Buying a high-value home is an exciting milestone, but if a significant portion of your earnings comes from commissions, bonuses, or variable pay, the path to approval can feel more complicated than it needs to be. Jumbo mortgages — loans that exceed conforming loan limits — come with stricter underwriting standards, and lenders tend to look very carefully at income that fluctuates from month to month. The good news is that understanding how to calculate jumbo mortgage affordability with commission income can put you in a much stronger position before you ever submit an application. This guide walks you through the key concepts, documentation requirements, and practical steps that commission earners typically need to navigate when pursuing a jumbo loan.

What Makes Jumbo Loans Different From Conventional Mortgages

A jumbo mortgage is any home loan that exceeds the conforming loan limits set by the Federal Housing Finance Agency (FHFA). These limits vary by location and are adjusted periodically, but in most areas of the United States, any loan above the standard threshold qualifies as a jumbo loan. Because these loans cannot be purchased or guaranteed by Fannie Mae or Freddie Mac, lenders take on more risk — and that means they set their own, often more rigorous, qualification standards.

For commission-based borrowers, this distinction matters quite a bit. Conventional conforming loans follow relatively standardized guidelines for income documentation. Jumbo loans, on the other hand, may differ significantly from one lender to the next. Some lenders may require larger down payments, higher credit scores, lower debt-to-income (DTI) ratios, and more extensive income verification. Knowing these expectations upfront helps you prepare more effectively.

- Loan size: Jumbo loans typically start above the conforming limit, which may be higher in designated high-cost areas.

- Down payment: Many jumbo lenders require at least 10% to 20% down, though requirements vary.

- Credit score: A score of 700 or higher is often expected, with some lenders preferring 720 or above.

- DTI ratio: Lenders may look for a DTI of 43% or lower, though some allow more flexibility for well-qualified borrowers.

- Cash reserves: Jumbo borrowers are often expected to demonstrate several months of mortgage payments in reserve assets.

How Lenders View Commission and Variable Income

One of the most important things commission earners need to understand is that lenders do not simply take your highest-earning month and use that figure to determine what you can afford. Instead, they typically average your commission income over a period of time — most commonly 24 months — to arrive at a stable, reliable income figure. This averaged number is what gets used in affordability calculations.

The reasoning behind this approach is straightforward. Commission income can vary significantly due to market cycles, seasonal fluctuations, or changes in employment. Lenders want confidence that you can sustain mortgage payments even during slower earning periods. If your commission income has been increasing year over year, that trend may work in your favor. However, if income has been declining, lenders may use the lower figure or take a more conservative average.

It's also worth noting that lenders typically distinguish between different types of variable pay:

- Base salary plus commission: If you receive a guaranteed base salary alongside commissions, lenders may count the base salary in full and average the commission portion separately.

- 100% commission income: If your entire earnings come from commissions, lenders may treat this more like self-employment income and require additional documentation such as profit-and-loss statements.

- Bonuses: Year-end or performance bonuses are often averaged over two years if they appear consistently on your tax returns. A one-time bonus may not be counted at all.

For borrowers qualifying for a jumbo loan with bonuses, consistency is key. If your bonus income appears reliably on your W-2s or tax returns across multiple years, there's a better chance a lender will include it in your qualifying income.

Step-by-Step: How to Calculate Jumbo Mortgage Affordability With Commission Income

Understanding how to calculate jumbo mortgage affordability with commission income starts with building an accurate picture of your qualifying income. Here's a practical approach to estimating what you might be able to borrow:

