For veterans, active-duty service members, and eligible surviving spouses, the VA home loan benefit is one of the most valuable financial tools available. At the heart of this benefit is a concept called VA loan entitlement — a figure that determines how much the Department of Veterans Affairs will guarantee on your behalf. Understanding how entitlement works could be the key to buying or refinancing a home with no down payment and no private mortgage insurance. Whether you're a first-time homebuyer using your benefit for the first time or a veteran looking to purchase again, this guide breaks down everything you need to know.

What VA Loan Entitlement Actually Means

VA loan entitlement isn't a dollar amount you receive directly. Instead, it's the portion of your loan that the VA promises to repay your lender if you default. This guarantee is what allows VA-approved lenders to offer favorable terms — including no down payment requirements on qualifying loans — to eligible borrowers.

There are two layers to VA loan entitlement: basic entitlement and bonus entitlement (sometimes called second-tier or additional entitlement). Together, they work to support your purchasing power depending on your location and the loan amount you need.

- Basic entitlement is typically set at $36,000, which covers loans up to a certain threshold.

- Bonus entitlement kicks in for higher loan amounts and is tied to the conforming loan limits set by the Federal Housing Finance Agency (FHFA) each year.

It's worth noting that since the Blue Water Navy Vietnam Veterans Act of 2020, eligible veterans with full entitlement no longer face a loan limit imposed by the VA. That means if you have full entitlement remaining, you may be able to borrow as much as a lender will approve — without a down payment — regardless of the home's purchase price.

Full Entitlement vs. Reduced Entitlement: Knowing the Difference

Your entitlement status plays a major role in what loan terms you can access. Here's how each scenario typically works:

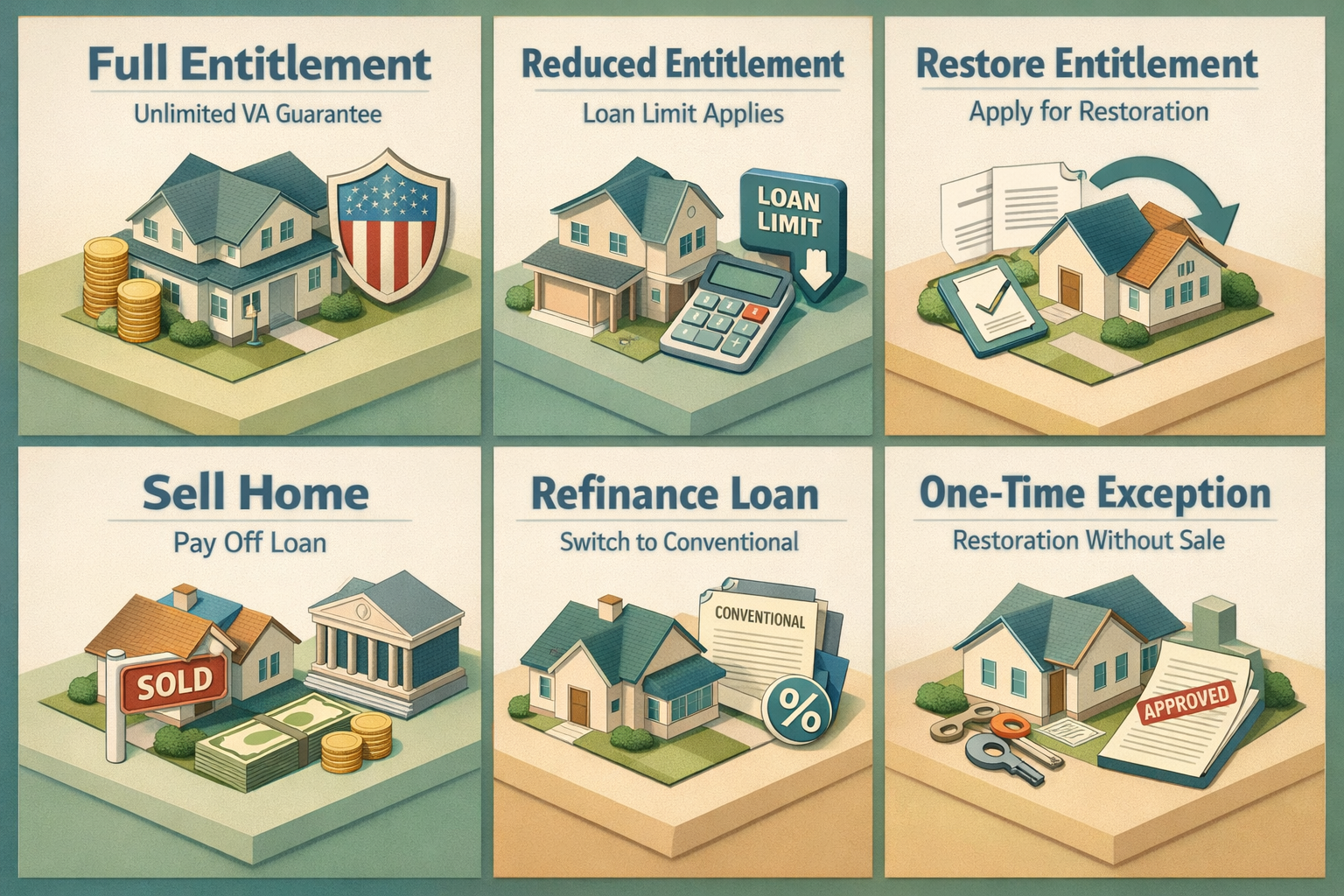

Full Entitlement

You have full VA loan entitlement if you've never used your VA home loan benefit before, or if you've paid off a previous VA loan and had that entitlement restored. With full entitlement, the VA's guarantee is unlimited in practice — meaning no VA-imposed loan cap and potentially no down payment required, subject to lender approval and creditworthiness.

