If you're carrying student loan debt and dreaming of homeownership, you're not alone. Millions of Americans are navigating the same challenge — balancing monthly loan payments while trying to save for a down payment and qualify for a mortgage. The good news is that student loan debt doesn't automatically disqualify you from getting a home loan. Lenders look at the full picture of your financial profile, and with the right strategy, qualifying for a mortgage with student loan debt is absolutely within reach. This guide walks you through what lenders consider, how your debt impacts your borrowing power, and the practical steps you can take to strengthen your application.

Why Student Loan Debt Matters to Mortgage Lenders

When you apply for a mortgage, lenders aren't just looking at your income or credit score in isolation. One of the most important calculations they run is your debt-to-income ratio, commonly referred to as DTI. This ratio compares your total monthly debt obligations to your gross monthly income. Student loan payments are counted as part of that debt load — and depending on the size of your balance, they can meaningfully affect how much home you're eligible to finance.

Most conventional loan programs prefer a DTI ratio at or below 43%, though some lenders may have more flexibility depending on other compensating factors like strong credit or a larger down payment. If your student loan payments push your DTI above acceptable thresholds, a lender may reduce your approved loan amount or, in some cases, decline the application altogether.

It's worth noting that lenders calculate your student loan obligation differently depending on the loan program and your current repayment status. For example, if your loans are in deferment or on an income-driven repayment plan, some loan programs may use a percentage of your total loan balance as an estimated monthly payment rather than your actual payment. This can sometimes make your DTI appear higher than your real monthly budget reflects — so understanding how each program treats deferred or reduced payments is an important part of the mortgage planning process.

How Different Loan Programs Handle Student Debt

Not all mortgage programs calculate student loan debt the same way, and this distinction could make a real difference in which loan product works best for you.

- Conventional loans typically require lenders to use the actual monthly payment listed on your credit report. If your payment is $0 due to an income-driven repayment plan, some lenders may still apply a calculated payment — often around 1% of your outstanding balance per month.

- FHA loans have historically used 1% of the total student loan balance as the monthly payment when calculating DTI, even if your actual payment is lower. However, updated guidelines have moved toward using the actual payment in some cases, so it's worth confirming current rules with your lender.

- VA loans, available to eligible veterans and service members, may offer more favorable treatment for student loan debt, particularly when payments are deferred for 12 months or more beyond the closing date.

- USDA loans for rural home purchases also have specific guidelines that may differ from conventional and FHA programs.

Because these guidelines can shift over time and vary by lender, it's a smart move to speak with a knowledgeable mortgage professional who can walk you through which program might be most advantageous for your specific situation.

Calculating Your Debt-to-Income Ratio Before You Apply

Before you submit a mortgage application, it's helpful to run your own DTI estimate so you have a realistic sense of your borrowing power. Here's a simplified approach:

- Add up all your monthly debt payments: student loans, car loans, credit card minimums, personal loans, and any other recurring obligations.

- Divide that total by your gross monthly income (before taxes).

- Multiply the result by 100 to get a percentage.

For example, if your total monthly debts come to $1,200 and your gross monthly income is $5,000, your DTI is 24%. That's generally considered healthy. But if your student loan payment is $600 per month and that same DTI calculation pushes you to 36% before adding the estimated mortgage payment, you'll want to understand how much additional debt a lender will allow before your application gets complicated.

Keep in mind that your front-end DTI — which only includes housing costs — and your back-end DTI — which includes all debts — are both evaluated. Most lenders focus heavily on the back-end ratio when student loans are part of the picture. Running these numbers ahead of time helps you set a realistic home purchase budget and identify areas to improve before applying.

Strategies to Improve Your Mortgage Eligibility

If your DTI is higher than you'd like, or if you're worried that your student loan debt might limit your options, there are several practical strategies that could help you strengthen your application.

Switch to an Income-Driven Repayment Plan

If your actual student loan payment is lower than what a lender would calculate using a percentage-based method, getting on an income-driven repayment plan and documenting your real payment may help reduce your effective DTI — depending on the loan program. Confirm this approach with your lender before assuming it applies to your situation.

Pay Down High-Interest Revolving Debt

Credit card balances and other revolving debts can carry significant weight in your DTI calculation. Paying those down before applying for a mortgage could free up room in your debt-to-income ratio, even if you're not aggressively reducing your student loan balance.

Increase Your Income

A higher gross income directly improves your DTI. If you've recently received a raise, taken on a side income stream, or are considering a job change, lenders typically want to see stable, documented income — so timing matters here.

Save for a Larger Down Payment

A larger down payment reduces your loan amount, which may help your DTI stay within acceptable limits. It can also unlock better interest rates and eliminate the need for private mortgage insurance on some loan types.

Work With a Co-Borrower

Adding a co-borrower — such as a spouse or family member — who has income and a solid credit profile could help balance out the DTI calculation and improve your overall application strength.

The Role of Credit Score When You Have Student Loan Debt

Your credit score plays an equally important role in qualifying for a mortgage with student loan debt. Even if your DTI is manageable, a lower credit score can result in higher interest rates or stricter lending requirements. The good news is that consistently paying your student loans on time may actually help build a positive payment history — which is one of the most influential factors in your credit score.

On the flip side, missed or late student loan payments can leave a lasting mark on your credit report and make mortgage approval more difficult. If you've had payment issues in the past, it may be worth spending several months re-establishing a clean payment record before applying for a home loan.

