One of the biggest misconceptions in home financing is that you need a large down payment to qualify for a conventional mortgage. The truth is, many homebuyers today are purchasing homes with as little as 3% down through conventional loan programs. If you've been saving diligently but haven't quite reached that 20% milestone, you're not alone — and you may not need to wait. Understanding how to get a conventional loan with low down payment requirements could be the key that unlocks your path to homeownership sooner than you think. This guide walks you through everything you need to know, from eligibility requirements to private mortgage insurance, so you can move forward with confidence.

What Is a Conventional Loan and Why Does It Matter

A conventional loan is a mortgage that isn't backed by a government agency like the FHA, VA, or USDA. Instead, these loans are typically sold to or guaranteed by Fannie Mae or Freddie Mac, the two government-sponsored enterprises that set the guidelines most lenders follow. Because they aren't government-insured, conventional loans often come with stricter credit requirements — but they also offer a wider range of loan structures and can be more cost-effective in the long run for well-qualified borrowers.

Conventional loans are available for primary residences, second homes, and investment properties, making them one of the most versatile mortgage products on the market. They can be used for purchases and refinances alike, and they're available in both fixed-rate and adjustable-rate formats. For homebuyers who meet the credit and income requirements, conventional financing can offer competitive rates and more flexibility than government-backed alternatives.

What makes conventional loans especially appealing right now is that low down payment options have expanded significantly over the past decade. Programs that once required 5% or 10% down have evolved to allow conventional mortgage options 3% down, opening the door for first-time buyers and repeat buyers who prefer to preserve their savings.

Exploring 97% LTV Conventional Loan Programs

A 97% loan-to-value (LTV) ratio means you're borrowing 97% of the home's purchase price and putting down just 3%. Both Fannie Mae and Freddie Mac offer programs specifically designed for this scenario. Fannie Mae's HomeReady and standard 97% LTV programs, along with Freddie Mac's Home Possible and HomeOne products, are among the most commonly used options for low down payment conventional financing.