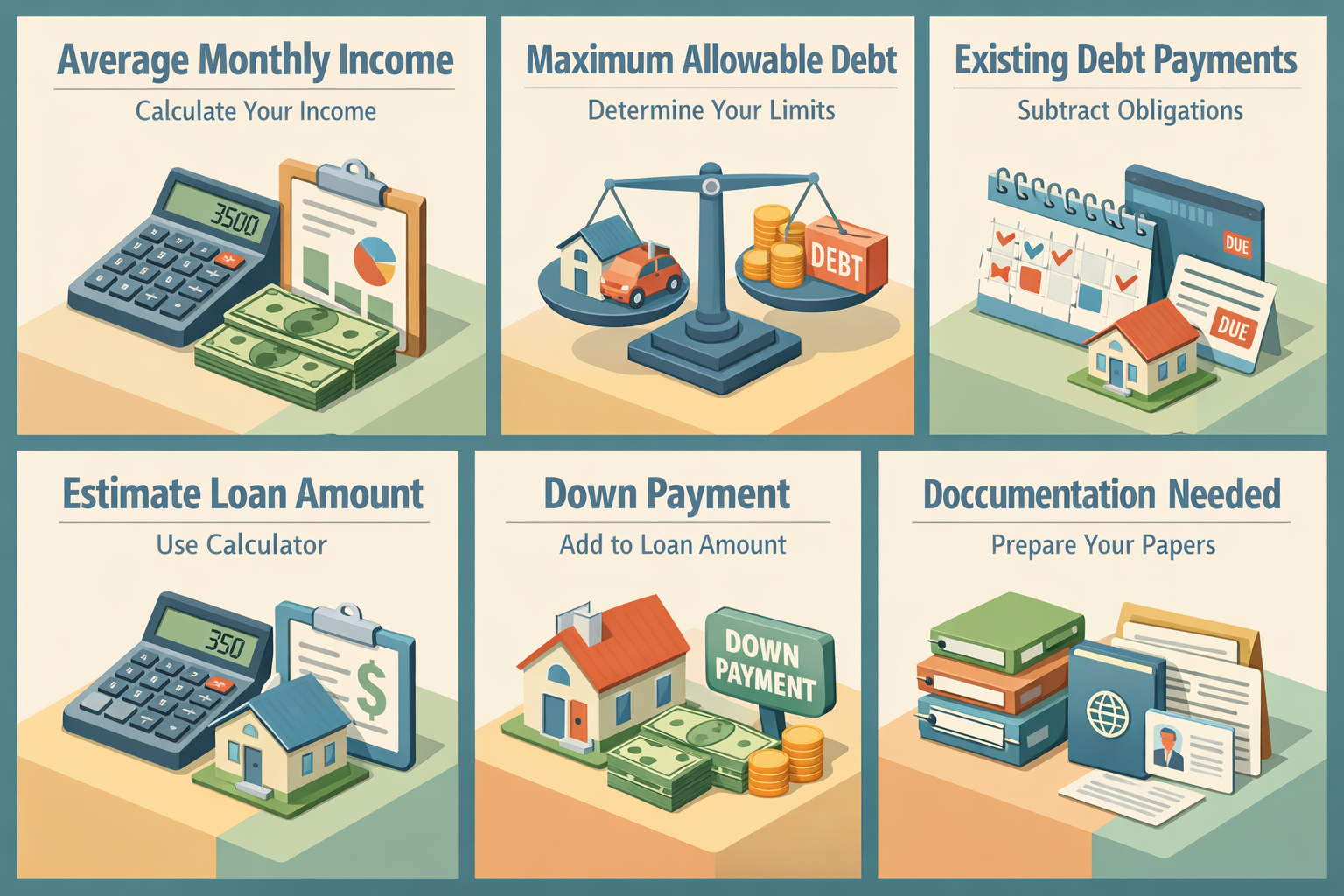

Step 1 — Determine Your Average Monthly Income

Gather your W-2 forms, tax returns, and pay stubs for the past 24 months. Add up all commission and bonus income reported over that period and divide by 24. If your employer pays a base salary, add that monthly figure to your averaged commission total. This combined number is typically what lenders will use as your gross monthly qualifying income.

Step 2 — Calculate Your Maximum Allowable Monthly Debt

Most jumbo lenders prefer a total DTI ratio no higher than 43%, though some may go a bit higher for exceptionally well-qualified borrowers. Multiply your qualifying monthly income by the lender's maximum DTI to get your maximum allowable monthly debt. For example, if your qualifying income is $20,000 per month and the lender's DTI limit is 43%, your total monthly debt obligations — including the new mortgage payment — should generally not exceed $8,600.

Step 3 — Subtract Existing Monthly Debt Payments

Review your current monthly obligations: car loans, student loans, credit card minimum payments, and any other recurring debt. Subtract these from your maximum allowable debt figure. The remaining amount represents the maximum monthly mortgage payment you may qualify for.

Step 4 — Estimate the Loan Amount

Use a mortgage payment calculator to work backward from your maximum monthly payment. Factor in the current interest rate, your anticipated loan term (usually 30 years), and estimated property taxes and homeowner's insurance. This will give you a rough estimate of the maximum loan amount you might be able to support.

Step 5 — Account for the Down Payment

Add your anticipated down payment to the maximum loan amount to estimate what you can afford. Keep in mind that jumbo lenders often require larger down payments, so having 20% or more available can improve both your approval odds and your interest rate.