Most conventional loan programs typically require a minimum credit score in the mid-600s, though specific thresholds vary by lender and program. FHA loans may allow for lower scores, making them potentially more accessible for borrowers who are still rebuilding credit. VA and USDA programs each have their own benchmarks as well. Talking to a mortgage advisor early in the process can help you understand exactly where you stand and what score you might want to target before applying.

How to Qualify for a Mortgage With Student Loan Debt: Real Steps to Take Today

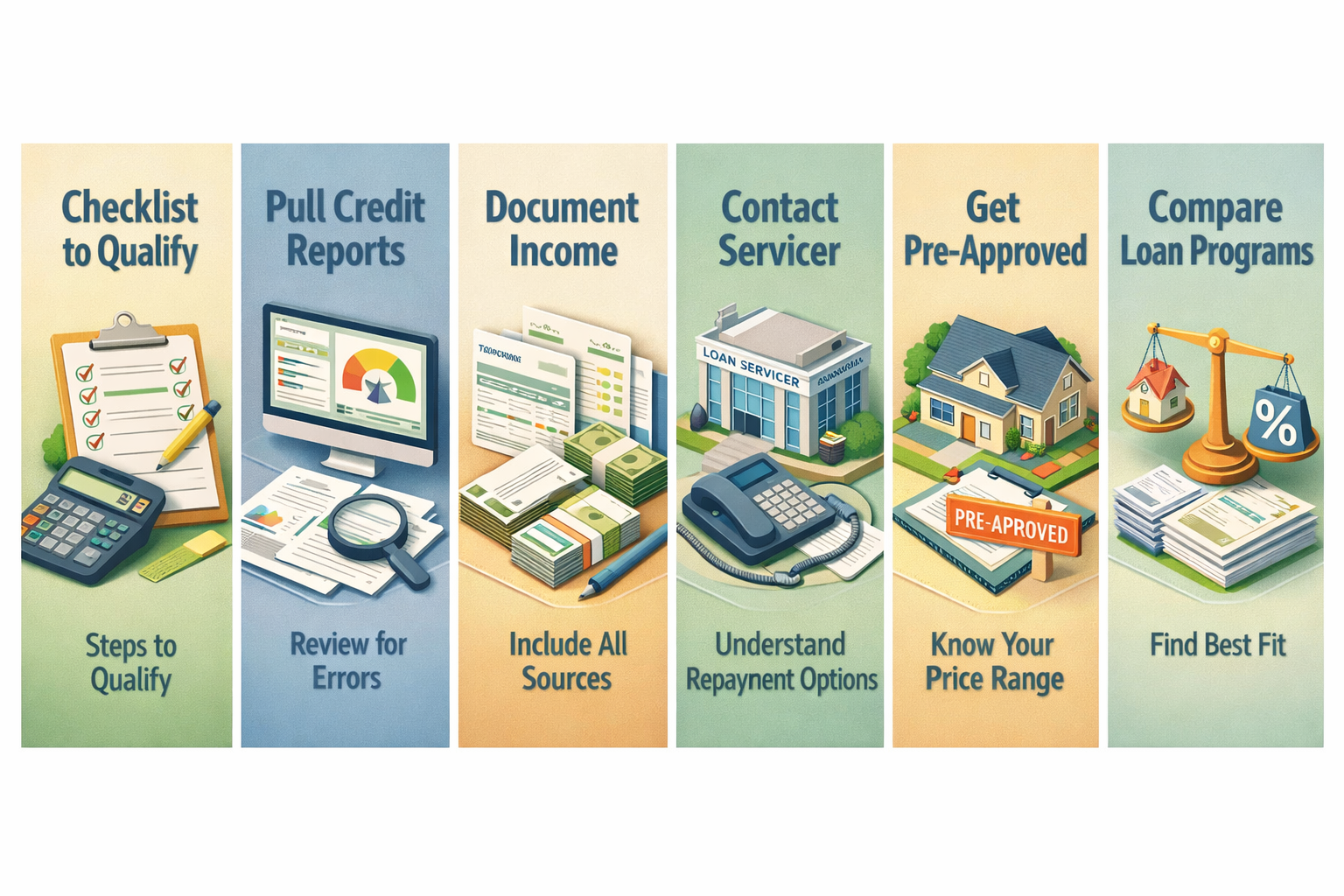

Understanding the theory is one thing — but taking action is what actually moves the needle. Here's a practical checklist to help you get mortgage-ready even while managing student loan obligations:

- Pull your credit reports from all three bureaus and review them for errors or outdated information that might be dragging down your score.

- Document your income thoroughly — including any secondary income sources like freelance work, rental income, or bonuses that can be verified with tax returns or bank statements.

- Contact your student loan servicer to understand your repayment options and get written documentation of your current monthly payment amount.

- Get pre-approved early to understand your realistic purchase price range and identify any application weaknesses before you're under contract on a property.

- Compare loan programs — conventional, FHA, VA, and USDA — to see which treats your student debt most favorably based on your specific balance and repayment status.

- Work with an experienced mortgage professional who has helped borrowers in similar situations navigate student debt and the homebuying process.

Taking these steps well in advance of your target purchase date gives you the best chance of walking into the buying a home process prepared, informed, and positioned for approval.

●Conclusion

Student loan debt is a real obstacle for many hopeful homebuyers — but it's rarely an insurmountable one. By understanding how lenders evaluate your debt, knowing which loan programs may be more flexible, and taking deliberate steps to strengthen your financial profile, you can absolutely move toward homeownership even while carrying education-related debt. The key is preparation, clarity, and working with professionals who can help you navigate the process confidently. At LoanWise, we're here to help you explore your mortgage options and find a path that works for your unique situation — student loans and all.