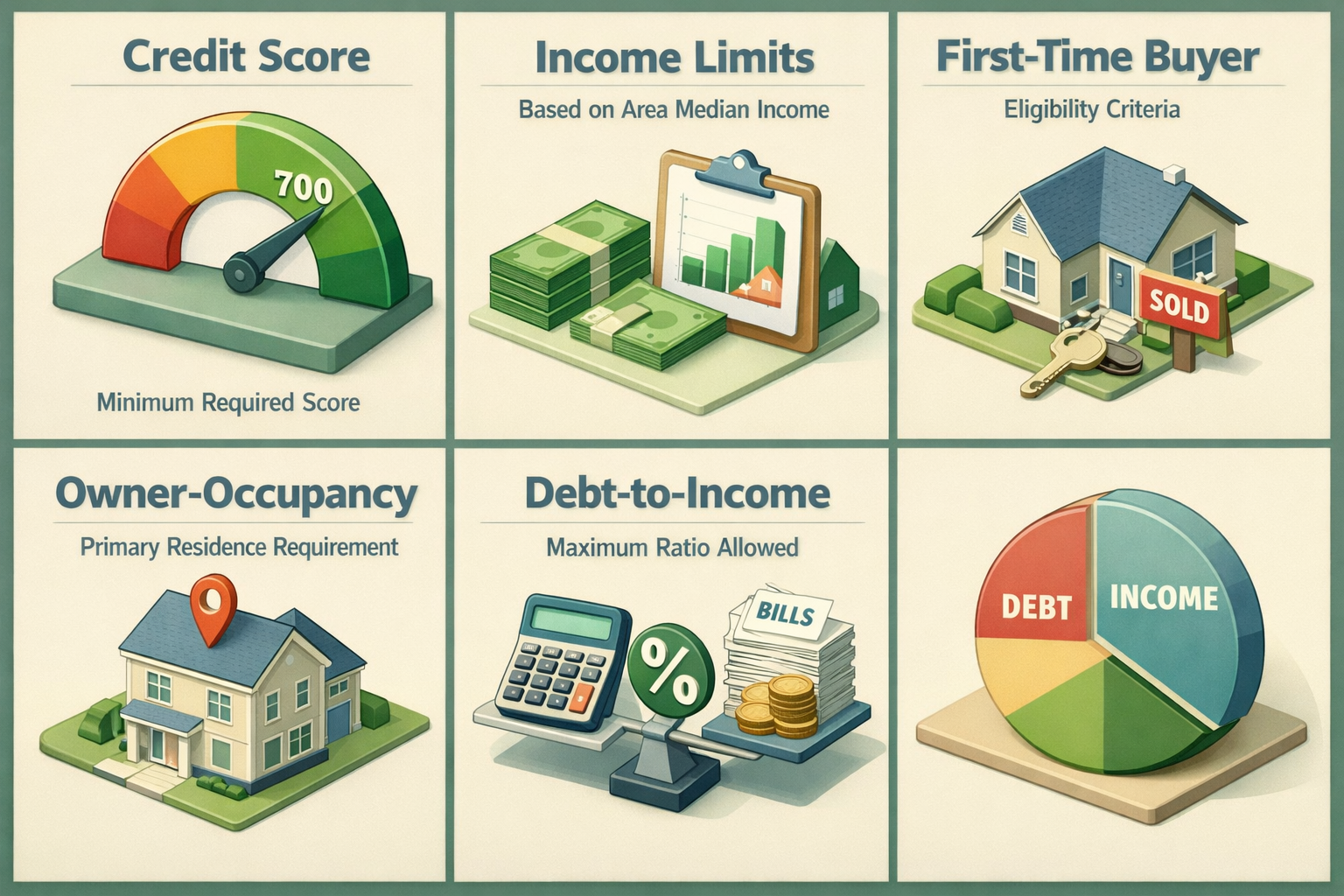

The requirements for 97% LTV conventional loan eligibility typically include the following:

- Credit score: Most lenders require a minimum credit score of 620 for a standard conventional loan. Some 97% LTV programs may require a score of 640 or higher, though this can vary by lender.

- Income limits: Programs like HomeReady and Home Possible have income limits based on area median income (AMI), often capping eligibility at 80% of AMI. However, Freddie Mac's HomeOne and Fannie Mae's standard 97% program do not carry income restrictions for first-time buyers.

- First-time homebuyer status: Some programs are reserved for first-time buyers, typically defined as someone who hasn't owned a home in the past three years. Others allow repeat buyers as well.

- Owner-occupancy: These programs generally require the property to be your primary residence.

- Debt-to-income ratio (DTI): Lenders typically look for a DTI of 45% or lower, though some programs may allow up to 50% with strong compensating factors.

It's worth noting that the specific requirements can vary between lenders, even within the same program. Shopping around and comparing offers may help you find a lender whose guidelines best match your financial profile.

Understanding Private Mortgage Insurance on Conventional Loans

When you put less than 20% down on a conventional loan, you'll typically be required to carry private mortgage insurance, or PMI. This is one of the most important cost factors to understand before committing to a low down payment strategy. PMI protects the lender — not you — in the event you default on the loan, and it adds to your monthly payment.

The cost of private mortgage insurance on a conventional loan is typically expressed as a percentage of your loan amount and can vary based on your credit score, down payment, and loan term. Generally, borrowers with stronger credit scores and larger down payments pay lower PMI rates. While specific rates vary, PMI often ranges from a fraction of a percent to over 1% of the loan balance annually, which can translate to a meaningful monthly cost on a mid-sized mortgage.

Here's what makes conventional PMI stand out compared to FHA mortgage insurance:

- Cancellable coverage: Once your loan balance drops to 80% of the home's original value, you can request PMI cancellation. By law, lenders must automatically terminate PMI when the balance reaches 78% — something FHA loans don't offer in most cases.

- No upfront premium: Unlike FHA loans, conventional PMI typically doesn't require an upfront mortgage insurance premium at closing, which may reduce your out-of-pocket costs on day one.

- Flexible structures: Some borrowers choose lender-paid PMI, where the lender covers the insurance cost in exchange for a slightly higher interest rate. Others prefer single-premium or split-premium structures depending on their financial goals.

Understanding how PMI works helps you plan for the true cost of a low down payment mortgage and evaluate when it might make sense to refinance or make extra payments to eliminate that cost sooner.