Income Verification Documents Commission Earners Typically Need

Proper documentation is one of the most critical factors in income verification for commission earners applying for a jumbo loan. Since your income doesn't fit neatly into a simple pay stub review, expect to provide a more comprehensive paper trail. Being organized and proactive with documentation can help speed up the underwriting process.

Most lenders will ask for some combination of the following:

- Two years of federal tax returns (personal and, if applicable, business): These provide the clearest picture of your actual earnings after deductions.

- Two years of W-2 forms: Even if you receive commissions, W-2s show total compensation paid by your employer.

- Recent pay stubs: Typically the most recent 30 days, showing year-to-date commission and base pay.

- Verification of employment: Lenders may contact your employer directly to confirm your position, compensation structure, and likelihood of continued employment.

- Bank statements: Several months of statements may be required to confirm income deposits and demonstrate cash reserves.

- Profit and loss statements: If you're treated as an independent contractor or are self-employed, a current P&L statement signed by a CPA may be requested.

If you're using a self-employed jumbo mortgage calculator or working with a lender on a non-QM (non-qualified mortgage) product, the documentation requirements may differ slightly. Some non-QM jumbo programs allow for bank statement loans, where 12 to 24 months of personal or business bank statements are used in place of tax returns to verify income. This can be especially helpful for borrowers whose tax returns show lower income due to business deductions.

Strategies to Strengthen Your Jumbo Loan Application

If your commission income is variable or your earnings have been inconsistent, there are several steps you can take to improve your chances of approval and potentially secure a more competitive interest rate.

Build a Strong Credit Profile

A high credit score can offset some of the risk lenders associate with variable income. Paying down revolving debt, avoiding new credit inquiries, and keeping account balances low relative to credit limits may all contribute to a higher score over time. Many jumbo lenders look favorably on scores above 720.

Increase Your Down Payment

A larger down payment reduces the lender's exposure and demonstrates financial discipline. Putting down 25% or more on a jumbo purchase may open doors to better rates and more flexible income guidelines, depending on the lender.

Maintain Substantial Cash Reserves

Jumbo lenders often want to see that you have enough liquid assets to cover 6 to 12 months of mortgage payments even after closing. Strong reserves signal that you can weather a slow commission period without defaulting on your loan.

Reduce Your Existing Debt Load

Since DTI is such a critical factor, paying off or paying down existing debts before applying can meaningfully improve your qualifying position. Even reducing a car payment or credit card balance can shift your DTI into a more favorable range.

Work With a Lender Experienced in Variable Income

Not all lenders handle jumbo loans for variable income borrowers in the same way. Some have more flexible underwriting guidelines or access to non-QM products designed specifically for commission earners, self-employed professionals, and business owners. Shopping with a lender who understands your income type can make a significant difference in both your approval odds and your overall experience.

Common Pitfalls Commission Earners Should Avoid

Even well-qualified commission earners can run into trouble during the jumbo loan process if they're not careful. Being aware of common missteps can help you avoid unnecessary delays or denials.

- Overestimating qualifying income: Many borrowers assume lenders will use their peak earning year or their current income momentum. In practice, lenders typically average over two years, which may produce a lower qualifying figure than expected.

- Changing jobs or income structures during the application: Switching from a salaried position to 100% commission, or from employee status to independent contractor, can significantly complicate your application. Try to maintain income consistency in the months leading up to and during the loan process.

- Large, unverifiable deposits: Jumbo lenders scrutinize bank statements carefully. Unexplained large deposits — such as a personal gift or cash sale — may raise questions and require additional documentation.

- Underestimating the impact of tax deductions: Self-employed borrowers and independent contractors often take significant business deductions that reduce their taxable income. While this is a smart tax strategy, it can lower your qualifying income on paper. Talk to your lender early about how your tax returns may affect your application.

- Neglecting to shop multiple lenders: Jumbo loan guidelines vary considerably from one lender to the next. Accepting the first offer without comparing alternatives could mean leaving money on the table.

●Conclusion

Knowing how to calculate jumbo mortgage affordability with commission income is about more than running numbers through a calculator. It's about understanding how lenders interpret variable earnings, preparing the right documentation, and positioning your finances as strategically as possible before you apply. Commission-based income is absolutely a viable path to jumbo loan approval — it may just require a bit more preparation and the right lending partner. If you're ready to explore your options, consider speaking with a lender who specializes in high-value home financing and has experience working with variable income borrowers. The right guidance can help turn a complex process into a clear, manageable path toward the home you're working toward.