Reduced (Remaining) Entitlement

If you currently have an active VA loan or previously used your entitlement without fully restoring it, you may have reduced entitlement. In this case, a loan limit based on the county's conforming loan limit may apply, and you might need to make a down payment on amounts above the limit your entitlement can cover.

Veterans in this situation can still use their remaining entitlement to purchase a second home or investment property — but the math becomes more nuanced. A knowledgeable VA-approved lender can help you calculate how much of your entitlement remains and what your options are.

How to Check and Restore Your VA Entitlement

Your Certificate of Eligibility (COE) is the official document that shows lenders your entitlement status and confirms your eligibility for a VA loan. You can request your COE through the VA's eBenefits portal, by working directly with a VA-approved lender, or by submitting VA Form 26-1880 by mail.

If you've previously used your VA benefit and want to restore your full entitlement, there are a few pathways available:

- Sell the home and repay the loan: Once the VA-backed loan is paid off and the property is sold, you can apply to have your entitlement restored.

- Refinance into a non-VA loan: Paying off the VA loan by refinancing into a conventional loan and then selling the property may also restore your entitlement.

- One-time restoration exception: In some cases, veterans may qualify for a one-time restoration even if they haven't sold the property, provided the loan is fully paid off.

It's important to formally apply for restoration rather than assuming it happens automatically. Processing times can vary, so it's wise to plan ahead if you're considering a future purchase.

Using VA Entitlement to Buy Again or Own Multiple Properties

One of the most misunderstood aspects of the VA loan program is that you can use it more than once. Veterans who have remaining entitlement — even if it's only partial — may be able to purchase a second property using a VA loan. This is sometimes called a bonus entitlement loan or second-tier entitlement.

For example, suppose you purchased a home using your basic entitlement and still have that VA loan active. If you need to relocate — say, due to military orders — you might be able to use your remaining bonus entitlement to purchase a new primary residence. In most cases, VA loans are intended for owner-occupied primary residences, though there are exceptions for certain service-related relocations.

Real estate investors should be aware that using VA loans for pure investment properties isn't typically permitted under VA guidelines. However, eligible buyers who occupy one unit of a multi-unit property (up to four units) may use VA financing, potentially allowing rental income from other units to help qualify. This can be a smart strategy for veterans looking to build long-term wealth through real estate.

The VA Funding Fee and How Entitlement Affects Your Costs

While VA loans don't require private mortgage insurance (PMI), they do come with a VA funding fee — a one-time charge that helps sustain the program for future generations of veterans. The amount you pay depends on several factors, including:

- Whether it's your first time using a VA loan or a subsequent use

- Your down payment amount (if any)

- Your military service category (regular military, National Guard, or Reserves)

First-time users who make no down payment typically pay a lower funding fee than those using the benefit a second or third time. Putting even a small down payment — such as 5% or more — can reduce the fee further. Some veterans are exempt from the funding fee entirely, including those receiving VA disability compensation and surviving spouses of veterans who died in service or from service-connected disabilities.

It's worth calculating how the funding fee fits into your overall loan costs. In many cases, even with the fee factored in, VA loans can be a more cost-effective option than conventional financing — especially when you consider the absence of PMI and the competitive interest rates often associated with VA-backed loans.

Common Mistakes Veterans Make With Their VA Loan Benefit

Even well-informed veterans can stumble when navigating VA loan entitlement. Here are some common missteps to watch out for:

- Assuming entitlement is automatically restored: Entitlement doesn't reset without a formal request. Many veterans don't realize they need to apply for restoration after paying off a previous VA loan.

- Not shopping around for VA lenders: The VA sets guidelines, but individual lenders set their own rates, fees, and credit requirements. Comparing multiple VA-approved lenders could save you thousands over the life of your loan.

- Overlooking the COE process: Some buyers wait until they're under contract to request their COE, which can delay closing. Getting it early keeps the process moving smoothly.

- Misunderstanding occupancy requirements: VA loans require the borrower to occupy the home as their primary residence, typically within 60 days of closing. Failing to meet this requirement could create compliance issues.

- Ignoring refinance opportunities: Veterans with existing VA loans may benefit from an Interest Rate Reduction Refinance Loan (IRRRL), which can streamline the process of lowering your rate with minimal documentation.

●Conclusion

VA loan entitlement is one of the most powerful housing benefits available to those who've served our country — but only if you understand how to use it effectively. From checking your Certificate of Eligibility to exploring bonus entitlement for a second purchase, taking the time to learn the details could save you significant money and open doors to homeownership that might otherwise seem out of reach. If you're ready to explore your VA loan options or want to find out how much entitlement you have remaining, connecting with a VA-approved lender is your best next step. At LoanWise, we're here to help veterans and eligible borrowers navigate the process with confidence.