Essential Business Loan Eligibility Criteria for Real Estate Investors

Understanding business loan eligibility criteria can make the difference between securing favorable financing for your next investment property or missing out on lucrative opportunities. As the real estate investment landscape evolves in 2026, lenders are refining their qualification standards, particularly for DSCR loans and rental property financing. With current DSCR loan rates ranging from 5.875% to 8.75%, according to recent market data, investors who understand these criteria can position themselves for success in today's competitive lending environment.

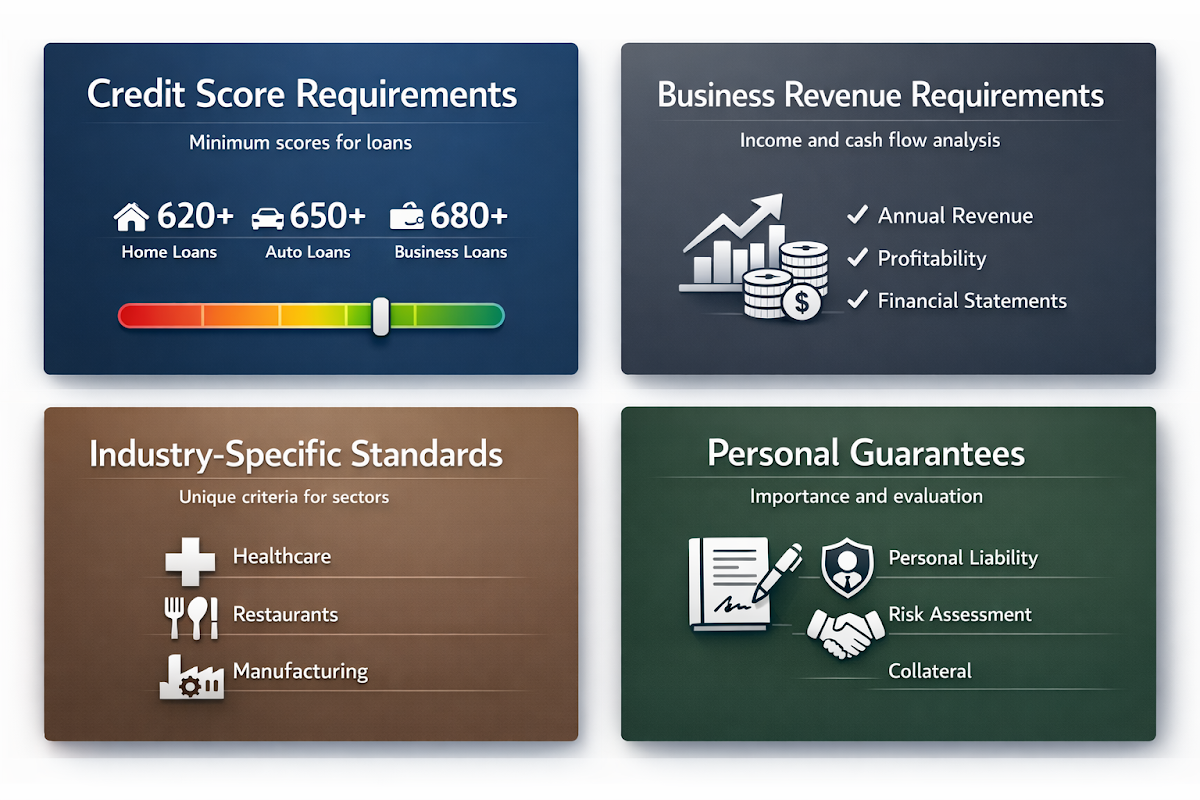

Core Credit Score Requirements for Business Loans

Credit score requirements for business loans vary significantly based on the type of investment financing you're seeking. Understanding these benchmarks helps you prepare your application strategically.

- DSCR loans typically require minimum credit scores of 620-680, though some lenders may accept scores as low as 600 with compensating factors like higher down payments

- Fix and flip financing often demands higher scores of 680-720 due to the short-term, higher-risk nature of these projects

- Portfolio lenders may offer more flexibility for investors with multiple properties and strong cash flow history, sometimes accepting scores in the 580-620 range

- Commercial real estate loans generally require scores above 700 for optimal terms and competitive interest rates

Business Revenue Requirements and Cash Flow Analysis

Business revenue requirements form the backbone of loan qualification, particularly for rental property investors who rely on consistent income streams.

- DSCR calculations require rental income to exceed debt payments by at least 1.25 times, though some lenders accept ratios as low as 1.0 with sufficient reserves

- Two years of rental income documentation is typically required, including lease agreements and bank statements showing consistent deposits

- Vacancy allowances of 5-10% are factored into income calculations, so your properties need to generate sufficient cash flow above this threshold

- Multiple property portfolios strengthen your position by demonstrating diversified income sources and management experience

Industry-Specific Loan Eligibility Standards

Industry-specific loan eligibility varies considerably across different real estate investment sectors, with lenders applying unique criteria based on property type and investment strategy.

- Residential rental properties typically offer the most flexible terms with standard DSCR requirements and conventional down payment options starting at 20-25%

- Commercial properties require higher down payments of 25-35% and more comprehensive financial documentation including profit and loss statements

- Short-term rental properties face stricter scrutiny with some lenders requiring additional cash reserves due to income volatility

- Mixed-use properties combine residential and commercial underwriting standards, often requiring separate analysis for each component

Essential Documentation Steps for Loan Approval

Proper documentation significantly improves your chances of loan approval and can expedite the underwriting process.

- Compile comprehensive financial statements including two years of tax returns, profit and loss statements, and current balance sheets to demonstrate your financial stability and business performance

- Gather property documentation such as lease agreements, rent rolls, and recent appraisals to support your income projections and property values

- Prepare cash flow projections and market analysis showing realistic rental income expectations and local market conditions that support your investment thesis

- Organize entity documentation including business licenses, operating agreements, and insurance policies to establish proper business structure and risk management

Personal Guarantees for Business Loans Requirements

Personal guarantees for business loans remain a critical component of most investment property financing, though requirements vary by loan type and borrower strength.

- Evaluate your personal credit profile separately from business credit since lenders typically require personal guarantees for loans under $1 million, making your individual creditworthiness crucial

- Understand limited versus unlimited guarantee structures where some lenders offer limited guarantees capped at specific dollar amounts or percentages of the loan balance

- Consider entity structuring strategies that may reduce personal exposure while maintaining qualification for preferred loan programs, though this requires careful legal and tax planning

- Negotiate guarantee terms during the application process as experienced investors with strong portfolios may secure more favorable personal guarantee conditions

●Conclusion

Mastering business loan eligibility criteria positions you to capitalize on today's evolving investment opportunities. With DSCR loan demand continuing to rise and lenders competing for qualified borrowers, understanding these requirements helps you structure deals that meet underwriting standards while maximizing your returns. Focus on maintaining strong credit profiles, documenting consistent cash flows, and building relationships with lenders who understand real estate investment strategies. As market conditions shift, investors who stay informed about eligibility criteria and adapt their approach accordingly will find the best financing solutions for their portfolios.