises. Consider how these financing strategies align with your overall investment portfolio management and growth plans.

Whether you're managing a fix and flip operation, rental property portfolio, or construction business, maintaining proper payroll tax compliance protects your ability to access future financing for real estate opportunities. The key lies in viewing payroll tax loans as temporary bridges rather than permanent solutions, while building robust cash flow management systems that support both your tax obligations and investment ambitions.