Credit Score and Financial Profile Tips for Getting Approved

Your credit score plays a central role in determining both your eligibility and your loan terms when learning how to get a conventional loan with low down payment requirements. A higher score generally means a better interest rate and lower PMI costs, so it's worth taking steps to strengthen your credit before applying.

Here are some practical strategies that may help improve your approval odds:

- Check your credit reports: Review your reports from all three major bureaus for errors or outdated information. Disputing inaccuracies could give your score a meaningful boost.

- Reduce credit card balances: Your credit utilization ratio — how much of your available credit you're using — is a significant scoring factor. Keeping balances below 30% of your credit limit is often recommended.

- Avoid new credit applications: Each hard inquiry can temporarily lower your score. Try to avoid opening new credit cards or taking on other debt in the months before applying for a mortgage.

- Maintain consistent employment: Lenders typically want to see at least two years of steady employment history. Self-employed borrowers may need to provide additional documentation such as tax returns and profit-and-loss statements.

- Document your assets: Even with a 3% down payment, you'll need to show that you have sufficient funds for closing costs and, in some cases, cash reserves. Bank statements and investment account records help verify this.

It's also wise to get pre-approved before house hunting. Pre-approval gives you a clearer picture of your buying power and signals to sellers that you're a serious, qualified buyer.

Comparing the Best Conventional Loans for Low Down Payment Scenarios

Not all low down payment conventional programs are created equal. Choosing among the best conventional loans for low down payment situations depends on your income, credit score, and homeownership history. Here's a brief overview of the most widely available options:

- Fannie Mae HomeReady: Designed for low-to-moderate income borrowers, this program allows a 3% down payment and accepts income from household members who aren't on the loan. It also allows gift funds and down payment assistance. Income limits apply based on the property's location.

- Fannie Mae Standard 97: This option allows 3% down and is available to first-time buyers without income limits. It's a straightforward option for buyers who don't qualify for HomeReady but still want minimal down payment requirements.

- Freddie Mac Home Possible: Similar to HomeReady, this program targets low-to-moderate income buyers with a 3% down payment option. It also permits non-occupant co-borrowers and allows various income sources to count toward qualification.

- Freddie Mac HomeOne: Specifically for first-time homebuyers with no income limits, HomeOne offers 3% down and is a strong choice for buyers in higher-cost markets who may exceed income caps on other programs.

Each of these programs has nuances in terms of homebuyer education requirements, eligible property types, and borrower qualifications. Speaking with a knowledgeable loan officer can help you identify which option aligns best with your specific situation.

Down Payment Sources and Assistance Options Worth Knowing

One of the great advantages of low down payment conventional programs is their flexibility regarding the source of your down payment funds. Many programs allow gift funds from family members, which can be a significant help for buyers who are short on savings but have supportive relatives willing to contribute.

Down payment assistance (DPA) programs are another avenue worth exploring. These are typically offered through state housing finance agencies, local governments, and nonprofit organizations. Some DPA programs provide grants that don't need to be repaid, while others offer second loans with deferred or forgivable terms. Eligibility requirements vary widely, but many programs target first-time buyers and those with moderate incomes.

It's important to verify that any down payment assistance you use is compatible with your chosen conventional loan program. Not all DPA sources are accepted by every lender or program, so confirming compatibility early in the process can prevent delays or complications at closing.

Additionally, some employers offer homebuyer assistance benefits as part of their compensation packages, and certain community development financial institutions (CDFIs) provide specialized lending products for underserved communities. These resources are often underutilized simply because borrowers aren't aware they exist.

●Conclusion

Homeownership doesn't have to wait until you've saved up a 20% down payment. With the right loan program and a solid financial foundation, buying a home with as little as 3% down is a realistic and achievable goal for many borrowers. Whether you're a first-time homebuyer or a repeat buyer looking to preserve your cash, understanding how to get a conventional loan with low down payment options is the first step toward making a smart, informed decision. Take the time to compare programs, review your credit profile, and speak with a qualified mortgage professional who can guide you through the process. The path to your next home may be closer than you think — and LoanWise is here to help you navigate every step of the way.